Reinsurance exists specifically to address this exposure. It redistributes risk before it becomes a solvency problem — and for dealers, it does something more: it converts that risk into a profit opportunity.

This article covers what reinsurance is, how it works mechanically, the types available, the risk management benefits it provides, the risks embedded within any reinsurance arrangement, and how auto dealers — including Buy Here Pay Here (BHPH) operators — use dealer-owned reinsurance to protect their business and retain profits they're currently handing to third parties.

TL;DR

- Reinsurance transfers a defined portion of insurance risk from one party (the cedent) to another (the reinsurer), reducing catastrophic financial exposure.

- Two primary structures exist: facultative covers individual risks; treaty applies automatically across a product portfolio.

- Key benefits include solvency protection, expanded underwriting capacity, and loss smoothing.

- For auto dealers, a dealer-owned reinsurance program captures underwriting profits that third-party F&I providers currently keep.

- Program structure (proportional vs. excess-of-loss, admin obligor vs. fronted) shapes how much risk you retain and how profits flow back to you.

What Is Reinsurance and How Does It Work?

The Insurance Information Institute defines reinsurance as a contractual arrangement where an insurer transfers part of its risk to another company — the reinsurer — in exchange for a share of the premium. The phrase "insurance for insurers" captures it well.

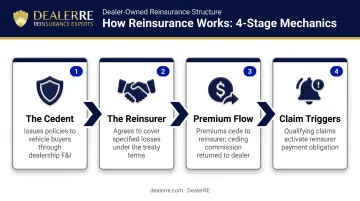

The Mechanics of Risk Transfer

Here's how the structure works in practice:

- The cedent (primary insurer) issues policies and remains directly responsible to policyholders for all claims.

- The reinsurer agrees to cover a specified share of losses — either from the first dollar or after a defined threshold (the retention limit) is crossed.

- Premium flow: The cedent pays the reinsurer a portion of collected premiums to fund the reinsurer's obligation. In proportional arrangements, the reinsurer often returns a ceding commission to cover the cedent's acquisition and administrative costs.

- Claim triggers: The reinsurer either shares losses proportionally from day one, or steps in only after the cedent's net losses exceed the retention limit — depending on the contract structure.

The NAIC reinforces a critical point: the cedent retains ultimate liability to policyholders. Reinsurance doesn't eliminate that obligation — it funds it more sustainably.

Why This Matters Beyond Traditional Insurers

Reinsurance isn't only for large carriers. Auto dealerships can establish their own reinsurance entities to manage the claims risk on F&I products they sell.

Rather than outsourcing that risk to a third-party provider and surrendering the underwriting profit along with it, dealers can retain both the risk and the reward. A-rated carrier backing provides the regulatory and solvency structure the program requires.

Types of Reinsurance: Facultative, Treaty, and Proportional Structures

The structure of a reinsurance arrangement determines how much risk is retained, how premiums are shared, and whether the program can realistically operate at scale.

Facultative vs. Treaty

| Structure | How It Works | Best Use Case |

|---|---|---|

| Facultative | Covers one specific risk, negotiated individually; reinsurer can accept or decline each submission | High-value, unusual, or non-standard exposures |

| Treaty | Automatically covers an entire portfolio or product class without individual negotiation | High-volume, standardized products like vehicle service contracts or GAP |

For auto dealer F&I programs, treaty structures are the practical choice. When a dealer sells hundreds of VSCs annually, negotiating each one individually isn't feasible. Treaty arrangements apply coverage across the entire book automatically — no per-contract submissions, no delays. Once the second structural decision is made, that efficiency compounds further.

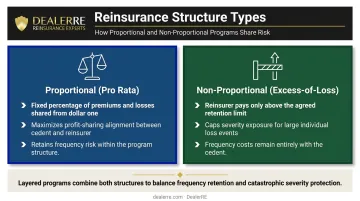

Proportional vs. Non-Proportional

The second structural decision is how losses are shared:

- Proportional (pro rata): The reinsurer shares a fixed percentage of both premiums and losses from the first dollar. This maximizes profit-sharing alignment but leaves frequency risk — the day-to-day volume of smaller claims — with the dealer program.

- Non-proportional (excess-of-loss): The reinsurer only pays losses above a set retention limit. As Munich Re's non-proportional brief notes, this structure caps severity exposure while keeping frequency costs on the ceding dealer program.

Many well-structured dealer programs layer both: a proportional treaty for standard product volume, with an excess-of-loss layer providing tail protection against unusually large or concentrated loss events.

Key Risk Management Benefits of Reinsurance

The Reinsurance Association of America identifies three core functions reinsurance serves — each directly applicable to dealer-owned programs.

Financial Stability and Solvency Protection

Without reinsurance, a single catastrophic claim period can deplete reserves and threaten operations. Reinsurance caps net exposure so that insurers — and dealers running their own programs — can maintain required financial minimums without liquidating assets or halting business.

For dealers, this is particularly relevant during economic downturns or when a specific vehicle model generates unusually high breakdown rates across a portfolio.

Expanded Underwriting Capacity

That solvency protection also creates room to grow. By transferring a portion of risk to the reinsurer, the cedent can write more policies than their capital alone would support. For a dealer, this means selling more F&I products without proportionally increasing balance sheet exposure — the reinsurer absorbs a defined share of potential losses, freeing capital for higher volume.

Claims Smoothing and Profit Retention

These two mechanisms reinforce each other:

- Smoothing: Instead of facing full exposure to one bad claims year, the reinsurance structure distributes losses across a much larger pool — stabilizing results year over year.

- Profit retention: When claims are low relative to premiums collected, the unused premium stays in the reinsurance entity. Under a third-party arrangement, that surplus goes to the vendor. Under a dealer-owned structure, it stays with the dealer — and that difference compounds significantly over time.

Regulatory and Reserve Compliance

Reinsurance reduces net liability on the balance sheet, which helps primary insurers meet statutory reserve requirements. In dealer-owned admin obligor programs, A-rated carrier backing handles this directly — the carrier satisfies solvency and regulatory obligations while the dealer captures the underwriting profits.

What Are the Risks Within Reinsurance Programs?

Reinsurance doesn't eliminate risk — it shifts where that risk sits. Before entering any reinsurance arrangement, dealers need to understand the three core exposures that affect program performance and long-term profitability.

Counterparty (Credit) Risk

When a cedent transfers risk to a reinsurer, the cedent still carries ultimate liability to its policyholders if the reinsurer becomes insolvent. The reinsurer's financial strength is a critical selection factor, not an afterthought.

AM Best's Financial Strength Rating (FSR) scale is the standard measure:

| FSR Category | Symbols | Meaning |

|---|---|---|

| Superior | A++, A+ | Superior ability to meet ongoing obligations |

| Excellent | A, A- | Excellent ability to meet ongoing obligations |

| Good | B++, B+ | More vulnerable to adverse changes |

| Fair through Poor | B and below | Increasing vulnerability |

Most well-managed programs set a minimum counterparty threshold at A- (Excellent) or better. DealerRE's admin obligor structure requires A-rated carrier backing to meet this standard — protecting dealers from the financial exposure that comes with lower-rated obligors.

Underwriting and Pricing Risk

If premiums collected are insufficient to cover actual claims plus administrative costs, the program becomes unprofitable. This risk is managed through:

- Accurate product pricing based on historical claims data and actuarial analysis

- Ongoing loss ratio monitoring to catch adverse trends before they compound

- Adjusting coverage terms or premium rates when actual claims deviate from projections

- Working with an experienced administrator who understands F&I product performance across dealer segments

Regulatory and Operational Risk

Reinsurance programs operate within a complex compliance environment — state insurance regulations, tax filing requirements, and corporate governance obligations all apply. Gaps in any of these areas can expose the dealer's reinsurance company to penalties, forced restructuring, or loss of operating status.

Key operational controls include:

- Maintaining current state filings and corporate renewals

- Ensuring tax returns are filed accurately and on time

- Documenting claims adjudication processes for audit readiness

- Partnering with an administrator who manages compliance as part of the program — not as an add-on

DealerRE manages legal forms, filings, tax returns, and renewals on behalf of dealer clients, reducing the operational burden and compliance exposure that comes with running a dealer-owned reinsurance company.