A Controlled Foreign Corporation (CFC) — also called a PARC, or Producer-Affiliated Reinsurance Company — changes that equation. Instead of paying third parties to carry the risk on products your dealership sold, you own the reinsurance entity yourself. The underwriting profits stay with you, and the tax treatment on distributions is structured to be far more favorable than ordinary dealership income.

This guide breaks down exactly how CFCs work, what the tax advantages look like under current law, how they compare to other profit participation structures, and what the setup process actually involves. Whether you're a franchise dealer, independent, or BHPH operation, if you're currently selling F&I products through a third-party provider, there's a strong case that you're leaving money on the table.

TL;DR

- A CFC (PARC) is a dealer-owned offshore reinsurance company that captures F&I underwriting profits rather than sending them to third parties

- Under IRC §831(b), qualifying CFCs pay tax only on investment income — not underwriting profits — up to $2.85M in annual premiums (2025)

- The Section 962 election taxes CFC distributions at the 21% corporate rate instead of ordinary income rates up to 37%

- Assets held in the CFC trust are invested, generating additional income while reserves accumulate

- DealerRE has helped 400+ dealers run these programs since 1994, managing all filings, tax returns, and renewals

What Is a CFC and How Does It Work for Auto Dealerships?

A Controlled Foreign Corporation, as defined under IRC Section 957, is any foreign corporation where U.S. shareholders owning 10% or more of the voting stock collectively hold more than 50% of the total voting power or value. For auto dealers, this means an offshore reinsurance company that you own and control — structured to capture a portion of the premium generated from F&I products sold at your dealership.

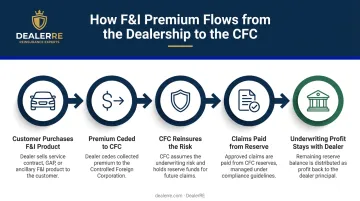

How the Premium Flow Works

When a customer purchases an F&I product — a vehicle service contract, GAP coverage, tire and wheel protection, or another ancillary product — a portion of that premium is "ceded" into your CFC. The CFC reinsures the underlying risk. When claims don't exhaust the reserve, the remaining underwriting profit belongs to your company, not a third-party administrator.

DealerRE structures these as admin obligor programs: your reinsurance company becomes the obligor on the service contracts sold to customers. All funds ceded are placed in a U.S.-based trust account — nothing is held offshore.

A Trust Agreement between the underwriting insurance company, your reinsurance company, and the Trust Company defines each party's responsibilities and governs withdrawal rules.

Dealers own 100% of their CFC and, as owner, officer, and director, can direct investment decisions (once reserves exceed 125% of unearned premiums), approve distributions, and access accumulated surplus.

CFC vs. PARC: The Same Thing

If you've read about dealer-owned reinsurance, you've likely seen multiple acronyms referring to the same structure. All three describe a dealer-owned, offshore-domiciled reinsurance entity subject to U.S. federal income taxes:

- CFC (Controlled Foreign Corporation) — the IRS classification

- PARC (Producer-Affiliated Reinsurance Company) — the industry-standard term

- PORC (Producer-Owned Reinsurance Company) — an alternate used by some providers

DealerRE typically recommends formation in the Turks and Caicos Islands, which offers established insurance regulations, minimal capital requirements, and allows all trust assets to remain in the United States.

Compliance note: U.S. shareholders of a CFC must file Form 5471 annually with their income tax return. DealerRE's administrator, Assured Vehicle Protection (AVP), handles this along with the annual Form 1120-PC corporate tax return and all renewals — removing the administrative burden from your dealership team entirely.

The CFC Tax Advantages Every Auto Dealer Should Know

The tax case for a CFC comes from three distinct angles: what happens at the entity level, what happens when you receive distributions, and what happens to the assets while they sit in reserve.

IRC §831(b): The Core Entity-Level Benefit

Under the small insurance company election, a qualifying CFC pays federal tax only on taxable investment income — underwriting profits are excluded from the tax base entirely. For 2025, the annual premium threshold is $2.85 million, rising to $2.9 million in 2026 per IRS Rev. Proc. 2025-32.

This is the primary engine of the structure. Profits from F&I product underwriting aren't taxed at the entity level as long as net written premiums stay within the cap.

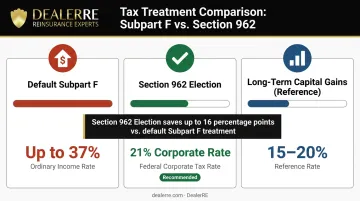

Distribution Tax Treatment: Section 962 Election

When income flows from a CFC to U.S. shareholders, the default treatment under Subpart F rules is ordinary income — potentially taxed at rates up to 37% for individual shareholders.

Individual shareholders can avoid that default by making an IRC Section 962 election, which taxes Subpart F inclusions at the 21% corporate rate and also permits indirect foreign tax credits under Section 960.

The rate difference is significant:

| Tax Treatment | Rate |

|---|---|

| Ordinary income (default, no election) | Up to 37% |

| Section 962 corporate rate election | 21% |

| Long-term capital gains (reference) | 15–20% for most taxpayers |

The 962 election doesn't convert income character to capital gains — but moving from 37% to 21% on Subpart F income is a meaningful difference. The decision typically hinges on the shareholder's overall income picture and whether foreign tax credits are available to reduce the 21% further.

Investment Income Inside the Trust

The tax advantages don't stop at the entity and distribution levels — the reserve assets themselves generate returns while they wait. Key mechanics:

- Initial reserves go into conservative government bonds per regulatory guidelines

- Excess funds above 125% of unearned premiums can be invested more aggressively at the owner's direction

- Manufacturer warranties often cover early-year claims, letting reserve balances compound through investment returns before meaningful claims materialize

- All investment income belongs to your reinsurance company, not a third-party provider

The QBI Deduction Layer

The One Big Beautiful Bill Act (OBBBA) made the 20% Qualified Business Income deduction under IRC §199A permanent for tax years beginning after December 31, 2025. For dealerships structured as S-corps, LLCs, or partnerships, this deduction can layer on top of CFC tax planning.

One important boundary: the QBI deduction applies to domestic pass-through entity income, not to the CFC itself, which is a foreign corporation. C-corp dealerships are not eligible for QBI.

What Dealers Can Actually Do with CFC Income

DealerRE clients have put accumulated CFC earnings to work in several ways:

- Purchase real estate — using distributions as down payments or acquisition capital

- Fund children's college education — redirecting what would have been ordinary dealership income into education accounts

- Buy watercraft and personal assets — accessing wealth that was previously flowing to third-party warranty companies

- Reinvest in the dealership — upgrading facilities, expanding inventory, or funding operational improvements on favorable terms

The reinvestment option stands out for cash-flow management. F&I profits that once left the dealership ecosystem can flow back as working capital, funded through your own reinsurance surplus rather than borrowed at market rates.

Multi-Entity Strategy for Dealer Groups

A single CFC has the $2.85M annual premium cap under §831(b). Dealer groups generating more premium than that need a strategy. One approach is the NCFC structure (Non-Controlled Foreign Corporation), which carries no annual premium limit — discussed in the next section. Another is careful structuring across related entities, but dealers must be aware of the controlled group aggregation rules under §831(b)(2)(C)(i).

Under these rules, premiums across entities with more than 50% common ownership must be aggregated toward the single cap. Family attribution rules under IRC Sections 267(b) and 707(b) also apply, meaning spouses, siblings, ancestors, and lineal descendants can be treated as related parties. A tax advisor experienced in CFC structures is essential before pursuing a multi-entity approach.

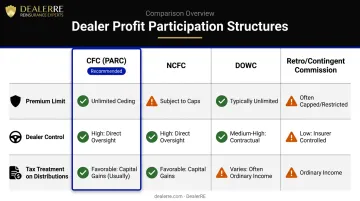

CFC vs. Other Profit Participation Structures

Most dealers encounter four main structures. Here's how they compare:

| Structure | Premium Limit | Dealer Control | Tax Treatment on Distributions |

|---|---|---|---|

| CFC (PARC) | $2.85M/year (§831(b)) | Full ownership & control | Subpart F ordinary income; 962 election at 21% |

| NCFC | No annual limit | Limited (board-managed) | Similar Subpart F treatment |

| DOWC (Dealer Owned Warranty Co.) | N/A | Full control, domestic | Accelerated tax deductions, domestic structure |

| Retro/Contingent Commission | N/A | No entity ownership | Ordinary income; simpler but lowest return |

The NCFC suits very large dealership groups that have exhausted CFC premium capacity. Dealers purchase preferred shares in a multi-dealer offshore entity — there's no annual premium cap, but operational control is limited and losses from other dealers in the pool can reduce your fund's returns.

The Retro plan requires no upfront investment. Earnings distribute based on underwriting performance, but payouts are ordinary income — and returns typically run lower than the CFC structure.

The CFC remains the default recommendation for most dealers: it offers full ownership control, favorable entity-level tax treatment via §831(b), and a complete annual compliance structure through an IRS-filed corporate return. Over 90% of the top 100 dealer groups already use some form of reinsurance — the CFC is the most widely adopted structure among them.

How to Set Up a Dealer-Owned CFC

Setting up a dealer-owned CFC involves five distinct phases. DealerRE handles the administrative and regulatory complexity — dealers provide direction, not legwork.

High-Level Setup Steps

- Business analysis — DealerRE reviews F&I volume, product mix, and financial goals to recommend the right structure. The decisions made here affect long-term tax efficiency, claims performance, and wealth accumulation.

- Entity formation — Your offshore reinsurance company is formed (typically in the Turks and Caicos Islands) under regulations that allow minimal startup capital while keeping all assets U.S.-based.

- Trust account establishment — A Trust Agreement is executed between the underwriting insurer, your CFC, and the U.S.-based Trust Company, securing your reserves in a domestic account.

- F&I product selection — You determine which products to reinsure: vehicle service contracts, GAP, CPI, DCC, ancillary products, or the full portfolio.

- First premium cession — Premiums begin flowing into your trust account, and reserve investment starts from the first deposit.

Industry sources indicate formation can take up to six months depending on domicile, regulatory licensing, and program complexity — though working with an experienced administrator shortens the timeline considerably.

Ongoing Administration

After setup, DealerRE's administrator (AVP) handles:

- Annual Form 1120-PC tax return preparation

- Monthly financial statements on all reinsurance operations

- Claims adjudication

- License renewals and regulatory filings

- Performance reports and loss projections

DealerRE meets with owners periodically to review financial direction and program performance. That keeps the dealer focused on the store — and the CFC's tax and profit advantages working in the background.

Is a CFC the Right Move for Your Dealership?

If you're selling F&I products through a third-party provider and generating more than 30 contracts per month, you're almost certainly paying underwriting profits to someone else that could be captured in your own structure.

Average F&I gross profit per vehicle retailed was $2,401 in Q2 2024 and $2,339 in Q4 2024 for publicly owned dealerships, according to Haig Partners. With the nation's 16,990 franchised dealers selling over 16 million vehicles annually, the aggregate underwriting profit pool is substantial — and most of it flows to third parties.

That profit opportunity extends across dealer types. CFC programs work for franchise dealers, independent retailers, and BHPH operations alike. In the BHPH space specifically, the structure reinsures:

- Collateral Protection Insurance (CPI)

- Debt Cancellation Coverage (DCC)

- Vehicle service contracts

- Limited warranties

This builds a customer-funded reserve that protects the dealer's portfolio from mechanical and insurance losses.

DealerRE has helped more than 400 dealers nationwide build and manage profitable reinsurance programs since 1994 — with clients recognized as National Quality Dealer of the Year and NIADA board members. Contact DealerRE at dealerre.com or (804) 824-9533 to model the potential tax savings and investment income for your specific F&I volume.

Frequently Asked Questions

What are dealer taxable fees?

Dealer taxable fees typically refer to charges dealers collect — such as documentation fees, financing charges, or administrative fees — that may be subject to income tax or sales tax depending on jurisdiction and structure. These are distinct from CFC underwriting income, which is governed by Subpart F rules and §831(b) at the entity level.

What is a CFC in auto dealership reinsurance?

A CFC (Controlled Foreign Corporation) is an offshore reinsurance company owned and controlled by the dealer, typically domiciled in a jurisdiction like the Turks and Caicos Islands. It captures F&I underwriting profits and investment income that would otherwise flow to a third-party provider, with tax treatment governed by IRC §831(b).

How are CFC distributions taxed for auto dealers?

CFC income flows to U.S. shareholders as ordinary income under Subpart F rules. Individual shareholders can make a Section 962 election to be taxed at the 21% corporate rate rather than individual rates up to 37%. A CPA experienced in CFC structures can help determine the most advantageous approach.

What is the annual premium limit for a dealer CFC?

The §831(b) annual premium cap is $2.85 million for 2025 and $2.9 million for 2026, adjusted for inflation in $50,000 increments. Dealers exceeding this threshold can consider an NCFC structure for overflow premium, though controlled group aggregation rules apply to related entities.

Can independent and BHPH dealers set up a CFC?

Independent and BHPH dealers can both participate in CFC programs. In the BHPH space, the structure reinsures CPI, debt cancellation coverage, vehicle service contracts, and limited warranties — protecting the dealer's portfolio from mechanical breakdown and insurance losses.

How long does it take to set up a dealer-owned reinsurance CFC?

Formation can take up to six months depending on entity domicile, regulatory licensing, and program complexity. Working with a full-service partner like DealerRE speeds the process significantly, as they manage all entity formation, trust agreements, legal forms, and regulatory filings for the dealer.