Introduction

Dealer-owned reinsurance has existed for over 30 years, yet most dealers evaluating a Controlled Foreign Corporation (CFC) structure still struggle to find a straight answer on what it actually costs to get started. Setup fees, administrative expenses, and capitalization requirements vary widely — and that uncertainty stops some dealers from moving forward on a structure that could return significant underwriting profit.

CFC setup costs depend on your provider, program structure, F&I production volume, and whether administration is bundled or billed separately. This article breaks down what to expect across setup fees, recurring costs, key pricing factors, and the budgeting mistakes that catch dealers off guard.

Key Takeaways

- CFC setup fees typically run $5,000–$6,000 with minimal precapitalization — the lowest entry point of any reinsurance structure

- Ongoing costs include administration fees, tax filings, compliance management, and claims handling — and vary by provider

- Single-rooftop or sole-owner dealers with lower F&I volume generally face the lowest total costs

- The cheapest setup rarely returns the most — know which services are bundled versus billed separately before deciding

How Much Does CFC Reinsurance Setup Cost?

CFC setup does not carry a single fixed price. Costs depend on the provider, services bundled into the program, and the dealer's F&I production level. Many smaller dealers mistakenly believe reinsurance is prohibitively expensive, when in reality, CFC programs are designed to be accessible even for moderate-volume stores.

Dealers run into trouble when they underbudget for annual compliance, select low-fee providers with poor claims management, or discover hidden fees that erode profit over time. The tiers below break down what each investment level typically covers—so you can evaluate the full cost before committing to a provider.

Typical Cost Ranges

Entry-level CFC setup ($5,000–$6,000 one-time):

This range covers the core formation work needed to get a CFC legally operational. Industry data from the mid-2010s placed turnkey formation costs around $4,000; current pricing reflects modest increases for IRS filing complexity and domicile registration requirements.

Typically includes:

- CFC entity formation

- Offshore or tribal domicile registration

- IRS filings (Section 953(d) and Section 831(b) elections)

- Initial corporate documentation

What this usually excludes:

- Ongoing administration and compliance management

- Annual tax return preparation

- F&I training and menu development

- Claims processing services

Mid-range CFC program ($7,000–$15,000 total first-year cost):

Programs in this tier bundle full-service administration—claims adjudication, compliance management, performance reporting, and staff training. The higher cost reflects comprehensive support rather than just entity formation. These programs often eliminate surprise fees by including services that entry-level providers charge for separately.

High-end or multi-CFC structures ($15,000+):

Larger dealer groups may form multiple CFCs for family succession planning or to exceed the annual premium cap (more on this below). Each entity carries its own setup and administrative costs. This tier is most appropriate for groups writing significant net premium annually or those with complex ownership structures.

Key Factors That Affect CFC Reinsurance Setup Cost

CFC pricing is shaped by structural, operational, and provider-specific factors. Understanding these helps dealers evaluate proposals from different reinsurance partners on equal footing.

Annual F&I Production Volume

The IRS Section 831(b) election allows CFC underwriting profits to grow tax-free, but only up to an annual net premium cap. According to IRS Revenue Procedure 2024-40, the cap is $2.85 million for 2025 and $2.9 million for 2026. The cap was doubled from $1.2 million to $2.2 million by the PATH Act of 2015 (effective January 2017) and increases with inflation in $50,000 increments.

Dealers approaching or exceeding this threshold may need:

- Multiple CFCs to continue capturing tax-advantaged profit

- A Super CFC structure that uses retail accounting and net operating losses instead of the 831(b) election

- A different structure entirely, such as a DOWC

Each option directly impacts total cost and administrative complexity.

Scope of Administrative Services Included

The difference between providers often lies in what's bundled versus what's billed separately:

Unbundled providers charge a low formation fee but bill separately for:

- Tax return preparation (Form 1120-PC)

- Compliance filings and regulatory reporting

- Claims adjudication and management

- Performance reporting and financial analysis

Full-service providers cover all legal forms, filings, tax returns, renewals, training, claims handling, and performance reporting under one fee. The upfront cost may appear higher, but total annual cost is typically lower. DealerRE, for example, operates this way — no hidden fees, with claims adjudication and F&I training included from day one.

Provider Experience and Program Quality

A lower-cost setup paired with weak claims adjudication can cost far more in eroded underwriting profits than whatever was saved on the setup fee. Provider track record, claims controls, and F&I training depth all directly affect what the dealer actually keeps at year-end.

Quality indicators to evaluate:

- Years administering dealer CFC programs

- Claims adjudication process and controls

- Depth of F&I training and ongoing coaching

- Transparency around fees and withdrawals

- References from similar-sized dealers

Ownership Structure and Succession Planning Needs

Dealers who plan to use the CFC for succession planning or talent retention—such as adding family members or key managers as partial owners—may need to establish additional CFCs with varying ownership structures. Each adds incremental setup and administration cost, but can deliver significant estate planning and retention benefits.

Net vs. Retail Accounting Method

The accounting method determines how much premium capital flows into the structure and sets the baseline for comparing a CFC against a Super CFC or DOWC.

| Structure | Accounting Method | Premium That Enters | Key Trade-off |

|---|---|---|---|

| Traditional CFC | Net accounting | Wholesale portion only (after admin and carrier fees) | Lower complexity; subject to 831(b) cap |

| Super CFC | Retail accounting | Full premium | Larger NOLs, no 831(b) cap; higher administrative overhead |

The right choice depends on your annual F&I volume, tax strategy, and tolerance for administrative complexity — all of which should factor into how you compare provider proposals.

Complete Cost Breakdown of Setting Up a CFC

The total cost of a CFC reinsurance program goes well beyond the initial setup fee. Dealers who focus only on formation cost often underestimate their annual program expense.

One-Time Setup Costs

Formation costs typically include:

- CFC entity formation and corporate documentation

- Offshore or tribal domicile registration (Turks & Caicos, Anguilla, Delaware Tribe, etc.)

- IRS Section 953(d) filing (to be taxed as a U.S. domestic insurance company)

- IRS Section 831(b) election (small insurance company tax treatment)

- Federal Tax ID procurement

- Reinsurance treaty negotiation and execution

- Custodial Trust Agreement establishment

Critical difference from DOWC: CFCs require minimal precapitalization—Automotive Assurance Group recommends at least $5,000 as a minimum capitalization. This is a significant difference from DOWCs, which typically require approximately $50,000 in initial capitalization, and significantly more in some states.

Ongoing Annual Administration Fees

Recurring administration costs vary significantly by provider and often represent where hidden costs emerge in lower-tier programs:

- Annual corporate tax return preparation (Form 1120-PC)

- Claims adjudication and processing

- Compliance management and regulatory filings

- Performance reporting and financial analysis

- Bookkeeping and financial recordkeeping

Full-service administration can be the difference between a profitable and a poorly managed program. Dealers should ask providers exactly what's included in annual fees and what's billed separately.

F&I Training and Staff Development

Some providers include F&I training, menu development, and ongoing coaching as part of their program fee, while others charge separately. This investment directly impacts how much premium flows into the CFC—a well-trained F&I team generates higher product penetration, which funds the reinsurance company more effectively.

Investment Management and Trust Costs

That premium volume flows directly into a trust account, where CFC assets are typically invested in conservative instruments like government bonds or index funds. Automotive Assurance Group cited an average custodial/investment management fee of approximately 0.50% (50 basis points) for managing brokerage accounts holding reinsurance trust assets.

One tax point worth understanding: Investment income is the only category of CFC income taxed annually under the Section 831(b) election—underwriting profit is excluded from taxable income until withdrawn. According to IRS Form 1120-PC instructions, companies making the 831(b) election complete Schedule B (Taxable Investment Income) and do not include underwriting income in their tax computation.

Periodic or Contingency Costs

Additional costs can arise from:

- Recapitalization requirements if underwriting performance reduces trust funds below minimum levels

- Multi-CFC restructuring as volume grows beyond the 831(b) cap

- Transitioning to a Super CFC or DOWC when production exceeds the premium ceiling

Before signing with any provider, ask for a written fee schedule that covers each of these scenarios. Knowing the triggers and estimated costs in advance makes program growth manageable rather than disruptive.

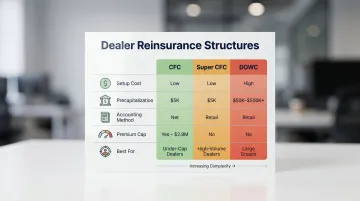

CFC vs. DOWC vs. Super CFC: Cost Differences at a Glance

The three most common dealer reinsurance options differ not just in tax treatment but in upfront capital requirements, ongoing costs, and long-term profit capture. If you're evaluating which structure fits your dealership, understanding where the costs diverge is the fastest way to narrow your options.

CFC (Controlled Foreign Corporation)

The CFC is the lowest-barrier entry point into dealer-owned reinsurance, making it the most common starting structure for independent and franchise dealers alike.

Cost highlights:

- Lowest upfront cost (~$5,000–$6,000 setup)

- Minimal precapitalization (as low as $5,000)

- Moderate ongoing administration costs

How it works:

- Uses net accounting — only wholesale premium enters the structure

- Subject to the Section 831(b) annual premium cap ($2.9 million for 2026)

- Taxed only on investment income annually

- Best for dealers writing under the premium cap

DOWC (Dealer-Owned Warranty Company)

Cost highlights:

- Highest upfront cost of the three structures

- Capitalization averages approximately $50,000 administratively; some states require significantly more (Florida requires $500,000 according to Agent Entrepreneur)

- Significant ongoing compliance costs for state licensing, solvency requirements, and forms management

The higher cost reflects what the dealer gains: full control and 100% profit retention.

How it works:

- Uses retail accounting — full premium enters the structure

- Dealer is the obligor and retains 100% of underwriting and investment income

- No annual premium cap

- Requires state licensing in every state where policies are sold

- Best for large dealer groups with the infrastructure to manage compliance complexity

Super CFC

The Super CFC keeps setup costs close to the traditional CFC while removing the premium cap — making it the natural upgrade path for dealers whose volume has outgrown the 831(b) limit.

Cost highlights:

- Similar low setup cost to a traditional CFC

- Higher administrative complexity than a standard CFC

- No annual premium cap

How it works:

- Uses retail accounting — full premium enters the structure

- Achieves tax deferral through Net Operating Losses (NOLs) rather than the 831(b) exclusion

- Not subject to the 831(b) premium cap

- Forms in under two weeks according to Elite FI Partners

- Best for dealers who have outgrown the traditional CFC's premium cap

Setup cost is just the starting point — ongoing administration, capitalization, and state licensing requirements drive the real long-term cost differences between these structures.

What Most Dealers Miss When Budgeting for a CFC

Three budget blind spots trip up dealers more often than any others:

Sticker price vs. total cost. A $5,000 setup with a provider that charges separately for tax returns, compliance filings, and claims handling often runs higher over three years than a full-service program with a slightly higher initial fee. Calculate total three-year cost, not just year-one expense.

Undervaluing claims management. Claims adjudication quality directly affects the underwriting profit flowing back to the dealer. A provider that mismanages claims erodes the reserve, reduces distributions, and can trigger recapitalization requirements — losses that dwarf any setup savings.

Ignoring the $2.9 million premium cap. Dealers who don't account for F&I growth trajectory may hit the annual cap within a few years. Restructuring or forming additional entities after the fact is costly — and avoidable with proper planning upfront.

Conclusion

CFC reinsurance setup is accessible for most auto dealers, with formation costs typically starting around $5,000–$6,000 and minimal precapitalization. The true cost and value of the program comes down to ongoing administration quality, claims management expertise, and whether all services are bundled transparently or billed piecemeal.

A partner that handles all filings, compliance, training, and reporting under one transparent fee structure turns setup costs into a foundation for sustained F&I profit—not just a paper entity. Reach out to DealerRE to find out exactly what your program would cost to launch and what it could realistically return.

Frequently Asked Questions

What is considered a Controlled Foreign Corporation?

A CFC is an offshore corporation owned and controlled by U.S. shareholders (in this case, the auto dealer) that reinsures F&I contracts. It elects to be taxed as a U.S. taxpayer under IRS Section 953(d), paying tax only on investment income rather than underwriting profit.

What is the difference between CFC and Super CFC?

A traditional CFC uses net accounting and the Section 831(b) election, capping annual premium at $2.9 million for 2026. A Super CFC uses retail accounting and tax deferral through Net Operating Losses, allowing it to scale beyond the premium cap with no annual ceiling, but without the outright underwriting profit exclusion.

What is reinsurance at a dealership?

Dealer reinsurance is a structure where the dealer owns a company that assumes the risk on F&I products sold at their store. This allows the dealer to capture underwriting profits and investment income that would otherwise go to a third-party administrator or carrier.

Why is reinsurance so expensive?

CFC setup costs as little as $5,000–$6,000 with minimal precapitalization. The perception of high cost typically comes from providers who layer on hidden fees for administration, compliance, and claims handling that aren't disclosed upfront.

What are premiums in reinsurance?

In dealer reinsurance, premiums are the amounts paid by the F&I product buyer that are ceded (transferred) from the obligor into the dealer's reinsurance company. The CFC receives either net premium (after dealer commissions and fees) or full retail premium depending on the accounting method used.

What is FET in reinsurance?

FET (Federal Excise Tax) is a tax applied to certain reinsurance arrangements—specifically NCFCs (Non-Controlled Foreign Corporations)—at approximately 1% of reinsured premiums per IRC Section 4371. For most dealers, that difference alone justifies choosing a CFC structure over an NCFC from a cost standpoint.