Yet most dealers treat both sides reactively. Operational coverage gets renewed annually without much scrutiny. F&I products get sold, a front-end margin gets booked, and the rest — the underwriting surplus that accumulates when claims come in below projections — flows quietly to the third-party provider.

This article covers the insurance coverage dealerships are required to carry, the products they sell customers, the compliance obligations that govern both, and how dealer-owned reinsurance changes the financial math entirely.

TL;DR

- Dealerships require specialized coverage — garage liability, dealer open lot, garage keepers legal liability, and surety bonds — that standard commercial policies don't address.

- F&I products like VSCs, GAP, and ancillary protection plans are major profit drivers, but dealers typically capture only the front-end markup while the underwriting surplus stays with the provider.

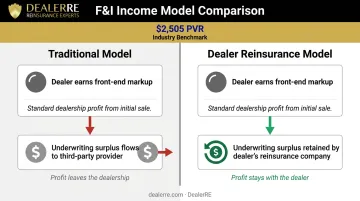

- Public dealer groups averaged $2,505 F&I gross per vehicle retailed in Q1 2025, with F&I representing as much as 73% of total dealership profit in some datasets.

- FTC enforcement, state licensing rules, and the Red Flags Rule create real compliance exposure for dealers who aren't paying attention.

- Dealer-owned reinsurance lets dealers stop funding third-party profits and start retaining the underwriting surplus from every F&I product they sell.

Types of Insurance Coverage Dealerships Must Carry

Running a dealership without the right coverage is illegal in most states. The policies below aren't interchangeable with standard business insurance, and underwriters price and structure them specifically around automotive operations.

Garage Liability

Garage liability is the foundational policy for any auto dealer. It covers bodily injury and property damage arising from dealership operations — test drives, service work, and customer visits. Standard general liability policies aren't designed for these exposures, which is why garage liability exists as a separate product.

Underwriters pay close attention to test drive protocols. Unaccompanied test drives and overnight vehicle releases are red flags that consistently affect both pricing and insurability. The practical implication: document driver IDs, keep test drives accompanied, and prohibit overnight releases in writing.

Dealer Open Lot (Physical Damage)

This coverage protects your inventory against physical damage — collision, theft, vandalism, severe weather, fire, and transit damage. According to Jencap, collision is the most frequently cited peril, but hail and weather events drive significant claim volume depending on geography.

Underwriters evaluate:

- Fencing, lighting, and camera systems on the lot

- Geographic exposure to hail and wind

- Transport radius (thresholds around 200–300 miles are commonly cited)

- Vehicle mix, including salvage, heavy trucks, or motorcycles

- Whether inventory is valued at 100% to avoid coinsurance penalties

Garage Keepers Legal Liability

This is the coverage that protects customer vehicles left in your care — for service, detailing, or repairs. It's separate from your open lot coverage, which protects your own inventory. Keeping distinct limits and deductibles for each is an operational necessity.

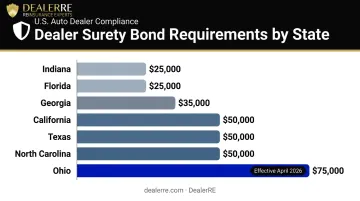

Surety Bonds

Most states require a surety bond as a condition of dealer licensing, and the amounts vary significantly:

| State | Bond Amount |

|---|---|

| Indiana | $25,000 |

| Florida (used dealer) | $25,000 |

| Georgia | $35,000 |

| California (retail) | $50,000 |

| Texas | $50,000 |

| North Carolina | $50,000 (first location) |

| Ohio (effective April 2026) | $75,000 |

A lapsed or insufficient bond doesn't just create a compliance problem — it can trigger immediate license suspension. Multi-rooftop dealers need state-by-state bond calendars that account for renewal dates and any pending legislative increases.

Additional Required or Recommended Coverages

Three additional coverages round out a complete dealership insurance program:

- Workers' compensation is required in most states wherever employees are present

- Commercial umbrella is strongly recommended given the liability exposure in automotive operations

- Active business status matters — insurers may decline to write a garage policy for operations without sufficient ongoing activity; underwriters want to see a functioning dealership

Insurance Products Dealerships Sell to Customers Through F&I

F&I is where insurance stops being a cost and starts being a revenue line. The products below are sold at the point of sale, backed by third-party administrators or carriers, and represent a significant portion of dealership profitability.

Vehicle Service Contracts

VSCs are the most prevalent and profitable F&I product category. A dataset of 202 dealers showed average VSC profit rising from $1,119 to $1,254 per deal across two consecutive six-month periods, with VSC income performing strongest on financed transactions.

The structural problem: in a traditional model, the dealer earns a front-end margin on each contract sold, but the underwriting surplus — what remains after claims are paid — stays with the provider. That surplus exists because providers price conservatively. That's profit your customers generated — and in a traditional structure, you never see it.

GAP Insurance

GAP covers the difference between a vehicle's actual cash value at total loss and the remaining loan balance. It's most directly relevant to BHPH and subprime dealers, where loan-to-value ratios frequently create negative equity from day one.

Regulatory attention on GAP has increased. Several states updated their GAP waiver rules in 2024 — including Colorado, Connecticut, and California — clarifying fee caps, refund requirements, and disclosure obligations. Dealers need state-specific forms and compliant refund workflows, not a one-size-fits-all approach.

Credit Life and Credit Disability

These products insure the loan itself against borrower death or disability. They carry compliance sensitivity: the Quebec AMF has noted that dealer-sold versions can cost consumers significantly more than comparable coverage purchased independently, requiring dealers to ensure buyers understand their options. While that's a Canadian regulatory example, the underlying principle applies broadly — regulators scrutinize whether customers are adequately informed that these products are optional.

Ancillary Products

Beyond the compliance-sensitive products, ancillary offerings follow the same basic structure: sold at the F&I desk, backed by a third-party carrier, with the dealer retaining a front-end markup and the underwriting surplus flowing to the provider. Common products include:

- Tire and wheel protection

- Door ding / paintless dent repair

- Windshield coverage

- Appearance protection

- Roadside assistance

Recent data shows meaningful per-deal income gains in these categories — tire and wheel up roughly $38 per deal, appearance protection up over $93 per deal on financed transactions. Given those numbers, improving product penetration has a direct impact on the bottom line.

Compliance and Regulatory Obligations Around Dealership Insurance

FTC Oversight

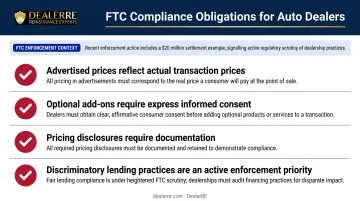

The FTC's CARS Rule was vacated by the Fifth Circuit in January 2025 and never took effect — but enforcement activity hasn't slowed. In December 2024, the FTC and Illinois took action against Leader Automotive Group, resulting in a $20 million settlement tied to deceptive pricing and add-on practices. Enforcement against deceptive pricing and add-on practices has continued since, signaling that the CARS Rule's failure to take effect hasn't reduced regulatory scrutiny.

The practical obligations haven't changed regardless of the CARS Rule's status:

- Advertised prices must reflect actual transaction prices

- Optional add-ons require express, informed consent

- Pricing disclosures need documentation

- Discriminatory lending practices remain an active enforcement priority

State Licensing for F&I Products

Some states require F&I managers or the dealership entity to hold an insurance producer or limited-lines license to legally sell certain products. New York is explicit: the NY Department of Financial Services has opined that unlicensed dealers may not sell GAP insurance or individual credit life policies. GAP waivers may be offered under specific conditions, and group credit life structures face their own constraints.

The practical takeaway: Assuming you don't need a license is the wrong default. Map each F&I product to its licensing requirements by state before selling it.

The Red Flags Rule

Any dealership that extends credit or arranges financing is a covered creditor under the FTC's Red Flags Rule. The rule requires a written Identity Theft Prevention Program that:

- Identifies relevant warning signs (red flags) in customer applications and transactions

- Detects those red flags when they occur

- Responds appropriately when red flags are detected

- Updates the program periodically to address new threats

The program must be board- or principal-approved, and staff need training to apply it at the finance desk and delivery. This isn't an optional best practice — it's a legal requirement with enforcement consequences.

How Insurance Costs and Claims Affect Dealership Profitability

Insurance affects the bottom line in two distinct directions simultaneously.

On the operational side, garage liability, open lot, and workers' comp are direct costs that rise with claim frequency and severity. Dealers with histories of theft, test drive accidents, or inventory damage face higher premiums and, in some cases, reduced market availability. These measures directly influence what you pay for coverage — and whether carriers will write you at all:

- Key security protocols and driver verification procedures

- Documented test drive processes with signed acknowledgments

- Lot surveillance cameras covering vehicle storage areas

- Incident response and reporting workflows

On the F&I side, the picture is more nuanced. F&I gross per vehicle retailed has been climbing: $2,505 PVR for public groups in Q1 2025, with some dealer datasets showing F&I representing 73% of total dealership profit. Those are strong numbers.

But in a traditional arrangement, the dealer captures the front-end markup while the carrier or administrator captures the underwriting surplus (the amount by which collected premiums exceed claims paid over time).

Third-party providers aren't pricing F&I products charitably. That spread between premiums collected and claims paid represents recapturable income. Every year a dealer operates on a commission-only model is a year of underwriting surplus flowing out the door.

For BHPH dealers, the insurance dynamic is even more direct. NIADA data indicates approximately 78% of BHPH lending volume goes to subprime borrowers, with substantially higher repossession rates than traditional lenders. When customers let their insurance lapse on financed vehicles, the dealer's portfolio exposure increases directly.

How well F&I products are structured, maintained, and paid for by the customer base has a measurable impact on actual dealership financial performance — not just in fee income, but in portfolio risk.

Turning Insurance Into a Profit Center: Dealer-Owned Reinsurance

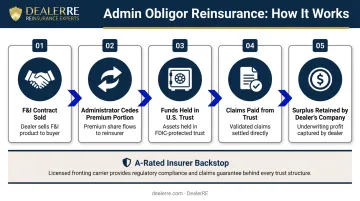

How the Admin Obligor Model Works

Rather than selling F&I products through a third-party provider and keeping only the front-end margin, a dealer establishes their own reinsurance company that participates in the underwriting profits on those same products. When claims come in below collected premiums (which, by design, they usually do), the surplus stays in the dealer's reinsurance company rather than flowing to an external carrier.

The core mechanics work like this:

- The administrator cedes a portion of each F&I premium to the dealer's reinsurance company

- Funds are held in trust at a U.S.-based trust company

- Dealer liability is limited to formation costs plus accumulated earnings

- An A-rated direct writing insurer backstops the obligation if the reinsurance company can't meet it

- The dealer owns 100% of the company, which only reinsures contracts from their own F&I operations

Critically, dealers don't lose the front-end gross. They still make the same per-contract margin they made before. They just also capture the underwriting profit that their third-party provider was keeping.

The Financial Benefits Beyond Premium Capture

The underwriting surplus is only the first layer. Dealers in an admin obligor structure also gain:

- Claims control — the ability to direct service work back to their own service department and manage the customer experience through claims, rather than depending on a third party that may have different priorities

- Reserve investment — once reserves exceed regulatory requirements, accumulated funds can be invested for additional return

- Capital deployment flexibility — earned income can fund real estate purchases, dealership improvements, education, or other personal and business goals

- Tax planning advantages — the reinsurance structure creates a distinct legal entity with its own tax profile, opening planning opportunities not available to dealers operating on a commission-only basis

For BHPH dealers specifically, the structure addresses a problem unique to their business model. Instead of paying the full VSC premium to a third party the month after the sale, premiums are billed monthly as customers make payments.

The dealer builds a customer-funded pool that covers mechanical breakdowns, keeps customers on the road, and reduces portfolio write-offs — all while capturing underwriting profits on the back end.

What DealerRE Manages on Your Behalf

DealerRE has helped more than 400 auto dealers across the country establish and manage their own admin obligor reinsurance companies since 1994. The program covers:

- Legal entity formation and all state regulatory filings

- State approvals for contracts and policies

- Claims adjudication through their administrative partner

- Monthly financial statements and accounting records

- Tax return preparation and annual renewals

- F&I training (online and in-person) and ongoing staff development

- Performance reporting and periodic program reviews

Dealers selling more than 30 cars per month are typically eligible. The analysis to determine fit and project potential underwriting profit recapture is available directly from the DealerRE team.

Frequently Asked Questions

What are the three main reasons for insurance regulation?

Insurance regulation exists to protect consumers from insolvency or fraud, ensure insurers maintain adequate financial reserves to pay claims, and promote fair and competitive market practices. All three principles apply directly to how F&I insurance products are regulated at the dealership level.

What is the Red Flags Rule for auto dealers?

The Red Flags Rule is an FTC regulation requiring dealers who extend credit or arrange financing to maintain a written Identity Theft Prevention Program — one that identifies warning signs of identity theft in customer applications and specifies how staff must respond when those signs appear.

What types of insurance does an auto dealership need to operate?

Core requirements include garage liability, dealer open lot/physical damage for inventory, garage keepers legal liability for customer vehicles in your care, workers' compensation, and a state-mandated surety bond as part of dealer licensing. Requirements vary by state.

Can auto dealers sell insurance products to customers?

Dealers can offer F&I products like VSCs, GAP, and ancillary coverage through licensed third-party administrators, but they generally cannot sell traditional auto insurance directly. Some states — including New York — require specific insurance producer licenses for F&I managers to legally offer certain products.

What is dealer-owned reinsurance and how does it benefit a dealership?

Dealer-owned reinsurance is a structure where the dealer forms their own reinsurance company to capture the underwriting profits on F&I products they sell, rather than those profits going to a third-party provider. It turns F&I income from a one-time front-end markup into a recurring stream of underwriting profits retained by the dealership.

How does garage insurance differ from a standard commercial auto policy?

Garage insurance is purpose-built for auto dealers and combines premises and operations liability with physical damage coverage for inventory vehicles. A standard commercial auto policy covers business-owned vehicles in use but doesn't address dealer-specific exposures like open lot inventory, test drives, or customer vehicles in the dealer's care.