That arrangement made sense when dealers had no alternative. It no longer does.

More dealers are choosing to own a piece of that equation — or all of it — through dealer-owned reinsurance companies. F&I gross profit per vehicle retailed averaged $1,995 in Q4 2025, up 8.7% year-over-year, which means the profit pool available for recapture keeps growing. This article covers how dealer reinsurance programs are structured, what funding decisions matter most, and what state-level and regulatory factors dealers must understand before launching one.

TL;DR

- Dealer-owned reinsurance lets you capture underwriting profit and investment income instead of handing both to a third-party administrator

- The admin obligor structure, backed by an A-rated fronting insurer, gives dealers direct control over reserves, claims, and invested premiums

- Capitalization minimums vary significantly by domicile, from $100,000 offshore to $500,000 in states like Florida

- IRS micro-captive regulations published in January 2025 affect program design; consult qualified tax counsel before structuring any reinsurance entity

- BHPH dealers face distinct product classification rules requiring different structural approaches than traditional retail F&I programs

What Is a Dealer-Owned Reinsurance Program?

A dealer-owned reinsurance company is a separate insurance entity the dealer controls. When customers buy F&I products at the dealership, a portion of each premium flows into this entity. Claims are paid from its reserves. Whatever remains after claims and fees is the dealer's underwriting profit — not the administrator's.

The Admin Obligor Structure

The admin obligor (AO) structure is the most common framework used by programs like DealerRE. The mechanics are straightforward:

- A licensed, A-rated fronting carrier issues the insurance policy and maintains the regulatory standing required to back the product

- The fronting carrier cedes the risk — and associated premium — to the dealer's reinsurance company

- The dealer participates in underwriting profits while the customer's coverage obligation remains protected by the financially stable carrier

This structure means dealers get the profit upside of self-insurance without the regulatory complexity of becoming a licensed insurer themselves.

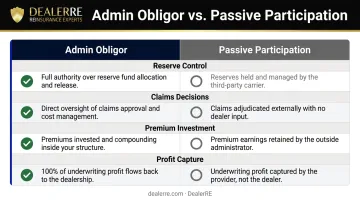

Admin Obligor vs. Passive Participation

Understanding the distinction between these two structures directly affects how much profit a dealer retains — and who controls the money in the meantime.

| Feature | Admin Obligor | Passive Participation |

|---|---|---|

| Dealer controls reserves | Yes | No |

| Claims decisions | Dealer's entity | Third-party administrator |

| Investment of premiums | Dealer directed | Administrator retains |

| Ultimate profit capture | Full underwriting profit | Shared per agreement |

In a participation program, the dealer receives a share of profits — but the administrator retains control of the money until it pays out. The admin obligor structure shifts that control entirely to the dealer — which is why it consistently produces stronger long-term returns for dealerships with consistent F&I volume.

Key Design Decisions for Your Dealer Reinsurance Program

Program design is where long-term profitability is won or lost. Four decisions carry the most weight.

Product Selection

The products you include determine your premium volume, risk exposure, and reserve-building pace. Common inclusions:

- Vehicle service contracts (VSCs) — highest volume driver; DealerRE identifies VSCs as one of the most profitable products to reinsure

- GAP — meaningful premium per deal, but loss ratios have returned to 2007–2008 peak levels as loan terms extend to 84 months and LTV ratios climb above 110%

- Credit life and disability — historically low loss ratios (NAIC data shows national averages around 41–42%), making these strong reserve builders

- Ancillary products — tire and wheel, door ding, windshield, theft protection; lower per-deal premiums but predictable, low-severity claims

Higher-volume, predictable-loss products build reserve strength faster. VSCs with back-loaded loss emergence patterns (only 2–5% of losses emerge in year one for new-car contracts) require rigorous actuarial reserve planning.

That same back-loading also generates substantial investable capital early in the program — capital that compounds before claims pressure materializes.

Attachment Points, Coinsurance, and Caps

Three parameters define how risk is shared between your reinsurance company and the fronting insurer:

- Attachment point — the claims threshold at which your reinsurance company begins paying. Set it too high and you underutilize the program; set it too low and small claims drain reserves before they compound.

- Coinsurance rate — the percentage of eligible claims your entity covers. Model this against your historical loss ratios before locking in. The IRS's 2025 micro-captive regulations use a 65% loss ratio over a 10-year period as one trigger for "listed transaction" classification, so coinsurance design must be actuarially defensible from the start.

- Reinsurance cap — the upper ceiling above which the fronting insurer resumes responsibility. This protects your company from catastrophic exposure while defining the band where you retain underwriting risk and profit.

These three parameters interact — a low attachment point combined with a high coinsurance rate can accelerate reserve depletion if loss ratios spike. Model them together, not in isolation.

Reserve Adequacy

Underfunded reserves create claims shortfalls that can trigger regulatory action and erode the program's balance sheet. Under the NAIC Service Contracts Model Act (Model #685), providers must maintain funded reserves of at least 40% of gross consideration received, plus a financial security deposit of at least $25,000 (or 5% of gross consideration, whichever is greater).

Properly funded reserves do more than satisfy compliance. DealerRE's trust structure requires reserves be invested conservatively in government bonds until the balance sheet exceeds 125% of unearned premiums — at that point, dealers can direct more aggressive investment strategies and put that capital to work.

Funding Your Dealer Reinsurance Program

How Premium Flows Work

When a customer buys an F&I product, the premium travels a specific path:

- Dealership collects the full product price

- Administrator deducts fees and sends the reserve portion to the fronting carrier

- Fronting carrier cedes the risk and premium into your reinsurance entity

- Claims are paid from your entity's reserves

- Excess after claims and fees remains as profit — and earns investment income while waiting

For BHPH dealers, DealerRE structures premium payments over the contract term rather than requiring a lump sum upfront, which protects dealer cash flow and lending pool stability.

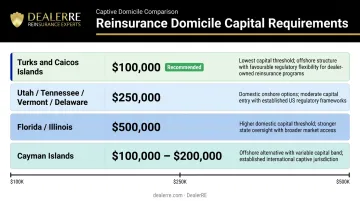

Startup Capitalization

Domicile choice drives capitalization requirements more than any other single factor:

| Jurisdiction | Minimum Capital | Notes |

|---|---|---|

| Utah / Tennessee / Vermont / Delaware | $250,000 | Common domestic choices |

| Florida / Illinois | $500,000 | Higher domestic tier |

| Turks and Caicos | $100,000 | DealerRE's primary recommendation; assets remain in the U.S. |

| Cayman Islands (Class B) | $100,000–$200,000 | Varies by license class |

DealerRE recommends the Turks and Caicos Islands for most dealer programs. The government there established specific regulations enabling reinsurance company formation with minimal capital investment, and all assets remain in U.S.-based trust accounts.

One common misconception worth clearing up: you don't need enormous sales volume or capital to start. The program scales from the volume you already have.

Investment of Reserves and Surplus Distribution

While premiums accumulate in reserve, they earn investment income — a secondary revenue stream on top of underwriting profit. Funds must be placed in investments acceptable to state regulators until reserves exceed the 125% threshold, at which point the dealer directs more aggressive allocation.

Distributable surplus — reserve funds exceeding projected claims obligations — can be returned to the dealer as income. DealerRE clients have used those distributions to:

- Acquire real estate

- Fund children's education

- Reinvest in dealership operations

- Purchase other assets

Distribution timing and method carry significant tax implications. An insurance tax expert prepares all required returns, and DealerRE reviews financial direction with owners periodically to keep planning ahead of those obligations.

State-Level Regulatory and Structural Considerations

Product Classification Drives Structure

The same dealer may need different reinsurance structures for different products — because product classification varies by state:

- Vehicle service contracts — not classified as insurance in most states; backed by NAIC Model #685 financial security methods (funded reserves, reimbursement policy, or $100M net worth). Approximately 30 states have broadly adopted Model #685 elements.

- Mechanical breakdown insurance (MBI) — regulated as insurance in California and some other states; must be backed by a licensed insurer

- Collateral protection insurance (CPI) — always classified as insurance; requires licensed insurer backing regardless of state

- Credit life and disability — always insurance; regulated by state insurance departments

Florida uniquely treats service contracts as "quasi-insurance," which creates a separate compliance track for dealers operating there.

Domicile Choice and Compliance Management

Offshore domiciles like the Turks and Caicos (home to over 2,700 restricted license reinsurers) offer lower capitalization minimums and established regulatory frameworks for dealer reinsurance. Domestic options in states like Utah, Tennessee, and Vermont offer regulatory familiarity and avoid offshore disclosure requirements — but come with higher capital minimums and ongoing state insurance department oversight.

The trade-offs between domicile options generally break down as follows:

| Factor | Offshore (e.g., Turks & Caicos) | Domestic (e.g., Utah, Vermont) |

|---|---|---|

| Capital minimums | Lower | Higher |

| Disclosure requirements | Offshore reporting applies | None |

| Regulatory familiarity | Less familiar to US dealers | Familiar framework |

| Oversight | Jurisdiction-specific | State insurance department |

DealerRE manages all legal forms, filings, tax returns, and renewals through partnerships with specialized administrators, CPAs, and legal counsel. Getting domicile selection and initial filings right matters — errors made at setup tend to compound over time.

BHPH-Specific Considerations

BHPH dealers typically work across more product classification categories than traditional franchise or retail dealers — which compounds state-by-state compliance demands. The most common BHPH reinsurance products span both insurance-classified and non-insurance-classified categories:

- Limited warranties and mechanical breakdown coverage — often non-insurance classified; governed by NAIC Model #685 or state-specific equivalents

- CPI (collateral protection insurance) — always insurance; state rules on point-of-sale vs. force-placement vary significantly

- GAP and debt cancellation — classification varies; some states treat debt cancellation as a banking product, others as insurance

CPI rules alone can differ enough between states to require separate program structures. A BHPH dealer operating in multiple states needs a program design that addresses each jurisdiction's requirements from the start.

Tax Planning and Financial Benefits of Proper Program Design

How the Tax Structure Works

Premiums paid into the reinsurance company may be treated as deductible business expenses at the dealership level, while income inside the reinsurance entity can be subject to more favorable tax treatment depending on structure and domicile.

Under IRC Section 831(b), qualifying small insurance companies can elect to be taxed only on investment income rather than premium income. The annual net written premium cap for this election is $2.8 million for recent tax years.

The IRS micro-captive final regulations published January 14, 2025 designated certain arrangements as listed transactions or transactions of interest. The key trigger: a loss ratio below 65% over a 10-year computation period. However, a "Consumer Coverage Exception for Seller's Captives" carve-out exists for certain dealer reinsurance structures — and according to ForvisMazars, many dealer reinsurance companies will not be subject to these regulations given the intentional definitions and this exception.

Dealers must consult qualified tax counsel with captive insurance expertise before making any tax elections, structuring premium flows, or claiming deductions related to a reinsurance entity.

Wealth-Building Beyond Underwriting Profit

Annual performance reports from a well-managed program provide monthly financial statements covering all reinsurance activity — giving dealers visibility into reserve positions, claims trends, and distributable income before year-end arrives. That visibility makes tax planning strategic rather than reactive.

Surplus that accumulates through consistent premium contributions and disciplined reserve management becomes distributable income — capital dealers can direct toward goals well beyond the dealership floor. Common reinvestment strategies include:

- Acquiring real estate using accumulated reinsurance surplus

- Funding dealership expansion without tapping traditional credit lines

- Covering education costs for family or key employees

- Purchasing watercraft, investment property, or other personal assets

These outcomes depend on getting program design and funding right from the start.

How DealerRE Helps Dealers Build Programs That Last

DealerRE has helped more than 400 dealers build and manage their own reinsurance companies since Tim Byrd founded the company in Southeast Virginia in 1994. The full-service model covers:

- Initial business analysis — evaluating dealership volume, product mix, and profitability targets before recommending any program structure

- Company setup — managing all formation documents, filings, and legal requirements across jurisdictions

- Staff training — online and in-person F&I training through DealerRE's academy, plus F&I menus and development support

- Ongoing administration — claims adjudication through AVP (Assured Vehicle Protection), monthly financial statements, compliance management, and tax return preparation

- Annual performance reviews — periodic meetings with ownership to review reserve positions, financial direction, and distribution strategy

Every DealerRE program uses the admin obligor structure backed by A-rated carriers. That means the dealer's reinsurance company captures underwriting profit and investment income, without exposing personal or business assets to uncapped claims risk. There are no hidden fees. For dealers evaluating program design and funding structure, that combination — retained profit, capped exposure, and full administrative support — is what determines whether a reinsurance program holds up over time.

Frequently Asked Questions

What is the difference between an admin obligor reinsurance program and a standard dealer participation program?

In an admin obligor program, the dealer's own reinsurance company holds reserves, controls claims, and directs investment of premiums — all backed by an A-rated fronting insurer. In a participation program, the third-party administrator retains ultimate control over reserves and distributes profit shares to the dealer on its own timeline and terms.

How much capital does a dealer need to start a reinsurance company?

Capitalization minimums vary by domicile — from $100,000 in the Turks and Caicos Islands to $500,000 in states like Florida. Actuarial feasibility studies may push actual requirements above statutory minimums. Confirm current figures with a qualified reinsurance administrator before budgeting.

Which F&I products work best in a dealer-owned reinsurance program?

Vehicle service contracts, GAP, and credit life/disability are the most common inclusions. VSCs drive the most premium volume; credit life and disability historically show lower loss ratios and build reserve strength faster. Product selection should reflect your dealership's sales volume and claims history.

How are profits distributed from a dealer reinsurance company?

Distributable surplus — reserve funds exceeding projected claims obligations — can be returned to the dealer as income once the trust balance satisfies reserve requirements. The timing and structure of distributions carry real tax planning implications, so distribution decisions should be coordinated with qualified tax counsel.

Does a dealer reinsurance program work differently for BHPH dealerships?

Yes. BHPH programs focus on mechanical breakdown coverage, collateral protection insurance, and debt cancellation products funded through customer payment streams. Because CPI is insurance-classified in every state, program design must satisfy insurance regulatory requirements — not just service contract statutes — a key difference from traditional retail F&I structures.

How long does it take to set up a dealer-owned reinsurance company?

Most programs reach active status within 60–90 days, depending on structure, domicile, and dealership complexity. Working with a full-service administrator compresses the process compared to navigating formation independently. Contact DealerRE at (804) 824-9533 to discuss your specific timeline.