With front-end vehicle margins falling 38% between 2022 and 2024 (from $6,244 to $3,857 per unit), according to VisionAST's 2025 dealership profitability report, the F&I department has become the primary variable profit driver at most franchise stores — not a supplemental one.

This guide is written for dealership owners, dealer principals, and general managers who want a clear, complete picture of the F&I manager's role: what they do every day, what products they sell, what compliance obligations they carry, what to look for when hiring, how they're paid, and how a well-run F&I program connects directly to your store's financial performance.

TL;DR

- The F&I manager owns every deal from the point of sale through funding — financing, products, paperwork, and lender submission

- F&I now accounts for up to 73% of variable gross profit at many dealerships as front-end margins continue compressing

- Core products include VSCs, GAP, prepaid maintenance, tire and wheel, and credit life/disability insurance

- Compliance obligations span TILA, ECOA, FCRA, and GLBA; misrepresentation is the top regulatory risk

- Average F&I manager compensation ranges from $119K to $150K+, with top performers reaching $210K–$250K

- Dealer-owned reinsurance programs let dealers keep underwriting profits instead of paying third-party administrators

What Is an F&I Manager?

F&I stands for Finance and Insurance. The F&I manager is the dealership employee responsible for finalizing vehicle transactions — taking over once the salesperson closes a deal and seeing the transaction through to funded. In automotive contexts, "F&I Manager" and "Finance Manager" are used interchangeably.

Where the F&I Manager Fits in the Dealership

The F&I manager enters the deal after the salesperson has reached an agreement with the customer. From that point forward, they own the transaction entirely:

- Securing and presenting financing options

- Presenting F&I protection products

- Preparing and executing all legal and lender-required documentation

- Assembling and submitting the funding package to the lender

The scope is broad — and so is the financial exposure. Approximately 85% of new car purchases in the U.S. are financed, meaning nearly every deal that crosses the showroom floor runs through the F&I office.

The F&I department accounted for 25.6% of total dealership gross profit in 2024, and that share is growing as front-end margins compress further. When front-end gross shrinks, the F&I office is often the only place left to recover it — which makes the manager in that seat one of the most consequential hires in the building.

Core Day-to-Day Responsibilities of an F&I Manager

The F&I manager's day is a sequence of high-stakes tasks, often running multiple deals simultaneously. Here's what that looks like in practice.

Credit Application Review and Lender Submission

The F&I manager reviews the customer's credit application and pulls the credit report, analyzing:

- Debt-to-income (DTI) ratio

- Employment history and income documentation

- Prior auto loan payment history

- Derogatory marks, collections, or public records

Based on that analysis, they select the most appropriate lenders to submit the deal to, review approval responses, and present the best available terms to the customer.

Deal Structuring

Structuring a deal means setting all financial components to meet both lender guidelines and dealership policy:

- Selling price and trade-in values

- Down payment requirements

- Interest rate (including finance reserve — the dealer markup above the lender's buy rate)

- Term length and monthly payment

Finance reserve is a meaningful profit component and a compliance-sensitive one. The CFPB has previously scrutinized discretionary dealer markup practices under ECOA, making consistent, documented rate-setting practices essential.

F&I Product Presentation

With financing set, the F&I manager presents a menu of protection products — vehicle service contracts, GAP, tire and wheel, and similar ancillary coverage. The presentation works best as a consultative walkthrough: understanding what the customer values, explaining what each product covers, and matching options to their actual needs and budget.

Documentation and Deal Finalization

Before any vehicle is delivered, the F&I manager prepares, reviews, and executes all required documents:

- Retail installment sales contracts

- Lender-specific paperwork

- Product agreements and disclosures

Every document must be accurate, complete, and properly disclosed. Incomplete or misdisclosed paperwork can trigger lender chargebacks, rescission risk, or regulatory scrutiny — making this step one of the most consequential in the deal.

Funding and Stipulation Management

After signing, the F&I manager assembles the funding package and submits it to the lender. Most lenders will return stipulations — requests for additional documentation such as proof of income, insurance verification, or trade title copies. Resolving these promptly matters: deals that sit unfunded tie up floor plan and create real cash flow drag on the dealership.

F&I Products the Manager Presents and Sells

F&I product sales are where the majority of back-end gross profit is generated. Per vehicle retailed (PVR) and product penetration rates are the two primary metrics used to evaluate F&I performance.

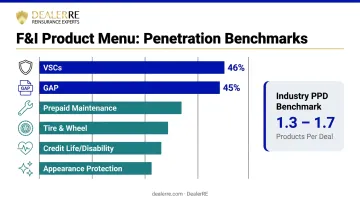

The Core Product Menu

| Product | What It Does |

|---|---|

| Vehicle Service Contracts (VSCs) | Covers mechanical and electrical repairs after the factory warranty expires |

| GAP Insurance | Covers the gap between the loan balance and the vehicle's actual cash value in a total loss |

| Prepaid Maintenance | Bundled oil changes, tire rotations, and inspections purchased at delivery |

| Tire & Wheel Protection | Covers repair or replacement from road hazard damage |

| Credit Life & Disability | Pays off or makes loan payments in the event of death or disability |

| Appearance Protection | Paint, fabric, and interior surface protection |

VSCs and GAP lead in both penetration and profit contribution. Industry benchmarks show service contract penetration at 46% and GAP at 45%, according to JM&A Group — with products per deal (PPD) ranging from 1.3 to 1.7. Stores below these thresholds have clear, measurable revenue gaps.

The F&I Menu Presentation

A structured F&I menu presentation shows customers all their options at once, without obscuring pricing or creating pressure. When executed consistently, menu selling improves both penetration rates and customer satisfaction scores. CDK Global's research found that shoppers who spent more time with the F&I manager reported higher satisfaction — meaning a thorough, well-organized presentation builds trust, not resistance.

The Profitability Angle for Dealers

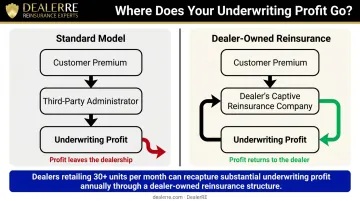

F&I product profits are typically split between the dealership and the third-party administrator or insurance company backing the product. That means a portion of every contract sold leaves your store.

Dealers who establish a dealer-owned reinsurance program — such as those structured by DealerRE — replace those third-party providers with their own captive reinsurance company. When contracts expire, the underwriting profits that would have gone to an external administrator flow back to the dealer instead. That shift can meaningfully change the economics of your F&I department:

- Recaptures underwriting profits currently paid to third-party warranty administrators

- Generates returns from premium reserves invested during the contract term

- Gives dealers direct control over claims experience and product pricing

Compliance, Legal Duties, and Lender Relations

The F&I office operates under a layered compliance framework. An F&I manager who doesn't understand these obligations creates real regulatory and reputational risk for the dealership.

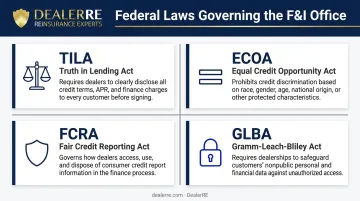

Federal Laws Every F&I Manager Must Know

- Truth in Lending Act (TILA) — Requires disclosure of the amount financed, finance charge, APR, and total of payments before signing

- Equal Credit Opportunity Act (ECOA) — Prohibits credit discrimination and requires adverse action notices when financing is denied or terms are less favorable

- Fair Credit Reporting Act (FCRA) — Governs permissible use of consumer credit reports and requires adverse action notices

- Gramm-Leach-Bliley Act (GLBA) — Requires written information security programs and privacy notices to protect customer data

State-specific disclosure requirements add another layer on top of these federal obligations.

Misrepresentation: The Most Common Risk

Regulatory exposure in the F&I office most often comes from misrepresentation — whether that's misstating the terms of a product, inaccurately booking vehicle information, or failing to disclose required information clearly. The FTC issued warning letters to auto dealership groups in 2023 regarding deceptive pricing and junk fee practices, signaling that enforcement scrutiny on F&I offices is intensifying.

Lender Relationships

A skilled F&I manager maintains active knowledge of each lender's programs and guidelines. Strong lender relationships directly affect dealership performance:

- Better approvals on difficult or non-prime deals

- Competitive rates that improve customer close rates

- Faster funding that improves cash flow for the dealership

- Access to specialty programs for unique financing situations

Certification

Many dealerships require F&I managers to hold an AFIP certification (Association of Finance and Insurance Professionals). AFIP has certified more than 70,000 professionals and requires an 80-question exam covering federal law, ethics, and state regulations. Recertification is required every two years, keeping knowledge current as regulations continue to change.

Key Traits and Qualifications to Look For When Hiring

Professional Qualifications

- 1–2 years of automotive sales experience minimum

- Comfort with financial documents, credit analysis, and basic math

- Organizational discipline to manage multiple deals simultaneously

- Strong professional ethics — the F&I office is a trust-intensive environment

Critical Soft Skills

- Empathy and active listening — customers in the finance office are often anxious; a good F&I manager reads that and adjusts accordingly

- Consultative selling — presenting products as solutions, not pitching them

- Persistence without corner-cutting — working difficult deals through proper channels

Cross-Departmental Communication

Strong cross-departmental communication separates good F&I managers from great ones. The customer's experience carries from the sales floor directly into the finance office — any breakdown in that handoff shows.

Look for candidates who consistently:

- Keep the sales team updated on deal status and lender conditions

- Collaborate with the GM on deal structure and approval strategy

- Communicate clearly and professionally with lenders and product vendors

Dealers who treat the F&I office as an isolated function tend to see lower CSI scores and more deal friction. A manager who communicates well across departments removes those bottlenecks before they start.

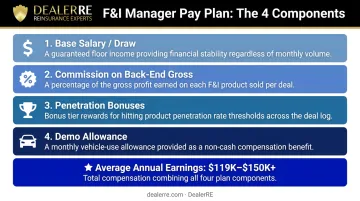

F&I Manager Salary and Compensation Structure

F&I compensation is performance-driven by design. Average annual earnings range from $118,982 (Indeed, based on 1,400 salary reports) to over $150,000 for the majority of working F&I managers, according to industry surveys. Top 10% earners reach approximately $210,500, with elite performers exceeding $250,000.

How Pay Plans Typically Work

Most F&I pay plans combine:

- Base salary or draw — a guaranteed weekly amount, often structured as a draw against future commissions

- Commission on back-end gross profit — typically a percentage of net F&I profit after product cancellation chargebacks

- Penetration bonuses — additional commission tiers triggered when product penetration rates hit defined thresholds (for example, a higher commission percentage when penetration exceeds 50%)

- Demo allowance — a monthly vehicle allowance in many stores

A manager who achieves strong PVR and maintains high penetration rates will earn substantially more than one posting mid-tier results. Well-structured pay plans create a direct link between product performance and take-home earnings — giving managers a financial reason to sharpen their process, not just show up.

The role carries an estimated 32% turnover rate, often driven by newer managers struggling to keep deals funded in tighter credit environments. Dealerships with well-structured training programs and competitive pay plans retain better talent longer.

How the F&I Office Drives Dealership Profitability

Front-end vehicle gross profit has been under sustained pressure. Front-end GPU dropped from $6,244 in 2022 to $3,857 in 2024 — a 38% decline in two years, with no signs of recovery.

Meanwhile, F&I PVR for publicly traded dealer groups reached $2,534 in Q3 2025, up 5.2% year-over-year. The national average for franchise dealers sits in the $1,700–$1,900 range (JM&A Group, 2025). The gap between those two figures — roughly $600–$800 per vehicle — represents significant unrealized profit for average-performing stores. At 1,000 units per year, closing half that gap yields $300,000–$400,000 in additional annual gross.

The Metrics That Matter

Dealers who consistently track and coach these metrics tend to outperform:

- PVR (per vehicle retailed) — total F&I gross profit divided by units sold

- Product penetration rates by category — VSC, GAP, prepaid maintenance, ancillary products

- Finance reserve — margin generated from interest rate markup

- Products per deal (PPD) — industry benchmark is 1.3–1.7

Tracking these numbers is the starting point. Where many dealers leave money on the table is in the structure behind the products themselves.

The Reinsurance Amplifier

When a dealership sells a VSC or GAP policy through a third-party administrator, a portion of the premium — the underwriting profit on unexpired or unclaimed contracts — leaves the store.

A dealer-owned reinsurance structure, like those established through DealerRE, changes that equation. The dealer sets up their own administrator obligor reinsurance company, backed by A-rated insurers. Products are still sold the same way in the finance office, but when contracts expire without claims, the underwriting profit flows back to the dealer's reinsurance company rather than to a third party. Dealers retain control over claims, drive repair work back to their service department, and build a growing pool of captive capital over time.

DealerRE has been helping franchise dealers, independent retailers, and BHPH operators establish and manage these programs since 1994. For stores retailing more than 30 units per month, the math is straightforward: every dollar in underwriting profit that currently goes to a third party is a dollar that could stay in the dealership.

Frequently Asked Questions

What does an F&I manager do?

The F&I manager finalizes vehicle transactions by securing financing, presenting protection products, completing all legal paperwork, and ensuring deals fund with lenders. They own the deal from the moment the salesperson hands off the customer through the point the lender releases funds.

How is an F&I manager paid?

Most F&I managers earn a base salary or draw combined with a commission percentage of back-end gross profit, typically adjusted for product cancellations. Penetration bonuses tied to product acceptance rates are common in well-structured pay plans.

What products does an F&I manager sell?

The core menu covers vehicle service contracts, GAP insurance, tire and wheel protection, prepaid maintenance, credit life and disability, and appearance packages. VSCs and GAP consistently generate the highest penetration rates and profit per deal.

What qualifications does an F&I manager need?

Most dealerships require at least one to two years of automotive sales experience, solid knowledge of finance and compliance regulations, and demonstrated professional ethics. AFIP certification (or a comparable credential) is increasingly expected as evidence of compliance competency.

What is the difference between an F&I manager and a finance director?

An F&I manager handles day-to-day transactions in the finance office at a single store. A finance director (or F&I director) typically oversees multiple F&I managers across a store or dealer group, taking on a supervisory and strategic role rather than working individual deals.

How does the F&I manager affect overall dealership profitability?

With front-end margins compressed, the F&I office is often the single largest contributor to per-vehicle gross profit. A skilled F&I manager directly determines how much of each deal's potential is captured, making their performance one of the highest-leverage variables in the dealership's financial results.