That gap is expensive. Floor plan interest is rising — net floor plan expense per vehicle climbed roughly 39% in Q2 2025, adding approximately $139 per unit in carrying costs. Meanwhile, front-end gross on new vehicles fell 14.4% year-over-year in Q1 2025. The margin pressure is real and compounding.

This article explains how floor plan financing works, what dealer reinsurance is, how the two programs connect operationally, and why treating them separately leaves significant money on the table.

TL;DR

- Floor plan financing is a revolving credit line repaid as vehicles sell, not on a fixed schedule

- Dealer reinsurance lets you own the company that captures underwriting profits from F&I products you already sell — instead of sending that money to third-party providers

- F&I gross profit now averages $2,612 per vehicle retailed, and without reinsurance, most of that underwriting income leaves your dealership

- Reinsurance earnings can offset floor plan costs, fund inventory, or build personal wealth outside the dealership

- The two tools are connected — knowing how they interact is where the real profitability advantage starts

What Is Dealer Floor Plan Financing?

Floor plan financing is a specialized revolving credit facility that lets auto dealers buy vehicle inventory without committing operating cash to every purchase. The lender pays the auction, manufacturer, or wholesaler directly. The vehicle goes onto the lot as collateral. The dealer repays that specific unit's balance when the vehicle sells.

It functions similarly to a business credit card secured by physical inventory — the credit replenishes as units turn, which suits the cyclical cash flow pattern of a dealership far better than a traditional term loan would.

Who Provides Floor Plan Financing

| Lender Type | Examples | Advance Rate | Who They Serve |

|---|---|---|---|

| OEM Captive Finance | Ford Credit, Toyota Financial | 95–100% of invoice | Franchised dealers |

| Commercial Banks | Bank of America Dealer Services | 95–100% of invoice | Franchise and large independents |

| Specialty Non-Bank Lenders | AFC, Floorplan Xpress | 75–90% of vehicle value | Independent and BHPH dealers |

The Cost Variable Most Dealers Underestimate: Curtailment

Understanding who lends is only half the equation — how lenders charge is where most dealers get caught off guard.

Curtailment is a mandatory principal reduction triggered when a vehicle sits unsold beyond the lender's agreed term — typically 60 to 120 days. Schedules generally require paydowns of 5–20% of the original loan balance every 30 to 60 days after that threshold. Holding costs start accruing on day one, not after the curtailment clock runs out.

The numbers add up faster than most dealers realize:

- $7.90/day in new-vehicle holding costs means a unit sitting 63 days costs over $497 in floor plan interest alone — before any curtailment fees apply

- The industry benchmark is 12x annual turns (every 30 days), but the U.S. average is 5.8x

- Most dealers are carrying more than double the optimal floor plan burden

Floor plan lines currently price at SOFR + 200 to 400 basis points depending on dealer credit quality. With 38% of dealers reporting higher rates have severely or significantly impacted floor plan costs, this is no longer a background expense — it demands active P&L management.

What Is Dealer Reinsurance?

Dealer reinsurance is a financial structure where the dealer owns a company that participates in the underwriting profits generated by F&I products sold to customers. Instead of 100% of that premium income flowing to a third-party administrator or insurer, a portion flows back into the dealer's own company. Understanding why this structure exists starts with how F&I profit actually flows — and where it goes without reinsurance.

Why It Exists

When a dealer sells a vehicle service contract, GAP policy, or other F&I product, they earn a front-end commission. The administrator keeps the rest, and if claims come in below expectations, the administrator keeps that underwriting profit too.

Reinsurance changes that equation. The dealer's company receives a share of the premium, pays claims from those reserves, and retains whatever surplus remains. F&I gross profit PVR hit $2,612 in Q4 2025, up 164% from 2019 levels. Without reinsurance, most of the underwriting income embedded in those figures flows directly to third parties.

The core advantage reinsurance provides:

- Captures underwriting profit instead of surrendering it to the administrator

- Builds a reserve fund the dealer controls and can invest

- Creates a tax-advantaged structure for retained earnings

- Shifts claims risk management to the dealer's own company

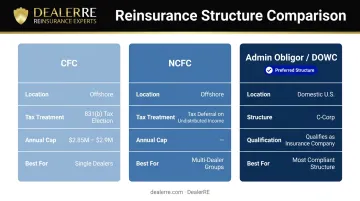

Reinsurance Structures Compared

| Structure | Location | Tax Treatment | Best For |

|---|---|---|---|

| CFC (Controlled Foreign Corporation) | Offshore | 831(b) election — premiums largely tax-free; only investment income taxed. Annual cap: $2.85M (2025), $2.9M (2026) | Single dealers below the premium cap |

| NCFC (Non-Controlled Foreign Corporation) | Offshore | Tax deferral on undistributed income | Multi-dealer groups; lower capitalization requirements |

| Admin Obligor / DOWC (Dealer-Owned Warranty Company) | Domestic (US) | Qualifies as an insurance company for federal tax purposes; domestic C-Corp | U.S. dealers seeking maximum compliance; DealerRE's primary structure |

The Admin Obligor model is widely considered the most compliant structure available to U.S. dealers today. The dealer's company serves as the named obligor on F&I contracts sold to customers, backed by an A-rated insurer — without being regulated as an insurance company itself. DealerRE specializes in setting up and administering this structure.

How Dealer Reinsurance Works: Step by Step

Here's how premium flows from a customer purchase through to dealer profit.

Step 1: Product Sale and Premium Collection

A customer buys a vehicle service contract or GAP policy at the dealership. The full retail premium is collected. After the administrator's fee and reserve for expected claims, a portion of that premium is ceded (transferred) into the dealer's own reinsurance company rather than retained entirely by the third-party provider.

The dealer's F&I gross profit on the transaction doesn't change — only where the underwriting profit lands after the sale.

Step 2: Reserve Management and Claims Funding

The reinsurance company holds reserves to fund claims as they arise. In the admin obligor structure, the dealer's company is the contractually named obligor on each F&I contract — meaning the dealer controls:

- How quickly claims are reviewed and approved

- Which repair facilities are authorized

- How customer disputes are handled

Claims control also shapes the customer experience directly. When a customer has a VSC claim, the dealer's service drive handles it — not a distant third-party call center. That distinction influences whether that customer returns for their next vehicle.

Step 3: Surplus Distribution and Capital Access

As premiums accumulate and claims are paid over the life of the contracts, any remaining surplus belongs to the dealer's company. Once reserves exceed required thresholds, excess funds can typically be accessed via distributions or loans against the accumulated balance.

That capital is the dealer's to deploy across a range of priorities:

- Floor plan balances and auction inventory purchases

- Facility improvements and dealership reinvestment

- Personal investments such as real estate or retirement accounts

Managing a reinsurance company alongside a dealership adds real administrative weight. DealerRE handles that backend — legal filings, tax returns, compliance monitoring, monthly financial statements, and annual reporting — so dealers stay focused on the sales floor.

How Floor Plan Financing and Dealer Reinsurance Connect for Profit

The Profitability Squeeze Dealers Are Facing

Floor plan and front-end gross are both moving in the wrong direction simultaneously:

- New vehicle front-end gross fell 14.4% year-over-year in Q1 2025

- New vehicle gross profit declined for 9 consecutive quarters through mid-2024

- Used vehicle front-end gross was $1,642 per unit in Q1 2025 — thin by any measure

- The annualized pre-tax profit impact from rising floor plan costs reached approximately $240,000 per franchised dealership in 2023

F&I has become the primary profit center holding dealerships together, accounting for an estimated 25–30% or more of total dealership gross profit. In the traditional model, the administrator keeps the underwriting income while the dealer keeps only the commission. Reinsurance recaptures what's being left behind.

The Reinvestment Cycle

Once premiums accumulate inside the dealer's own reinsurance company, that surplus becomes deployable capital. Common uses include:

- Paying down floor plan balances to reduce lender dependency

- Purchasing auction inventory outside the floor plan line

- Funding facility upgrades or service department expansion

- Building personal wealth through real estate, retirement accounts, or education funding

DealerRE has helped over 400 dealers nationwide build admin obligor programs. Some clients have reported accumulating six figures in underwriting profit annually — capital that had previously gone straight to a third-party provider.

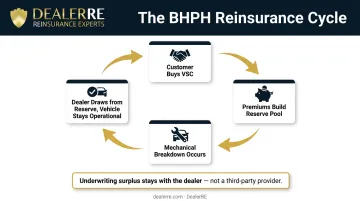

The BHPH Application

For Buy Here Pay Here dealers, reinsurance addresses a compounding risk that other dealer types don't face at the same scale. The average U.S. passenger car is now 14 years old, and the average repair costs $838 — with major component failures like fuel injectors or fuel pumps exceeding $1,125.

A mechanical breakdown on a BHPH vehicle doesn't just create a repair bill — it creates a payment default risk. A customer who can't drive to work stops paying, which turns one mechanical failure into a collection problem and potentially a repossession loss on the same unit.

DealerRE's BHPH reinsurance programs are structured around this reality. When customers purchase VSCs, the premiums build a customer-funded reserve pool. When the car breaks down, the dealer draws from that pool — keeping the vehicle operational and the customer making payments. The underwriting profit from premiums exceeding claims stays in the dealer's company rather than flowing to an outside provider.

Common Misconceptions About Floor Plan and Reinsurance

"Curtailment only matters for slow-moving units"

Every vehicle on a floor plan accumulates daily holding costs from day one. Curtailment fees are an additional layer on top of ongoing interest — not a replacement for it. Dealers who don't track aging aggressively often discover their true cost-per-unit is significantly higher than their gross profit calculation reflects.

"Reinsurance is too risky or only for large groups"

This is the most persistent misconception DealerRE encounters. The admin obligor structure is backed by A-rated insurers, meaning the dealer is never solely on the hook for claim obligations. If obligations cannot be met, ultimate liability rests with the direct writing insurance company. The dealer's downside is limited to formation costs plus accumulated earnings.

Programs are structured and profitable for independent dealers — including operations selling 30+ units per month. Most apprehension traces back to outdated experiences with poorly structured programs or underqualified administrators, not a flaw in the structure itself.

"Floor plan and reinsurance are separate issues"

Treating them in silos is the most expensive mistake. Floor plan is a recurring cost that compounds daily. Reinsurance generates a capital pool that accumulates over time and can be deployed against exactly that cost. Dealers who connect these two programs gain three specific advantages:

- Reduced lender dependency as reinsurance capital offsets borrowing needs

- Equity that builds over time rather than being paid to a third-party provider

- A profit stream that doesn't rise and fall with unit sales volume or market shifts

Frequently Asked Questions

What is dealer floor plan financing?

Floor plan financing is a revolving credit line specific to auto dealers, used to purchase vehicle inventory and repaid as each vehicle sells. Think of it as a credit card secured by the vehicles themselves: the credit replenishes with each sale rather than following a fixed repayment schedule.

What is dealer reinsurance?

Dealer reinsurance is a program where the dealer owns a company that captures the underwriting profits from F&I products like vehicle service contracts and GAP insurance — profits that would otherwise go entirely to a third-party insurer or administrator. Instead of paying those margins out, the dealer keeps them.

What is an admin obligor reinsurance program?

In an admin obligor structure, the dealer's own company is the named obligor on the F&I contracts sold to customers, backed by an A-rated insurer. The dealer controls claims decisions and the customer experience, while the insurer provides a financial backstop that limits the dealer's downside exposure.

What F&I products can be included in a reinsurance program?

Common products include vehicle service contracts, GAP insurance, collateral protection insurance (CPI), debt cancellation coverage (DCC), and ancillary products like tire and wheel, windshield repair, and door ding protection. The right product mix depends on the dealer's volume, inventory profile, and customer base.

Can reinsurance earnings fund floor plan or other dealership expenses?

Yes. Surplus accumulated in a dealer-owned reinsurance company can be accessed via distributions or loans against the account and deployed for any business or personal purpose, including floor plan payments, inventory purchases, facility investments, or retirement planning.

Is dealer reinsurance regulated and compliant?

Admin obligor structures are properly regulated under U.S. insurance law. The NAIC maintains regulatory frameworks for captive insurance companies across all 50 states. Working with an experienced administrator that manages legal filings, compliance, and tax returns is essential. DealerRE handles all of that on behalf of its dealer clients, keeping programs both compliant and profitable.