TL;DR

- Layer 3 of the GXL expanded from $600M to $850M excess of $1.5B, raising total GXL coverage to $2.25 billion

- Private placements in Layer 1 grew from three at 25% to four at 27.5%, cutting open market share to 72.5%

- FCC (container vessels) is the only category with a rate increase at +15%; all other categories held flat or declined

- Collective Overspill now attaches at $2.35B (up from $2.1B); Malicious Cyber and Pandemic sublimits each rose to $1.6B

- The RUB war sublimit increased 25% to $125 million

What Is the IG GXL and How Does the Pool Work?

The International Group of P&I Clubs is a consortium of 12 mutual marine liability insurers that together cover approximately 90% of the world's ocean-going tonnage. Because the clubs operate on a mutual basis, large claims don't just sit with the individual club — they move through a structured sharing arrangement before commercial reinsurance ever comes into play.

The claims-sharing architecture works in three distinct tiers:

| Layer | Amount | Who Bears It |

|---|---|---|

| Club Retention | First USD 10 million | Individual P&I Club |

| Pool | USD 90m xs USD 10m | Shared across all 12 Group Clubs |

| GXL (Commercial Reinsurance) | Attaches at USD 100 million | Commercial reinsurance market |

This structure means shipowners effectively access deep catastrophic coverage without purchasing standalone policies — the mutual pooling mechanism does the heavy lifting up to USD 100 million, after which the Group Excess of Loss (GXL) program takes over.

Hydra's Role in the Program

Hydra Insurance Company Limited is the IG's Bermuda-based segregated accounts captive reinsurer. Each of the 12 clubs has its own ring-fenced cell within Hydra, allowing premium that would otherwise flow entirely to the commercial market to stay within the Group's own structure.

Within Layer 1, Hydra retains an Annual Aggregate Deductible (AAD) — USD 103.6 million for 2026/27 — absorbing initial loss frequency before commercial reinsurers are triggered. This stabilises renewal pricing year over year by insulating the open market from routine claim activity.

The parallel to dealer-owned reinsurance is direct. The same logic that drives Hydra — retaining premium inside your own structure rather than ceding it to the market — is what DealerRE helps auto dealers accomplish through their own reinsurance programs.

Whether it's a P&I club or a dealership's F&I operation, keeping underwriting profit in-house means that income builds inside your own entity rather than funding someone else's bottom line.

Key Changes to the 2026/27 GXL Programme

After two consecutive years of elevated pool claims activity in 2024/25 and 2025/26 — following a benign period in 2022/23 and 2023/24 — the IG made five meaningful structural adjustments for 2026/27.

Here's a quick summary of what changed:

- Layer 3 expanded from USD 600 million to USD 850 million, lifting total GXL coverage to USD 2.25 billion

- Layer 1 private placements grew from three at 25% to four at 27.5%, trimming open market share

- Hydra's AAD was recalibrated from USD 107.1 million to USD 103.6 million (proportional adjustment)

- Collective Overspill attachment moved up from USD 2.1 billion to USD 2.35 billion

- Cyber and Pandemic sublimits in Layers 2 and 3 rose from USD 1.35 billion each to USD 1.6 billion each

The sections below break down the rationale behind each change.

Layer 3 Expansion

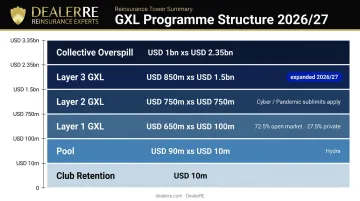

The headline change: Layer 3 grew from USD 600 million to USD 850 million excess of USD 1.5 billion. Total three-layer GXL coverage now stands at USD 2.25 billion excess of USD 100 million, up from USD 2 billion.

This matters because the MV Dali loss — now confirmed at USD 2.8 billion, consuming approximately 93% of the prior GXL tower — demonstrated that the old programme limit left very little headroom above a single catastrophic event. The USD 250 million expansion directly addresses that exposure.

Private Placement Growth in Layer 1

Layer 1 private placements moved from three placements at 25% to four placements at 27.5% (two at 10%, two at 3.75%), reducing the open market share from 75% to 72.5%.

Private placements are renewed independently of the open market, which insulates a portion of Layer 1 pricing from commercial market volatility. More private placement capacity means greater stability in what shipowners pay — particularly useful in a cycle where open market conditions are tightening.

Hydra AAD Adjustment

With the open market share decreasing, Hydra's AAD was recalibrated from USD 107.1 million to USD 103.6 million in 100% terms. This reflects a proportionally smaller share of the 72.5% commercial market order, not a change in risk appetite.

Collective Overspill Attachment

The USD 1 billion Collective Overspill cover now attaches at USD 2.35 billion (up from USD 2.1 billion in 2025/26), a direct consequence of the Layer 3 expansion. This cover is subject to one paid reinstatement and provides a final catastrophic backstop above the GXL tower.

Cyber and Pandemic Sublimits

Aggregate sublimits for Malicious Cyber and COVID/Pandemic risks in Layers 2 and 3 increased from USD 1.35 billion each to USD 1.6 billion each, totalling USD 3.2 billion across both categories. Cover within Layer 1 (up to USD 650 million excess of USD 100 million) remains free and unlimited for these risks.

Breaking Down the Three-Layer GXL Structure for 2026/27

Here is the complete layered structure from ground up:

| Layer | Coverage | Attachment Point | Notes |

|---|---|---|---|

| Club Retention | USD 10m | Ground up | Individual Club bears this |

| Pool | USD 90m xs USD 10m | USD 10m | Shared by all 12 Clubs; Hydra xs USD 30m |

| Layer 1 (GXL) | USD 650m xs USD 100m | USD 100m | 72.5% open market + 27.5% private (4 placements); free & unlimited |

| Layer 2 (GXL) | USD 750m xs USD 750m | USD 750m | 100% open market; aggregate sublimits for Cyber/Pandemic above USD 750m |

| Layer 3 (GXL) | USD 850m xs USD 1.5bn | USD 1.5bn | 100% open market; expanded from USD 600m for 2026/27 |

| Collective Overspill | USD 1bn xs USD 2.35bn | USD 2.35bn | One paid reinstatement |

How Cyber and Pandemic Risks Are Treated by Layer

Layer 1 is the most permissive — Malicious Cyber and Pandemic/COVID losses face no restrictions there. Higher layers apply tighter controls:

- Layer 1: Free and unlimited — no aggregate restrictions apply

- Layer 2 & 3: Separate annual aggregate limits of USD 1.6 billion each (one for Cyber, one for Pandemic) apply above USD 750 million

- Drop-down feature: Layer 3 reinsurers can make their aggregate limit available for Layer 2 claims if needed

- Shortfall: Any losses exceeding aggregate limits are pooled across IG Clubs — shipowner cover is preserved

- Passengers and Crew: Cover limits remain unchanged for 2026/27 — no reduction in protection for these classes

2026/27 Reinsurance Rate Changes by Vessel Category

Full Rate Comparison Table

| Vessel Category | 2025/26 Rate (USD/GT) | 2026/27 Rate (USD/GT) | Change |

|---|---|---|---|

| Persistent Oil Tankers | 0.6258 | 0.5758 | -8.0% |

| Clean Tankers | 0.4337 | 0.4337 | NIL |

| Dry Cargo | 0.6054 | 0.5751 | -5.0% |

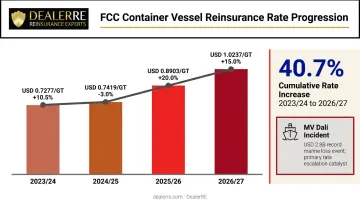

| FCC (Full Container Cargo) | 0.8903 | 1.0237 | +15.0% |

| Passenger | 3.4390 | 3.1472 | -8.5% |

Charterers categories were not published in the 2026/27 primary IG rate table and should be confirmed directly with your club.

Why FCC Rates Keep Climbing

Container vessels are now in their third consecutive year of adverse rate movement. The cumulative rate data shows just how much ground has shifted:

| Year | FCC Rate (USD/GT) | Change |

|---|---|---|

| 2023/24 | 0.7277 | +10.5% |

| 2024/25 | 0.7419 | -3.0% |

| 2025/26 | 0.8903 | +20.0% |

| 2026/27 | 1.0237 | +15.0% |

From 2023/24 to 2026/27, the FCC rate has risen 40.7% cumulatively. The MV Dali allision with the Francis Scott Key Bridge in Baltimore (March 2024) is the primary driver — now confirmed as the largest single marine insurance loss on record at USD 2.8 billion. The 2025/26 and 2026/27 rate increases both reflect that loss's continued impact on container vessel claims experience against the GXL.

Rate Reductions for Other Categories

While FCC absorbs compounding losses, other categories tell a different story. The IG's Reinsurance Committee reviews rates annually to reallocate programme costs based on historical loss experience — and for 2026/27, most vessel types benefited:

- Persistent Oil Tankers (-8.0%) and Passenger (-8.5%) vessels saw the largest reductions, reflecting relatively favorable loss experience against the GXL

- Dry Cargo (-5.0%) also declined, consistent with its claims record

- Clean Tankers held flat — neither rewarded nor penalized

The rate reallocation mechanism means total programme cost is redistributed by category rather than uniformly increased — better-performing categories get reductions while FCC absorbs the compounding impact of its own claims history.

Special Coverage Areas: War, MLC, and Cyber/Pandemic Risks

War Cover and the RUB Exclusion

The Excess War P&I cover is renewed for 12 months with premium included within overall rates, and per vessel limits of USD 500 million are maintained. However, reinsurers continue to apply Territorial Exclusion language for vessels trading in Russia, Ukraine, and Belarus (RUB) waters due to the ongoing conflict.

To address this gap, the IG increased its aggregated sublimited cover for RUB excluded risks from USD 100 million to USD 125 million — a 25% increase. The RUB sublimit has expanded progressively as market capacity has developed:

| Policy Year | RUB Sublimit |

|---|---|

| 2024/25 | USD 80 million |

| 2025/26 | USD 100 million |

| 2026/27 | USD 125 million |

MLC Cover

The Maritime Labour Convention (MLC) market reinsurance cover is renewed at competitive terms for 2026/27, with premiums included in overall rates. MLC cover protects against crew-related financial liabilities. Under Regulation 4.2 of the MLC 2006, shipowners must provide financial security to compensate seafarers in cases of sickness, injury, or death connected to their employment.

Malicious Cyber and Pandemic Framework Summary

- Below USD 750m: Free and unlimited across all layers for both risk categories

- USD 750m–USD 2.35bn: Separate USD 1.6bn aggregate towers for Malicious Cyber and COVID/Pandemic respectively

- Above aggregate limits: Shortfall is pooled across IG Clubs — no change to actual shipowner cover

- Introduced 2022: These limits followed reinsurer-driven coverage restrictions applied across the broader market

Frequently Asked Questions

What is the IG Group Excess of Loss (GXL) reinsurance contract?

The GXL is the International Group of P&I Clubs' annual commercial reinsurance program that attaches above the USD 100 million Pool ceiling. For 2026/27, it provides up to USD 2.25 billion of layered coverage across three layers for claims exceeding individual Club and Pool retentions.

What is Hydra, and what role does it play in the IG programme?

Hydra is the IG's Bermuda-based segregated accounts captive reinsurer. Each of the 12 Group Clubs maintains a ring-fenced cell within Hydra, retaining premium that would otherwise flow to commercial markets. For 2026/27, Hydra holds an Annual Aggregate Deductible of USD 103.6 million within Layer 1.

Why did FCC (container vessel) reinsurance rates increase again for 2026/27?

Container vessels have the worst claims record against the GXL, heavily influenced by the MV Dali casualty — now the largest single marine insurance loss on record at USD 2.8 billion. FCC rates have risen cumulatively by approximately 40.7% since 2023/24, with the 2026/27 +15% increase continuing that trajectory.

What is the Collective Overspill cover?

The Collective Overspill is an additional USD 1 billion of reinsurance purchased by the IG that attaches at USD 2.35 billion — above the top of the three-layer GXL. It provides a final catastrophic backstop and is subject to one paid reinstatement.

How does the 2026/27 GXL handle malicious cyber and pandemic risks?

Both risks receive free and unlimited cover within Layer 1 (up to USD 650m xs USD 100m). Above USD 750 million, separate annual aggregate limits of USD 1.6 billion each apply across Layers 2 and 3 — any shortfall above those limits is pooled across IG Clubs to preserve shipowner cover.

What does the Russia/Ukraine/Belarus territorial exclusion mean for war cover?

Standard Excess War P&I cover excludes vessels trading in Russian, Ukrainian, and Belarusian waters under reinsurer territorial exclusion language. The IG separately purchased USD 125 million of aggregated sublimited cover to fill this gap for 2026/27, up from USD 100 million in 2025/26.