The answer is straightforward, and it should bother you. A significant portion flows directly to third-party providers who bear the risk, pay the claims, and keep whatever's left over. That leftover amount — the underwriting profit — is money your dealership generated and then handed away.

F&I now accounts for nearly 40% of total dealership gross profit, up from 25% in 2005. Meanwhile, new vehicle front-end margins fell 14.4% year-over-year in Q1 2025. The math is clear: F&I is carrying more weight, and dealers who don't control the full profit structure of their F&I products are leaving serious money behind.

This article explains what ancillary products are in the insurance and reinsurance context, how they function inside your F&I department, and how dealer-owned reinsurance gives you a direct path to recapturing the profits you're currently surrendering.

TL;DR

- Ancillary products are supplemental coverages sold alongside primary insurance — in dealerships, these include VSCs, GAP, credit life, tire and wheel, and more

- Traditional models send that premium volume to third-party providers, who keep the underwriting profit

- Dealer-owned reinsurance lets you participate in that risk pool and keep the income that previously left your business

- Higher ancillary product volume and stronger F&I penetration directly expand your reinsurance opportunity

What Are Ancillary Products in Insurance?

Ancillary insurance products are supplemental coverages sold alongside a primary policy to fill gaps the core policy doesn't cover — not as a replacement for primary coverage, but as a complement to it.

In health insurance, ancillary products include dental, vision, hearing, and hospital indemnity plans. In property and casualty contexts, the same principle applies: a base policy covers the major risk, and ancillary products layer additional protection around it.

How This Translates to Auto Dealerships

In the dealership context, a customer's auto insurance policy is the primary coverage. Everything sold through your F&I office — vehicle service contracts, GAP, credit life, tire and wheel protection — sits in the ancillary layer.

These products exist because the primary policy leaves real gaps:

- Auto insurance doesn't cover mechanical breakdown

- It doesn't bridge the difference between loan balance and actual cash value after a total loss

- It doesn't protect against road hazard tire damage or unexpected repair costs after the factory warranty expires

The F&I office fills those gaps. Filling them profitably, though, depends on understanding who captures the financial upside when claims come in lower than expected.

Ancillary Products vs. Reinsurance Products

These two terms are related but not interchangeable:

- Ancillary products are what you sell to the customer — the VSC, the GAP waiver, the tire and wheel plan

- Reinsurance is the financial mechanism behind those products — it determines who bears the risk and who captures the profit when claims don't exhaust the reserve

Ancillary products also carry regulatory requirements. They must be structured through properly licensed entities, which is why the reinsurance structure matters — not just for profit, but for legal compliance.

Ancillary Products in the Auto Dealership F&I Department

A well-run F&I office offers several distinct ancillary products, each targeting a specific coverage gap.

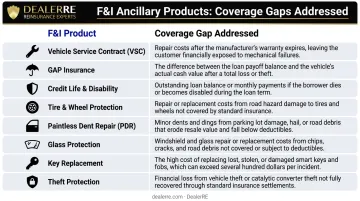

Core F&I Ancillary Products

| Product | Coverage Gap Addressed |

|---|---|

| Vehicle Service Contracts (VSCs) | Mechanical breakdown after factory warranty expiration |

| GAP Insurance | Difference between loan balance and insurance payout in a total loss |

| Credit Life & Disability | Loan payoff if borrower dies or becomes disabled |

| Tire & Wheel Protection | Road hazard damage — nails, potholes, metal, glass |

| Door Ding / PDR | Paintless dent repair without sanding or repainting |

| Windshield Repair | Chips and cracks caused by road debris |

| Key Replacement | Lost or damaged keys and fobs |

| Theft Protection | Window etching and anti-theft labeling programs |

Each product fills a gap a standard auto policy won't cover — and that's the customer-facing value proposition. The more interesting question for dealers is what happens to the money behind each sale.

Where the Real Money Sits

When a customer buys a VSC, the premium collected has two components:

- Dealer markup — this is your immediate F&I gross, captured at point of sale

- Reserve pool — funds set aside to pay future claims

According to Warranty Week, at least 50% of the retail price of a service contract goes to administrative costs and retailer profit — not to actual claims. That gap between what customers pay and what claims cost is the underwriting profit.

In the traditional third-party model, that profit sits with the product provider. When claims don't exhaust the reserve, the provider keeps the surplus — not your dealership. You drove the sale, carried the customer relationship, and sent the underwriting upside out the door with it.

The volume of ancillary products you sell determines how large that opportunity is. High-volume dealers with strong VSC and GAP penetration have the most at stake — and the most to gain from restructuring who captures the risk.

How Dealer-Owned Reinsurance Captures Ancillary Product Profits

The core concept is straightforward: instead of a third-party company bearing the risk on ancillary products and keeping the profit, you establish your own reinsurance company that participates in the risk pool and receives the underwriting income.

The Admin-Obligor Structure

DealerRE specializes in the admin-obligor reinsurance structure, which works as follows:

- Your reinsurance company serves as the obligor on contracts sold to customers

- An A-rated carrier backs the structure, insuring your reinsurance company's obligations

- If your reinsurance company cannot meet its financial obligations, the direct writing insurance company carries the ultimate liability

Dealers who hesitate at the word "reinsurance" often assume it means uninsured exposure. The A-rated carrier backstop means your risk is defined, bounded, and professionally managed — not open-ended.

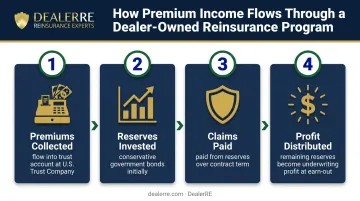

The Profit Flow

Premium income flows through a dealer-owned reinsurance program in four stages:

- Premiums collected at point of sale flow into your reinsurance company's trust account, held at a U.S. Trust Company

- Reserves are invested — initially in conservative government bonds, with more flexibility once the trust balance exceeds 125% of unearned premiums

- Claims are paid from those reserves throughout the contract term

- Remaining reserves become distributable profit at contract earn-out — underwriting income you capture rather than surrendering to a third party

Investment income on the reserves belongs to your reinsurance company from day one, creating a second return stream on top of underwriting profits. That combination is where the tax structure becomes relevant.

Tax Planning Advantages

Property and casualty insurance companies with annual net premiums under the applicable threshold may elect under IRC Section 831(b) to be taxed only on investment income — not underwriting profits. DealerRE coordinates with insurance tax experts and works alongside your CPA to ensure each program is structured correctly and compliantly.

The IRS issued final regulations on Section 831(b) micro-captive structures in February 2025, updating the compliance requirements. Dealers operating under this election should confirm their structure aligns with the updated rules — DealerRE's compliance management handles that review as part of ongoing program administration.

Key Benefits of Including Ancillary Products in a Dealer Reinsurance Program

Profit Retention

Dealers who structure their reinsurance correctly capture underwriting profits that previously left the dealership entirely. DealerRE's dealer clients report realizing hundreds of thousands of dollars in underwriting profit through their reinsured programs — income they didn't know was available before restructuring.

Your third-party warranty provider stays in business because they're making money on your products. Reinsurance lets you capture that income instead.

Customer Experience and Retention

When you own the reinsurance on your ancillary products, you have a direct stake in how claims are handled. DealerRE's full-service model includes claims adjudication support through its administrator, AVP, alongside F&I training to maintain consistent service standards.

Dealers using this structure report stronger CSI scores and better customer retention — because the claims experience reflects the dealership, not a faceless third-party provider.

One DealerRE client put it directly: "Our Family Advantage Program has allowed us to offer our customers a warranty that my dealer competitors can't come close to offering."

Competitive Differentiation

Dealer-branded F&I products create a competitive advantage that generic third-party products can't replicate. Owning the product gives you control over what you offer and how it's positioned against competing franchises or independent lots. That applies whether you're running a certified pre-owned program with a reinsured limited warranty or bundled ancillary protection packages.

When dealers control the product, they also control the story — which is difficult for a competitor to copy.

Key advantages of dealer-branded ancillary products include:

- Full control over product structure and pricing

- Consistent brand experience from sale through claim

- Differentiation that third-party off-the-shelf products can't match

- Flexibility to bundle products into a compelling F&I package

Common Challenges Dealers Face With Ancillary Products and Reinsurance

The Knowledge Gap

Most dealers know F&I generates income. Fewer understand the reserve structure, loss ratios, and claims experience analysis that reveal whether their current program is actually profitable. VSC attachment rates on new vehicles sit at approximately 41.9% according to NADA data, with franchise dealers achieving around 30% on used vehicles — leaving meaningful penetration headroom at most stores.

Understanding the full financial picture requires an experienced reinsurance consultant who can analyze your specific product mix, volume, and claims experience rather than presenting a generic model.

Compliance and Structural Risk

Setting up a dealer-owned reinsurance company incorrectly — wrong entity structure, improper filings, non-compliant forms — creates legal and regulatory exposure. The CFPB's October 2024 auto finance supervisory findings confirmed that federal oversight of F&I add-on practices remains active, making compliant structure non-negotiable.

DealerRE manages all legal forms, filings, tax returns, and renewals on behalf of dealer clients, and partners with vetted administrators, CPAs, and legal counsel to ensure programs operate within regulatory requirements.

F&I Penetration Is the Leverage Point

A reinsurance program is only as profitable as the volume flowing into it. Dealers with low F&I penetration need to invest in training before the reinsurance economics reach their full potential. DealerRE supports that foundation through:

- Online and in-person F&I training classes

- F&I menus and presentation development

- Ongoing F&I performance coaching before and after program enrollment

That training investment also removes a common barrier to entry. Dealers selling more than 30 cars per month can benefit from a reinsurance program — and neither high volume nor significant upfront capital is required to get started.

Frequently Asked Questions

What are ancillary products in insurance?

Ancillary insurance products are supplemental coverages sold alongside a primary policy to cover what the core policy excludes. In auto dealerships, they include VSCs, GAP insurance, credit life and disability, and protection products sold through the F&I office.

What are reinsurance products?

Reinsurance products are financial instruments that transfer risk from one insurer to another. In the dealer context, reinsurance allows a dealer-owned company to assume the risk on ancillary F&I products they sell — and keep the underwriting profit that risk generates.

What ancillary products are typically offered through a dealership's F&I department?

Common F&I ancillary products include vehicle service contracts, GAP insurance, credit life and disability coverage, tire and wheel protection, door ding/PDR coverage, windshield repair, key replacement, and theft protection packages.

Can a dealer keep the underwriting profits from ancillary products?

Yes. Through a dealer-owned reinsurance structure, the dealer participates in the risk pool and receives the underwriting income that would otherwise be retained entirely by a third-party product provider.

How does dealer-owned reinsurance work with ancillary products?

Premiums from ancillary products sold in the F&I office flow into the dealer's reinsurance company. Claims are paid from that reserve throughout the contract term, and remaining profits pay out to the dealer at earn-out. That creates a second revenue stream on top of the original F&I markup.

Is a dealer-owned reinsurance company difficult to set up?

Not with the right partner. DealerRE handles legal formation, carrier agreements, filings, tax returns, and ongoing renewals on behalf of dealer clients. The setup is more straightforward than most dealers expect, and the administrative complexity never falls on the dealership.