Startup costs for a DOWC vary widely depending on structure type, monthly contract volume, capital reserve requirements, and state-specific regulatory demands. This article breaks down what those costs actually look like across different dealer profiles.

Key Takeaways

- Startup costs run from ~$10,000–$20,000 for entry-level admin obligor structures to $100,000+ for full-scale DOWC formation

- Capital reserve requirements are typically the largest single cost component

- Lower-volume dealers often start with admin obligor structures, which have fewer regulatory hurdles and lower upfront costs

- Full-service administration partners reduce ongoing costs tied to compliance, filings, and claims management

How Much Does a Dealer-Owned Warranty Company Cost to Start?

There is no single fixed price for launching a dealer-owned warranty company. The final cost depends on the dealer's chosen structure, monthly contract volume, home state regulations, and whether they partner with a full-service administrator or attempt self-management.

Two common pitfalls significantly underestimate total startup costs:

- Focusing only on formation fees while ignoring reserve requirements that typically dwarf entity setup costs

- Failing to account for ongoing compliance and administration expenses that accumulate monthly and annually

Entry-Level: Admin Obligor Reinsurance Structure

For dealers seeking the lowest barrier to entry, an admin obligor or reinsurance-based structure offers a practical starting point. One provider cites formation costs of approximately $3,500 with annual maintenance around $2,500 for a producer-owned reinsurance company (PORC), an entry-level structure.

This approach typically includes:

- Entity formation and basic legal documentation

- Minimal reserve seeding (reserves build from premiums over time)

- Third-party administration partnership

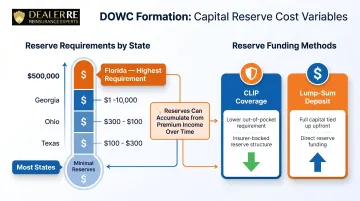

- CLIP (Contractual Liability Insurance Policy) backing

Best suited for: Independent dealers, BHPH operations, or lower-volume franchise dealers who want to capture underwriting profit without the full complexity of a domestic DOWC. Reinsurance becomes practical for many dealers at about 20–25 service contracts per month, making this structure accessible to a broad range of operations.

DealerRE specializes in admin obligor reinsurance structures, providing dealers with an accessible entry point that retains underwriting profits while avoiding the heavier infrastructure of a full DOWC.

Mid-Range: Growing Dealer or Single-Rooftop DOWC

Dealers moving beyond the PORC tier — generally those selling 40 or more VSCs per month — face a more involved startup profile. All-in cost figures for single-rooftop DOWCs vary widely by state, but breaking down the component costs shows what drives that number.

At this level, typical inclusions are:

- C-corp formation and state filings for service contract provider registration

- Initial capitalization: Industry sources cite average initial DOWC capitalization around $50,000, though requirements vary significantly by state

- Contractual Liability Insurance Policy (CLIP) or reinsurance backing to satisfy state financial security requirements

- Third-party administrator partnership for claims, compliance, and reporting

For reference, one analysis shows per-contract allocations including $250 TPA fee, $50 CLIP expense, and $350 to reserves on a $1,200 VSC, illustrating the economics once operational.

Full-Scale DOWC: Multi-Rooftop or High-Volume Groups

Large dealer groups operating across multiple rooftops face the most substantial startup investment. Capital reserve seeding at this scale frequently reaches six figures — Florida, for example, requires $500,000 capitalization for DOWCs operating in that state, one of the more stringent thresholds in the country.

At this level, infrastructure costs rise considerably and typically include:

- Full legal and compliance counsel for multi-state filings

- Substantial reserve accounts to cover projected claims liability

- Dedicated accounting and financial reporting systems

- Ongoing state registration renewals and regulatory filings

- Comprehensive third-party administration covering claims adjudication, tax returns, and performance reporting

The trade-off is straightforward: heavier upfront investment, but 100% profit retention, investment income on reserve funds, and meaningful enterprise value added when the dealership eventually sells.

Key Factors That Affect DOWC Startup Costs

The final cost of forming a dealer-owned warranty company is shaped by structural, regulatory, and operational decisions made before the entity is ever filed.

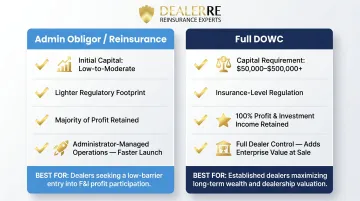

Structure Type: Admin Obligor vs. Full DOWC

The choice between an admin obligor reinsurance program and a full domestic DOWC represents the single most significant cost variable.

Admin obligor reinsurance programs require lower capital reserves, carry a lighter regulatory footprint, and allow dealers to begin capturing underwriting profits quickly. These structures are backed by A-rated insurers through CLIP coverage, reducing risk while maintaining profitability.

DealerRE specializes in this approach — giving dealers an accessible entry point without the overhead of a full DOWC infrastructure.

Full DOWCs, by contrast, require higher reserve seeding, are treated as insurance companies for tax purposes (filing Form 1120-PC), and offer greater control over all aspects of the program. They retain 100% of underwriting profits and investment income, and can add enterprise value when a dealership is sold.

Admin obligor structures suit dealers prioritizing lower upfront cost and faster launch. Full DOWCs fit those willing to invest more capital in exchange for complete ownership and maximum profit retention.

Monthly Contract Volume

VSC volume per month directly affects reserve capital requirements and determines when a program reaches financial break-even. Volume benchmarks for reinsurance viability cluster around 20–25 service contracts per month, with another framework citing approximately 25–30 VSCs monthly or 300–350 annually for PORC structures.

Higher volume dealers face larger reserve obligations since each contract written contributes a portion of its premium to the reserve fund. Example allocations show $350 per contract flowing to reserves in some structures — meaning a dealer writing 100 contracts monthly would need $35,000 in monthly reserve contributions.

Capital Reserve Requirements

This typically represents the largest single startup cost. The DOWC must hold sufficient reserves to cover projected claims liabilities, and requirements vary by state and by the type of backing used.

Key considerations:

- Ranges from minimal in most states to $500,000 in Florida, so state of domicile matters

- CLIP coverage can satisfy statutory reserve requirements at lower capital cost, reducing how much dealers must tie up out of pocket

- Many programs allow reserves to accumulate from premium income rather than requiring large lump-sum deposits upfront, which protects dealer cash flow during the early months

State Filing and Regulatory Requirements

Formation costs vary substantially by state. Over 30 states have adopted major elements of NAIC Model #685, the model framework for service contract regulation, but implementation details differ.

More complex regulatory environments:

- Florida — regulates service contract obligors in a quasi-insurance manner with higher capitalization thresholds and stricter ongoing oversight

- Washington — requires provider registration and annual reporting by March 1 under RCW 48.110

- Minnesota — all service contract providers must register with the commissioner before writing contracts

Eight states — DE, DC, IN, MI, NJ, PA, SD, and TN — regulate service contracts through non-insurance authorities (typically the state attorney general), which creates entirely different compliance pathways than insurance department registration.

Third-Party Administrator (TPA) Fees

Most dealers work with a third-party administrator for claims adjudication, compliance oversight, tax filings, and performance reporting. TPA fees are a recurring cost, typically structured per contract or as a flat monthly fee.

Industry examples show TPA fees around $250 per contract on a $1,200 VSC. For a dealer writing 50 VSCs monthly, that's $12,500 in monthly TPA fees — or $150,000 annually.

Full-service administrators handle all compliance, filings, claims, and financial reporting under a single arrangement, eliminating the need for dealers to manage these functions internally.

Full Cost Breakdown: One-Time and Ongoing Expenses

Startup cost goes beyond the initial formation check. Here's what to budget for across both one-time and recurring expenses:

| Cost Item | Type | Estimated Cost |

|---|---|---|

| C-corp formation and legal fees | One-Time | ~$3,500 (entry-level PORC); higher for multi-state DOWC |

| Capital reserve seeding | One-Time / Initial | ~$50,000 average; varies by volume and structure |

| CLIP / reinsurance backing | Recurring | ~$50 per $1,200 VSC contract; total depends on volume |

| TPA and compliance management | Recurring | ~$250 per contract; ~$2,500/year for entry-level programs |

Capital reserve seeding is typically the largest upfront commitment, but many programs allow reserves to accumulate from incoming premiums — reducing the initial lump-sum requirement considerably. TPA fees cover claims processing, state filings, Form 1120-PC tax preparation, and performance reporting. Full-service administrators bundle all of this under a single arrangement, which simplifies compliance management for most dealers.

Low-Cost Setup vs. Full-Scale DOWC: What's the Difference?

The choice between a lower-cost admin obligor entry point and a full DOWC comes down to more than budget. It reflects the dealer's monthly volume, growth goals, and tolerance for regulatory and operational complexity.

| Dimension | Admin Obligor / Reinsurance | Full DOWC |

|-----------|----------------------------|-----------|

| Initial Capital Required | Low to moderate; reserves build from premiums | Higher; often $50,000–$500,000+ depending on state and volume |

| Regulatory Complexity | Lighter; backed by A-rated insurers via CLIP | Heavier; treated as insurance company, files 1120-PC, subject to state insurance oversight |

| Profit Retention | Majority of underwriting profit retained | 100% of underwriting profit and investment income retained |

| Level of Control | Administrator manages operations; dealer retains profit | Dealer has full control over claims, pricing, coverage, and operations |

Long-term value:

A full DOWC retains 100% of underwriting profits and investment income and can add measurable enterprise value when the dealership sells. For most dealers starting out, an admin obligor reinsurance structure captures the majority of that profit with significantly lower upfront cost and regulatory burden. That combination makes it the more accessible entry point before scaling to a full DOWC.

How to Budget for a DOWC (and What Most Dealers Get Wrong)

The most important budgeting mistake dealers make is evaluating DOWC startup costs in isolation rather than comparing them against what they're currently paying third-party providers in lost underwriting profit.

The opportunity cost framework matters more than the absolute dollar cost. VSC loss ratios typically run 25%–45%, with blended portfolios around 30%–40% — meaning 55%–75% of premium dollars represent gross profit. In traditional third-party arrangements, most of that profit flows to the provider. Distributor markups on VSCs can reach 100%, which puts the scale of what dealers routinely leave on the table in sharp relief.

Key Variables to Calculate Before Selecting a Structure

- Monthly VSC volume — determines reserve scaling and break-even timeline

- Average contract premium — affects total capital flowing through the program

- Current loss ratio — indicates how much of each premium dollar goes to claims vs. profit

- Existing TPA or F&I provider fees — quantifies what you're currently paying away

- Home state regulatory requirements — impacts formation cost and ongoing compliance burden

DealerRE works through each of these variables with dealers directly, mapping them to the right program structure and a realistic cost projection before any commitment is made.

Three Things Dealers Miss When Calculating Total Cost

- Compliance costs accumulate annually — state renewals, tax returns, audits, and regulatory updates add real dollars to the total, especially without a full-service administrator handling them

- Internal time investment is often underestimated — without full-service administration, dealers must commit internal staff to claims adjudication, compliance tracking, and financial reporting

- Profitability has a ramp period — some programs take 12–24 months before reserves build to the point where the financial benefit is clearly visible; factor this timeline into your projections from day one

Frequently Asked Questions

Who owns the dealer-owned warranty company?

The dealer or dealer group fully owns the DOWC as a separate C-corporation. A third-party administrator typically handles daily operations, claims, compliance, and filings, while ownership and all profits remain entirely with the dealer.

What does the DOWC warranty cover?

DOWCs primarily cover non-insurance F&I products such as vehicle service contracts (VSCs), which protect against mechanical breakdown. Depending on program structure, they may also include GAP, tire and wheel, debt cancellation, collateral protection, and appearance protection.

Do dealers make money on warranty work?

Through a DOWC or admin obligor reinsurance structure, dealers retain the underwriting profit — premiums minus claims and admin costs — that would otherwise go to a third-party provider. This makes it one of the most significant wealth-building levers available through the F&I office.

Is DOWC a good investment?

For dealers with sufficient volume and access to strong administrative infrastructure, a DOWC or reinsurance program can generate solid long-term returns through profit retention, tax advantages under IRS Code 831(b), and investment income. The right structure depends heavily on volume, goals, and partnership quality.

What ongoing costs should dealers budget for after formation?

Beyond initial setup, dealers should plan for annual administration fees, claims reserves, compliance filings, and state renewal costs. These ongoing expenses are typically modest relative to the underwriting profit retained, and most well-structured programs cover operational costs within the first year of full production.

How long does it take to set up a dealer-owned warranty company?

Formation timelines vary by structure and state. An admin obligor reinsurance program can often be operational within 1 to 6 months, with dealers sometimes warehousing premiums while formation is finalized. A full DOWC involving C-corp filing, state approvals, and reserve establishment takes longer based on multi-state complexity and regulatory review.

Startup costs vary by structure, volume, state, and administration model — there is no single price. What stays consistent is the financial case: every premium dollar currently flowing to a third-party provider is a dollar a dealer-owned program would retain. With the right structure and partner, the formation costs are typically recovered within the first year of underwriting profit.