The cost to start a dealer reinsurance company is not a single fixed number. It varies based on structure type, domicile, sales volume, and level of ongoing support. This article breaks down what those costs actually are, what drives them up or down, and how dealers can estimate the right budget for their operation.

Key Takeaways

- Startup costs range from $10,000–$30,000 for standard structures; domestic setups require additional capital

- Biggest cost drivers: legal formation fees, initial paid-in capital, ceding fees, premium taxes, and annual compliance costs

- Smaller and independent dealers can start leaner; higher-volume dealers may justify more complex setups with greater tax advantages

- Setup costs are low compared to the underwriting profits dealers lose by relying on third-party providers

How Much Does It Cost to Start a Dealer Reinsurance Company?

There is no universal price tag. Total cost depends on four key variables: the program structure chosen (Admin Obligor, CFC, or DOWC), the domicile of the company, dealer sales volume, and whether a full-service partner handles administration or the dealer manages it independently.

Two common pitfalls emerge when cost is misunderstood:

- Underbudgeting creates compliance gaps or undercapitalization, generating IRS exposure that far outweighs any upfront savings

- Overestimating causes dealers to delay entry, continuing to surrender underwriting profit to third-party providers

Entry-Level / Basic Setup

This tier represents a simple Admin Obligor or CFC structure with minimum initial capitalization. IRS Notice 2002-70 (often miscited as "TAM 2002-70") doesn't mandate a specific dollar minimum for paid-in capital, but requires that the entity's "primary and predominant business activity" be insurance. Based on program experience, most administrators recommend at least $5,000 as a floor, with capitalization scaled to starting risk.

Typical all-in year-one costs for this tier range from approximately $10,000–$13,000. This includes:

- Basic formation and attorney fees

- Minimum capital deposit

- First-year filing costs

- IRS 953(d) and 831(b) election filings

This tier does not include investment management, advanced tax strategies, or higher-volume risk modeling.

Best for: Lower-volume dealers testing the reinsurance model for the first time, or dealers starting with a single product category such as VSCs.

Mid-Range / Standard Setup

This tier represents a fully structured CFC or Admin Obligor program with adequate capitalization scaled to actual warranty volume, first-year ceding fees, premium taxes, and custodial/trust account fees.

All-in year-one cost range: approximately $18,000–$30,000.

Core components include:

- Legal formation and licensing

- Capitalization scaled to volume

- Ceding fees (first-year premium basis)

- Premium taxes

- Trust account setup and custodial fees

- Annual compliance and filings

Best for: Established dealers selling moderate F&I volume who want full underwriting profit participation and tax advantages.

Advanced / DOWC Structure

A Dealer Owned Warranty Company (DOWC) is a domestic insurance entity requiring significantly higher statutory capital. State minimums typically range from $250,000 to $1,000,000+ depending on domicile and scope of risk written.

Core components at this tier include:

- Statutory capital deposit (state-mandated minimum)

- Regulatory filing and domicile approval fees

- Legal formation, licensing, and ongoing compliance

- Actuarial reserve modeling and claims administration

- Trust or custodial account setup

Formation typically takes 3–6 months for regulatory approval, followed by a 12–24 month seeding period before full tax benefits activate. During that window, claims reserves must build to demonstrate actuarial adequacy.

Best for: High-volume dealers seeking maximum control, domestic domicile, and long-term tax efficiency. A well-run DOWC can reduce federal income tax liability on F&I-related income dramatically — potentially to near zero for decades.

Key Factors That Affect the Cost of Starting a Dealer Reinsurance Company

Pricing is shaped by structural, regulatory, and operational decisions. The variables below determine whether your startup costs are $5,000 or $250,000 — and whether the structure you choose actually fits your volume and tax situation.

Structure Type

Each structure carries a different cost profile. Here's how they compare:

| Structure | Startup Cost | Key Advantage |

|---|---|---|

| Retro/Bonus Program | Minimal | Low barrier to entry |

| CFC (Controlled Foreign Corp.) | Moderate | IRC §831(b): 0% tax on underwriting income up to annual cap |

| Admin Obligor | Moderate | Profit participation without full DOWC complexity |

| DOWC | Significant capital required | Maximum tax efficiency |

Structure selection should match the dealer's volume, tax situation, and time horizon — not just the lowest entry fee.

Domicile Choice

The country or state where the reinsurance company is domiciled affects licensing costs, ongoing compliance fees, and IRS treatment.

Common offshore domiciles for CFC structures:

- Turks and Caicos Islands (TCI): Tax-neutral environment with no direct taxes on profits, income, or capital gains. Governed by Insurance Ordinance 2019. Streamlined application processes and timely approvals make TCI the leading domicile for dealer CFC reinsurance.

Domestic DOWC domicile options:

- Vermont: $250,000 minimum capital (reduced from $500,000 in 2024)

- Tennessee: $250,000 minimum capital, approximately 30-day processing for complete applications

Warning: Non-compliant domicile workarounds can create downstream IRS exposure that far outweighs any upfront savings.

Sales Volume and Risk Level at Launch

Capital and reserve requirements scale directly with the number and value of F&I contracts being written. A dealer selling 10 service contracts per month has very different capitalization needs than one selling 100.

Undercapitalizing to reduce startup costs is one of the most common — and costly — mistakes dealers make. Key reasons adequate capitalization matters:

- The IRS evaluates whether capitalization matches the risks actually assumed

- IRS Notice 2016-66 flags inadequate capitalization as a primary compliance risk for 831(b) entities

- Undercapitalized entities face audit exposure that typically dwarfs whatever was saved at formation

Ceding Fee Structure of the Chosen Provider

Ceding fees are charged by the admitted fronting carrier for transferring risk and premium reserves to the reinsurance entity. In dealer reinsurance, the "admin fee" functions as the composite ceding fee — typically 20% or less of the product cost — but this varies widely by provider.

Even a small difference in ceding fees compounds significantly over years of operation. Some providers bundle these costs into administration fees while advertising "zero ceding fees." Always request full itemized fee disclosure before signing.

Complete Cost Breakdown: One-Time vs. Recurring Expenses

The total cost to start and operate a dealer reinsurance company goes beyond the formation fee. Dealers need to budget for both one-time startup costs and ongoing annual expenses.

Formation and Legal Fees (One-Time)

This covers:

- Attorney fees to create the company structure

- Reinsurance license (commonly offshore for CFC structures)

- Corporate documents and stock certificates

- Tax ID number

- IRS 953(d) filings

- 831(b) election

Typical cost range: $4,000–$20,000 depending on structure.

DealerRE manages all legal forms, filings, and company setup as part of their program, so dealers don't have to navigate this process alone.

Initial Paid-In Capital (One-Time)

The IRS requires reinsurance companies to have initial paid-in capital to be considered viable insurance entities (per IRS Notice 2002-70 and Notice 2004-65). No law mandates a specific dollar minimum, but industry guidance recommends at least $5,000 as a floor, with capitalization scaled to starting risk.

This capital sits in a trust account — it is not spent but seeds the company's reserves and backs its risk-bearing capacity.

Annual Compliance and Renewal Fees (Recurring)

These cover attorney and CPA fees for annual renewals, books and records maintenance, tax preparation, and annual regulatory filings.

Typical annual range: $3,800–$5,000 per year.

Full-service reinsurance partners handle all of this — DealerRE's program covers legal forms, tax returns, and annual renewals with no hidden fees.

Ceding Fees and Premium Taxes (Recurring)

Two recurring line items dealers should model carefully:

- Ceding fees: A percentage of the premium reserve ceded monthly to the dealer's reinsurance entity. The admin fee typically represents 20% or less of product cost.

- Premium taxes: Based on amounts the insurance company pays in the state of filing. Georgia's rate, for example, is 2.25% — reduced to 1.25% if 25% or more is invested in specified Georgia assets.

Both figures directly reduce retained underwriting profit, so accurate modeling at the outset matters.

Custodial/Trust Account and Investment Management Fees (Recurring)

The money manager overseeing the brokerage account holding premium reserves charges a custodial fee — typically around 50 basis points (0.5%) of assets managed.

Caution: Some investment managers also charge proprietary fund fees not disclosed upfront. Dealers should always request full fee disclosure from any investment manager before committing.

Reinsurance Structures and What Each One Costs

Four main structures are available to auto dealers, ranging from lowest cost and least control to highest cost and maximum control. Understanding where each one sits on that spectrum helps narrow down which fits your volume, budget, and timeline.

Admin Obligor (Dealer Held Warranty Company)

A practical and widely-used structure for dealers seeking profit participation without the full complexity of a DOWC. The dealer is structured as an administrative obligor on the contract, giving direct control over the customer experience and claims.

Cost profile: Moderate formation cost, lower capitalization requirements than DOWC, faster setup timeline.

CFC (Controlled Foreign Corporation)

Involves offshore formation and ceding costs, but offers IRC Section 831(b) tax advantages. For taxable years beginning in 2026, qualifying entities can write up to $2,900,000 in net written premiums and are taxed only on investment income — underwriting income is excluded from taxable income (effectively taxed at 0%).

Cost profile: Moderate formation cost, faster setup than DOWC, subject to 1.0% Federal Excise Tax on reinsured premiums.

DOWC (Dealer Owned Warranty Company)

Domestic US insurance entity requiring $250,000–$1,000,000+ in statutory capital depending on state domicile. Formation timeline: 3–6 months for regulatory approval, plus a 12–24 month seeding period before full tax benefits activate.

In exchange, claims paid create negative taxable income, potentially enabling decades of tax-advantaged operation.

Best suited for dealers consistently moving 100+ units per month who can commit to the capital outlay and multi-year runway required to realize the full tax advantage.

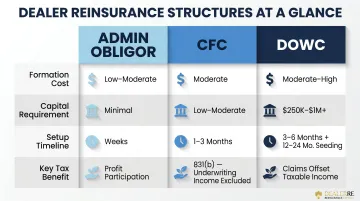

Here's how the three structures compare at a glance:

| Structure | Formation Cost | Capital Requirement | Setup Timeline | Key Tax Benefit |

|---|---|---|---|---|

| Admin Obligor | Low–Moderate | Minimal | Weeks | Profit participation |

| CFC | Moderate | Low–Moderate | 1–3 months | 831(b) — underwriting income excluded |

| DOWC | Moderate–High | $250K–$1M+ | 3–6 months + 12–24 mo. seeding | Claims offset taxable income |

Budgeting Mistakes Dealers Make — and How to Avoid Them

Treating Formation Fees as the Total Cost

The real financial picture includes recurring ceding fees compounding over years, annual compliance costs, premium taxes, and investment management fees. Dealers who budget only for setup and ignore year-two-plus operating costs are caught off guard.

The Cost of Delay

Every month a dealer continues without a reinsurance program is a month of underwriting profit flowing to a third-party provider. Every month a dealer continues without a reinsurance program is a month of underwriting profit flowing to a third-party provider. Those losses add up faster than most dealers expect.

Example calculation:

- Average VSC reserve per contract: $800

- Typical loss ratio: 50%

- Underwriting profit per contract: $400

- At 20 VSCs/month: $96,000 in additional annual net profit

- Over five years: $480,000

That gap widens every quarter a program launch gets pushed back.

The Right Way to Estimate a Budget

Once you understand what delay is costing you, building a realistic budget becomes straightforward. Follow this framework:

- Estimate your volume baseline — monthly contract count and average premium reserve per contract

- Match structure to your situation — the right program type depends on your volume and tax position

- Total your startup costs — formation fees, capital requirements, and first-year operating expenses

- Calculate your payback period — divide total cost by projected annual underwriting profit to set realistic expectations

DealerRE provides a no-cost dealer analysis that walks through each of these steps, helping you identify the right program structure and see a clear picture of projected returns before you invest.

Frequently Asked Questions

How do reinsurance firms make money?

Reinsurance companies earn money through underwriting profit (the difference between premiums collected and claims paid) and investment income generated by premium reserves held in trust accounts. Dealer-owned reinsurance companies return this profit to the dealer rather than to a third-party carrier.

What is the minimum capital requirement for a reinsurance company?

No specific dollar minimum is mandated, but industry guidance recommends at least $5,000 as a floor. IRS Notice 2002-70 and Notice 2004-65 require adequate paid-in capital relative to the risk assumed to qualify as a viable insurance entity.

How long does it take to set up a dealer reinsurance company?

Basic CFC or Admin Obligor structures can be formed in a matter of weeks with the right partner. DOWC domestic structures typically require 3–6 months for regulatory approval plus a 12–24 month seeding period before full tax benefits activate.

What is the difference between an Admin Obligor and a CFC reinsurance structure?

An Admin Obligor (or Dealer Held Warranty Company) is structured as an administrative obligor on the contract, giving the dealer direct control over the customer experience and claims. A CFC is an offshore entity that receives ceded premium reserves and benefits from IRC 831(b) tax treatment.

Can small or independent auto dealers start their own reinsurance company?

Smaller and independent dealers can participate through entry-level CFC or Admin Obligor structures with modest formation costs — a large dealership group is not required. Many independent and BHPH dealers qualify at volume levels that often surprise them.

What ongoing costs should dealers expect after setting up a reinsurance company?

Main recurring costs include annual compliance and renewal fees ($3,800–$5,000/year), ceding fees (varies by administrator and product type), premium taxes (~2.25% in common reference states), and custodial/investment management fees (~0.5% of assets). DealerRE bundles these into a single transparent program, handling all filings, renewals, and reporting on the dealer's behalf.