Dealer-owned reinsurance flips that arrangement. The concept has been around since the 1950s, and today dealerships of all types — franchise stores, independent retailers, and Buy Here Pay Here operations — are using it to recapture income, build long-term assets, and gain real control over their F&I programs.

This guide walks through what dealer reinsurance actually is, when it makes sense to start one, and exactly how the process works — step by step.

TL;DR

- A dealer-owned reinsurance company lets your dealership collect premiums from F&I products and keep the underwriting profit instead of sending it to a third-party provider

- The admin obligor model is the dominant structure — your company becomes the obligor on contracts, backed by an A-rated insurer

- Minimum volume threshold is around 30+ cars per month; program value compounds as F&I sales accumulate over time

- A full-service administrator handles legal formation, compliance, claims, tax returns, and ongoing training

- Initial setup is fast; building meaningful reserve fund value takes months to years of consistent volume

What Is a Dealer-Owned Reinsurance Company?

A dealer-owned reinsurance company is a separate legal entity — owned by the dealer principal — that assumes a portion of the risk from F&I products sold at the dealership. In return, it collects the premiums that would otherwise flow to a third-party provider.

When a customer buys a vehicle service contract or GAP policy at your store, those premiums flow into your reinsurance entity rather than to a third-party provider. When claims occur, your company pays them. What's left after claims is yours.

That's the core of the model: instead of paying a third-party provider to carry the risk — and keep the profit — you own that entity yourself. The admin obligor structure is how most dealers put this into practice.

The Admin Obligor Structure Explained

Most dealer reinsurance programs today use an admin obligor (AO) structure, sometimes called a Dealer Owned Warranty Company (DOWC). Here's how it works in plain terms:

- Your reinsurance company becomes the administrator and obligor on service contracts and other F&I products

- An A-rated insurer provides the regulatory and financial backbone — consumers and regulators have confidence that claims obligations will be met

- Your company captures the underwriting profit and investment income that would otherwise go to a third party

Admin obligor structures are generally not regulated as insurance companies by the states where they operate — they assume risk through contractual obligations rather than insurance licenses. For dealers, that means a faster, less burdensome setup process than forming a traditional insurer.

What to Know Before You Start

Many dealers assume reinsurance is too complex or only viable for high-volume stores. Both assumptions are wrong — though there are practical realities worth knowing before you commit.

Your F&I Volume Is the Engine

A reinsurance company grows in value as premium reserves accumulate. That means results compound over time rather than appearing immediately. Dealers selling 30+ vehicles per month are generally viable candidates. Industry sources cite 20–25 service contracts per month as a practical starting threshold — smaller than most dealers assume.

DealerRE addresses the misconception directly: "The largest misconception is you must be very large in volume or that it costs a lot of money to get started. Neither are true."

You're the Owner, Not the Day-to-Day Operator

A program administrator handles claims adjudication, compliance, tax returns, financial reporting, and staff training. Your job is to stay engaged with performance reporting and understand what's driving results — not to manage every claim.

Three factors directly shape how profitable your program becomes:

- Product mix: which F&I products feed the program and at what penetration rates

- Loss ratios: the spread between premiums collected and claims paid

- Reserve fund investment: how accumulated reserves are invested while contracts remain active

Get a clear picture of all three before launch — they determine whether you're building equity or just moving money around.

Why Start Your Own Reinsurance Company?

The financial case is straightforward. When you sell F&I products through a third-party provider, you earn a flat commission. The provider keeps the underwriting profit and investment income — the money earned while holding reserves over the three-to-seven-year life of a typical contract.

With F&I gross profit per vehicle reaching $2,515 in Q2 2025 among publicly traded dealer groups, the volume of money flowing through dealer F&I departments — and out to third parties — has never been higher.

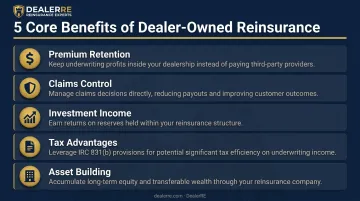

The Core Benefits

- Premiums flow into your reinsurance entity — after claims, what remains is yours, not a third-party provider's

- Influence how claims are processed, which protects your reserve fund's profitability and keeps repair work in your service department

- Reserve funds are invested during the contract period, generating income on top of underwriting profit

- Under IRC Section 831(b), P&C insurers with annual net premiums below ~$2.2 million may elect to be taxed only on investment income, with distributions at capital gains rates — consult a qualified tax advisor

- The reinsurance entity itself is a financial asset; dealers have used program earnings to fund real estate, college tuition, and reinvestment in operations

Who Is a Good Candidate?

These benefits compound over time, but they require the right foundation. The strongest candidates typically:

- Sell 30+ vehicles per month consistently

- Have a functioning F&I process with reasonable product penetration

- Want more than a flat commission on every deal

- Are willing to stay engaged with performance reporting over time

Average U.S. dealership penetration rates run around 40% for vehicle service contracts and 28% for GAP insurance. Dealers below these benchmarks should focus on improving F&I performance alongside — or before — entering reinsurance.

How to Start a Dealer-Owned Reinsurance Company — Step by Step

Setting up a dealer-owned reinsurance company is more straightforward than it sounds — especially with a full-service program administrator managing legal formation, compliance, and ongoing administration.

Step 1 — Evaluate Your F&I Volume and Product Mix

Before anything else, audit your current numbers:

- How many vehicles do you sell per month?

- What is your service contract penetration rate?

- What products does your F&I team currently sell, and at what volume?

Volume drives reserve accumulation. A dealer consistently selling 30+ units with reasonable F&I penetration will see the program build meaningful value over time. Getting excited about the concept before confirming you have enough F&I volume is the single fastest way to start a program that never gains traction.

Step 2 — Understand and Choose the Right Structure

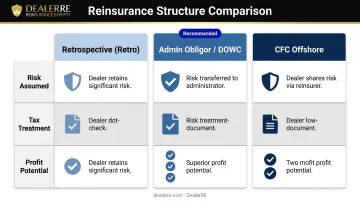

The admin obligor model is the right choice for most dealers who want maximum profit capture and control. Here's a quick comparison:

| Structure | Risk Assumed | Tax Treatment | Profit Potential |

|---|---|---|---|

| Retrospective (Retro) | None | Ordinary income | Lower |

| Admin Obligor / DOWC | Full contractual risk | Insurance company treatment | Higher |

| CFC (Offshore) | Reinsured risk | 831(b) election available | Higher |

Retros are simpler but provide only a performance-based bonus taxed as ordinary income. Admin obligor structures require entity formation but unlock underwriting profit, investment income, and favorable tax treatment.

The right structure depends on where you want the program to go — how aggressively you want to accumulate capital, what your tax planning objectives are, and whether you plan to reinvest profits or eventually distribute them.

Step 3 — Select a Reinsurance Program Administrator

The administrator is your operational partner for everything you don't want to manage yourself. Evaluate candidates on:

- Years of experience — this industry rewards longevity and track record

- Full-service vs. partial support — do they handle legal formation, compliance, claims, tax returns, and training, or just some of these?

- Fee transparency — are all costs disclosed upfront, with no hidden fees?

- F&I training quality — can they actually improve your team's product penetration?

- Reporting — will you receive monthly financials and performance analysis?

DealerRE has provided full-service administration since 1994, covering legal setup, claims adjudication through Assured Vehicle Protection (AVP), compliance management, tax returns, financial reporting, and both online and in-person F&I training for over 400 dealers nationwide. That full-service scope — not just one or two components — is what separates a true program partner from a vendor.

Step 4 — Set Up the Legal Entity and Fund the Company

Your reinsurance company must be a separate legal entity — your dealership's existing business entity cannot simply act as a reinsurance company. The domicile you choose affects capitalization requirements, regulatory obligations, and setup timeline.

Capitalization by jurisdiction:

| Domicile | Approx. Minimum Capital | Timeline |

|---|---|---|

| Turks and Caicos Islands | Low — $2,500–$25,000 range | Weeks |

| Nevis | No stated minimum | Days to weeks |

| Arizona (domestic) | ~$150,000 | ~6 months |

| Connecticut / Vermont (captive) | ~$250,000 | Varies |

Most program administrators, including DealerRE, use the Turks and Caicos Islands as the preferred domicile — regulations there were specifically designed for this type of company, capital requirements are minimal, and all assets remain in the United States in a domestic trust account. No funds are sent offshore.

The initial funding establishes the company's ability to meet claims obligations while reserve accumulation begins.

Step 5 — Integrate Products and Train Your F&I Team

The reinsurance company only generates value if F&I products are being sold consistently and effectively. This step covers two things:

Product menu alignment. Confirm which products your program covers — typically vehicle service contracts, GAP, collateral protection, and ancillary products like tire and wheel, door ding, windshield, and theft protection. Match your F&I menu to what your reinsurance entity will reinsure.

F&I team training. Staff need to know how to present products, handle objections, and maintain penetration rates. This isn't optional — it's the direct input that feeds reserve accumulation.

Quality administrators provide both in-person and online training. DealerRE's training program includes F&I development, in-person classes, online modules, and menu support. Parker Byrd, VP of DealerRE, spent time as both an F&I manager and salesman before joining the company — that hands-on dealership background shapes how the training is built and delivered.

Launching the reinsurance entity without simultaneously working on F&I process improvement is a setup for slow results. Entity formation takes weeks. Building the penetration rates that make it financially meaningful takes months of consistent execution.

Step 6 — Monitor Performance and Grow the Program

Once operational, the management cycle looks like this:

- Review monthly financials — track premiums ceded, claims paid, and reserve fund balance

- Monitor loss ratios — understand what's driving claims and whether adjustments are needed

- Evaluate reserve fund health — ensure the fund is growing at a pace consistent with contract volume

- Make product and pricing adjustments as needed based on performance data

Early years focus on stabilizing claims experience and building reserves. Over time, as contracts mature and reserve balances grow, investment income and underwriting profit begin compounding in a meaningful way.

Treating the reinsurance company as a "set it and forget it" asset is the most common long-term mistake. Dealers who review monthly reports, flag unusual loss ratios early, and refine their product mix consistently are the ones who see the largest reserve balances at year five and beyond.

Conclusion

Starting a dealer-owned reinsurance company is less about complexity and more about making the right structural choices, selecting a partner who handles the operational heavy lifting, and building a consistent F&I operation that feeds the program with premium volume.

The long-term value builds steadily for dealers who start early and stay consistent: underwriting profit capture, investment income, tax advantages, and asset accumulation all grow as the program matures. Dealers who have been running programs for years tend to say the same thing — they wish they'd started sooner.

If you're selling 30+ vehicles per month and want to stop giving away F&I profit to third-party providers, the next step is straightforward. DealerRE has been helping dealers set up and manage their own reinsurance programs since 1994 — handling the structure, compliance, administration, and training so you can focus on volume. Reach out to talk through whether your dealership is ready to start.

Frequently Asked Questions

What is the minimum capital for reinsurance?

Minimum capital requirements vary by structure and domicile. Offshore jurisdictions like the Turks and Caicos Islands allow formation with as little as $2,500–$25,000 in initial capital, while domestic options like Arizona require around $150,000. An experienced administrator can guide you through the specific requirements for your program structure and jurisdiction.

Are reinsurance companies profitable?

Dealer-owned reinsurance companies can be highly profitable when F&I product volume is sufficient and claims experience is managed well. Profit comes from three sources: underwriting profit retained after claims, investment income on reserve funds during the contract period, and proceeds from matured contracts.

What is the 80% rule in insurance?

The 80% rule is a property insurance coinsurance concept: policyholders must insure their property for at least 80% of its value, or claims payments are reduced proportionally. It has no bearing on dealer reinsurance programs, where profitability depends on the spread between premiums collected and claims paid.

How does a dealer-owned reinsurance company work?

Premiums from F&I products sold at your dealership are ceded to your reinsurance entity. When claims occur, your company pays them. The profit remaining after claims — plus investment income earned on reserves — stays in your company rather than going to a third-party provider.

What types of F&I products can be included in a dealer reinsurance program?

Typical products include vehicle service contracts, GAP insurance, collateral protection insurance, debt cancellation coverage, and ancillary products like tire and wheel, door ding, windshield repair, and theft protection. The exact product mix depends on your program structure and administrator.

How long does it take to set up a dealer-owned reinsurance company?

Offshore formation through a domicile like the Turks and Caicos Islands can take just weeks; domestic formation in Arizona historically runs around six months. The longer-term consideration is building reserve fund value, which grows steadily as F&I product sales accumulate.