Introduction

Every time a dealership sells a vehicle service contract through a third-party provider, the underwriting profits from unused reserve funds flow to that provider — not to the dealer. The concept of dealer-owned reinsurance offers a way to recapture those profits, and dealer interest has accelerated as F&I becomes an increasingly reliable revenue source. According to Haig Partners' Q3 2025 analysis, F&I gross profit per vehicle retailed reached $2,534, up 5.2% year-over-year, confirming F&I as one of the most stable dealership profit centers.

That growing interest raises an immediate question: what does it actually cost to get started?

The cost varies based on program structure, dealership volume, administration level, and the partner selected. Many dealers run into expensive surprises — underbudgeting for recurring fees like ceding costs and premium taxes, choosing the lowest-cost formation without evaluating compliance risk, or missing hidden admin fees that quietly erode underwriting profits.

This article breaks down realistic cost ranges, key cost components, what drives prices up or down, and the budgeting mistakes dealers most commonly make when evaluating VSC reinsurance programs.

TL;DR

- Startup costs range from $10,000–$13,000 (entry-level) to $18,000–$30,000 (mid-range) and $260,000+ for full-service programs

- Key cost drivers include initial paid-in capital (held in trust, not lost), ceding fees, administration fees, and state premium taxes

- Programs typically pay for themselves within 1–2 years by recapturing underwriting profits previously paid to third-party warranty companies

- Higher-volume operations benefit most from full-service programs — but lower-volume dealers can enter at reduced capital thresholds

How Much Does It Cost to Start a VSC Reinsurance Program?

VSC reinsurance programs cost far less to launch than most dealers expect — especially compared to traditional captive insurance structures, which carry much higher formation fees and minimum capital requirements. Most dealer programs operate under an administrator obligor model, where an A-rated admitted carrier backs the program and limits the dealer's direct financial exposure.

Dealers often misunderstand costs by underbudgeting for recurring fees, choosing the lowest-cost formation without evaluating compliance risk, or being surprised by hidden admin fees that erode underwriting profits.

Tier 1: Entry-Level Program (Lower-Volume or First-Time Dealers)

Typical year-one all-in cost: $10,000–$13,000

What's included:

- Corporate entity formation and registration

- Reinsurance license application and approval

- Articles of incorporation, bylaws, and operating agreements

- Registered agent appointment

- Tax ID (EIN) registration

- IRS election filings

- Modest initial trust capitalization (approximately $5,000 minimum)

Best for: Dealers newer to VSC reinsurance or those with modest monthly VSC volume who want to establish the program structure and test the model before scaling.

Tier 2: Mid-Range Program (Established Dealers with Consistent VSC Sales)

Typical year-one all-in cost: $18,000–$30,000

What's included:

- All Tier 1 formation components

- Scaled initial capital deposit ($10,000–$25,000)

- First-year administration setup (claims adjudication, compliance, financial reporting)

- Custodial trust account setup

- Initial compliance filings

Ideal for: Franchise dealers, retail dealers, or independent dealers with steady monthly VSC volume ready to capture ongoing underwriting profits.

Tier 3: Full-Service Program (High-Volume Dealers or Multi-Location Operations)

Typical year-one all-in cost: $260,000–$1,050,000+

What's included:

- Complete Dealer Owned Warranty Company (DOWC) formation

- Substantial statutory capital deposit ($250,000–$1,000,000)

- Regulatory approval and state licensing (3–6 month timeline)

- Hands-on account management

- Active investment management of excess reserves

- Full claims administration and compliance filings

- Monthly performance reporting and tax preparation

Who should consider this: High-volume dealerships or multi-location groups wanting to fully optimize F&I profitability and offload all compliance and administrative management to a specialized partner.

Quick-Reference: Tier Comparison

| Program Tier | Year-One Cost | Capital Deposit | Best For |

|---|---|---|---|

| Tier 1 — Entry-Level | $10,000–$13,000 | ~$5,000 | First-time or lower-volume dealers |

| Tier 2 — Mid-Range | $18,000–$30,000 | $10,000–$25,000 | Franchise, retail, or independent dealers |

| Tier 3 — Full-Service (DOWC) | $260,000–$1,050,000+ | $250,000–$1,000,000 | High-volume or multi-location groups |

To put payback in perspective: a dealer selling 20 VSC contracts monthly at $800 average reserve per contract, assuming a 50% loss ratio, generates approximately $8,000/month in underwriting profit. Against a $20,000 mid-range startup cost, that's a payback period of roughly 2.5 months.

Key Cost Components of a Dealer VSC Reinsurance Program

The total cost extends well beyond what appears on a formation invoice. Dealers who budget only for setup fees routinely get caught off guard by recurring charges that compound over time. Five distinct cost categories shape what you'll actually spend — one-time setup costs, ongoing compliance fees, and percentage-based charges that scale with your premium volume.

Formation and Legal Fees (One-Time)

Cost range: $4,000–$8,000 (entry to mid-range); $10,000–$20,000 (DOWC)

Formation fees cover:

- Corporate entity setup (articles of incorporation, bylaws, operating agreements)

- EIN registration

- Registered agent fees

- Reinsurance license application fees

The Automotive Assurance Group reports that attorneys and CPA firms handling setup also manage ongoing renewal fees, books, records, and tax preparation at approximately $3,800/year.

Initial Paid-In Capital / Trust Capitalization (One-Time Asset)

Entry-level: $5,000 minimum | Mid-range: $10,000–$25,000 | Full-service: $250,000–$1,000,000+

Initial capital is not a sunk cost. These funds sit in a trust account and can be invested, generating returns on top of underwriting profits. The IRS requires this capitalization to treat the entity as a legitimate insurance company.

For 2026, the IRS raised the IRC Section 831(b) micro-captive premium threshold to $2.9 million, meaning the entity is taxed only on investment income — not underwriting income — as long as premiums stay under $2.9 million. Most single-rooftop dealers fall comfortably under this cap.

Once trust balance sheet cash exceeds 125% of unearned premiums, excess funds may be invested more aggressively beyond conservative government bonds. Trust and custodial fees typically run 0.4%–0.6% annually.

Ceding Fees (Recurring — Percentage of Premiums)

Industry range: 1%–20% of net premium

Ceding fees are charged by the fronting admitted carrier that transfers risk and premium reserves to the dealer's reinsurance company. The wide range reflects what is bundled versus billed separately — CBT News documented that ceding fees can reach 10% and are sometimes itemized apart from broader administration fees.

Before signing any program agreement, confirm in writing whether ceding fees are bundled into administration costs or charged as a separate line item.

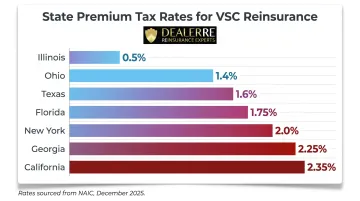

State Premium Taxes (Recurring — State-Specific)

General range: 0.5%–2.35% of direct premiums

Premium taxes are assessed by the state where the admitted carrier files and vary significantly:

| State | Premium Tax Rate |

|---|---|

| Illinois | 0.5% |

| Ohio | 1.4% |

| Texas | 1.6% |

| Florida | 1.75% |

| New York | 2.0% |

| Georgia | 2.25% |

| California | 2.35% |

Source: NAIC Premium Tax Rate by Line, December 2025

This recurring cost is often overlooked in initial budgeting. Some administrators charge an inflated premium tax surcharge of 1%–2% in addition to the actual state rate — a hidden fee dealers should watch for when reviewing program agreements.

Annual Administration and Compliance Fees (Recurring)

General range: $3,800–$5,000/year (basic compliance); higher for full-service

Annual costs cover:

- Compliance filings and annual renewal fees

- Monthly financial statements

- Tax return preparation (Form 1120PC)

- Claims adjudication

- CPA and attorney filings

- Compliance monitoring

A full-service administrator handles all of these tasks under one agreement. Self-administered programs shift that coordination burden to the dealer — and the cost of sourcing each vendor separately often exceeds the bundled fee.

What Factors Affect Your Total Startup Cost?

Monthly VSC Volume and Premium Flow

The more VSCs a dealership sells each month, the larger the premium reserves flowing into the reinsurance company — which means higher ceding fees and premium taxes as dollar amounts, but also proportionally larger underwriting profit capture.

Using illustrative math: a dealer selling 20 VSCs/month at $800 reserve per contract generates $16,000 monthly in gross premiums. Assuming a 50% loss ratio, that's $8,000/month in underwriting profit, or $96,000 annually. Higher volume justifies higher initial capital investment.

Colonnade Advisors found that franchise dealerships attach VSCs to 42% of used vehicle sales versus only 20% at independent dealers — a gap that represents real, uncaptured reinsurance income for independents willing to formalize their programs.

Dealer Type and Program Structure (BHPH vs. Retail vs. Franchise)

BHPH dealers typically use reinsurance to protect their portfolios from mechanical breakdown claims funded by their customer base, while franchise and retail dealers focus on replacing third-party F&I products.

Key BHPH structural differences:

- Premium financing: BHPH dealers finance VSC premiums monthly as customer payments arrive, rather than collecting upfront

- Collateral protection focus: Products like Vendor Single Interest (VSI), Collateral Protection Insurance (CPI), and Debt Cancellation Coverage (DCC) are central

- Payment continuity: AutoSuccess reports that 33% of failed BHPH customer relationships stem from mechanical breakdowns — reinsurance funds repairs that keep vehicles running and customers paying

Program structure directly shapes administration complexity and cost. Bundling GAP, CPI, DCC, and VSCs expands that scope considerably — which brings the administrative requirements into sharper focus.

Level of Administration and Management Support

Self-administered programs carry lower ongoing fees but place the full compliance burden on the dealer. That includes:

- Claims adjudication and dispute resolution

- Regulatory filings and state compliance reporting

- Financial reporting and tax preparation

- Annual renewals and legal form management

Fully managed programs cost more but eliminate that operational complexity. For dealers without insurance industry experience, the compliance exposure of self-administration often outweighs the fee savings. A full-service administrator like DealerRE handles legal forms, filings, tax returns, and renewals — reducing audit risk and keeping dealer attention where it belongs: on the lot.

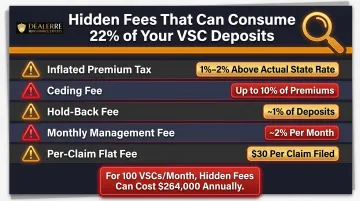

Transparency of the Administrator's Fee Structure

Not all administrators disclose their full fee structure upfront. CBT News documented that undisclosed fees can consume 22% of every VSC dollar deposited into reinsurance:

| Fee Type | Example Rate/Amount |

|---|---|

| Inflated premium tax | 1%–2% above actual state rate |

| Ceding fee | Up to 10% of premiums |

| Hold-back fee | Approximately 1% |

| Monthly management fee | Approximately 2% |

| Per-claim flat fee | $30 per claim |

For a dealer averaging 100 VSC contracts monthly, these hidden fees can cost $264,000 annually. Before signing with any administrator, request a complete fee schedule in writing and verify that every line item is accounted for — not buried in contract language.

Administrators that publish a transparent fee structure upfront — DealerRE among them — make it easier to model true program costs before committing capital.

Minimal Setup vs. Full-Service Administration: What's the Real Difference?

Dealers evaluating VSC reinsurance programs often face a choice between lower-cost, bare-bones formation and a fully managed program — and the differences go well beyond the initial fee.

| Dimension | Minimal Setup | Full-Service Administration |

|---|---|---|

| Compliance Management | Dealer sources and manages independently | Partner manages all filings, renewals, and regulatory requirements |

| Claims Administration | Dealer arranges separately with third-party adjudicator | Full adjudication from first call to claim resolution |

| Tax Preparation & Reporting | Dealer hires separate CPA and tax preparer | Handled by insurance tax experts; includes Form 1120PC and monthly statements |

| Long-Term Risk | Higher audit and compliance exposure | Reduced risk through expert oversight and regulatory adherence |

| Ongoing Cost | Lower fees but higher hidden costs from vendor coordination | Higher upfront fees but predictable, bundled cost structure |

Dealers focused on selling and servicing cars rarely have the bandwidth to manage compliance filings, tax reporting, and claims coordination across separate vendors. The full-service model consolidates all of that under one roof — which is where the real cost comparison becomes clear.

What Most Dealers Miss When Evaluating VSC Reinsurance Costs

Three cost evaluation mistakes show up repeatedly — and each one can quietly erode the program's profitability before it gets off the ground.

Focusing Only on the Formation Invoice

Many dealers budget for entity setup and forget that recurring costs — ceding fees, premium taxes, annual admin, custodial fees — are ongoing from year one. The real budget question is total annual cost relative to underwriting profit captured.

Writing Off the Initial Capital Deposit as a Loss

Trust capitalization is not a sunk cost — it's an investable asset. Once reserve balances exceed 125% of unearned premiums, excess funds can move into higher-yield instruments, generating additional ROI. Dealers who overlook this misread the financial structure of the program.

Choosing the Cheapest Administrator Without Checking Fee Transparency

Hidden fees can eliminate a meaningful share of the underwriting profit the program was built to create. Common culprits include:

- Holdback fees not disclosed at enrollment

- Inflated premium surcharges added post-agreement

- Per-claim fees buried in fine print

- Monthly management fees absent from the initial pitch

CBT News reported that undisclosed fees eroded 22% of every deposited dollar — costing one dealer $264,000 annually.

DealerRE provides a full cost breakdown upfront, with no hidden fees added after enrollment.

Frequently Asked Questions

What is a VSC provider?

A VSC (Vehicle Service Contract) provider is the company that administers and backs the service contract sold at the dealership, handling claims processing, coverage terms, and reserves. Third-party providers retain underwriting profits, while dealer-owned reinsurance structures allow dealers to recapture those profits.

What is a VSC fee?

VSC fees refer to administrative costs built into the vehicle service contract's total price, covering the administrator's services, fronting insurer fees, agent commissions, and reserves. In a dealer-owned reinsurance program, the dealer recaptures the reserve portion rather than remitting it to a third party.

What is dealer VSC?

Dealer VSC refers to vehicle service contracts offered and sold directly through the dealership's F&I department. These can be sold through a third-party warranty provider or through a dealer-owned reinsurance program where the dealer retains underwriting profits.

How much does a vehicle service contract cost?

From the dealer's perspective, VSC pricing includes a dealer markup retained immediately at sale and a dealer cost that incorporates the reserve. Through a reinsurance program, that reserve is held in a dealer-controlled trust instead of flowing to a third-party warranty company.

Is VSC insurance worth it?

For dealers selling VSCs through third-party providers, profitability is limited to markup. For dealers running their own reinsurance program, the wealth-building potential through underwriting profits and investment income on trust reserves makes it far more valuable over the long term.

What is reinsurance pricing?

Reinsurance pricing refers to the cost structure of a dealer-owned reinsurance program, which includes ceding fees, premium taxes, administration fees, and initial capitalization. These costs are offset by the underwriting profits and investment income dealers earn by retaining reserve funds instead of remitting them to a third-party warranty company.

Ready to explore how a VSC reinsurance program can transform your F&I profitability? Contact DealerRE at (804) 824-9533 for a confidential dealership analysis and transparent cost breakdown tailored to your volume and goals.