This guide explains what an 831(b) captive is, how the tax election works, what benefits it offers, and why dealer-owned reinsurance programs are particularly well-positioned to take advantage of it.

At a Glance

- 831(b) allows small insurance companies to pay federal income tax only on investment income — not underwriting income — if annual written premiums stay at or below $2.85 million (2025 threshold)

- The insured business deducts premiums as an ordinary business expense while the captive accumulates underwriting profits in a tax-advantaged structure

- Qualification requires genuine risk transfer, actuarially supported premiums, and operation as a legitimate insurance company

- Dealer-owned reinsurance programs can often be structured to qualify under 831(b), layering tax-free underwriting income on top of existing profit retention benefits

What Is an 831(b) Captive Insurance Company?

A captive insurance company is an insurance company owned by one or more business owners, formed specifically to insure that business's risks rather than sell coverage to the general public. It is a licensed, regulated insurance entity — not just a policy or product.

A micro-captive is a captive that qualifies for taxation under Section 831(b) of the Internal Revenue Code, meaning its gross written premium income falls at or below the annual threshold. For 2025, that threshold is $2.85 million, per IRS Rev. Proc. 2024-40.

Where 831(b) Came From

Section 831(b) was enacted as part of the Tax Reform Act of 1986. At the time, a U.S. liability insurance crisis had made coverage scarce and unaffordably expensive for small businesses. Congress created this provision to encourage legitimate captive self-insurance as an alternative.

The original premium cap was set at $1.2 million and remained unchanged until the Protecting Americans from Tax Hikes (PATH) Act of 2015 updated it significantly:

- Raised the cap to $2.2 million and indexed it for inflation

- Added two new diversification requirements under IRC 831(b)(2)(B) — the "20% premium test" and the "ownership test" — to prevent captives from functioning primarily as estate planning vehicles

The Core Distinction

Understanding the legislative history makes the core appeal clear: captives exist to redirect profit flow.

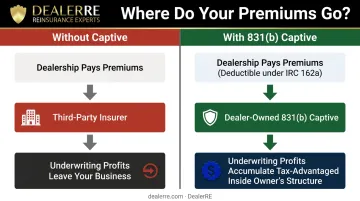

With a commercial insurer, underwriting profits belong to the insurer's shareholders. With a captive, those profits stay inside the business owner's ecosystem. For auto dealers, that means the income generated by vehicle service contracts, GAP, and ancillary F&I products can build value inside a structure you own — rather than funding someone else's balance sheet.

How the 831(b) Tax Election Works

The Core Mechanic

Under IRC 831(b)(1), a qualifying insurance company pays federal income tax only on its taxable investment income — interest, dividends, and capital gains from invested reserves. Underwriting income (premiums earned minus claims paid) is not subject to federal income tax in the same year.

This creates a meaningful accumulation advantage for profitable captives with favorable loss experience.

The Premium Threshold

| Tax Year | Premium Limit | Change |

|---|---|---|

| 2024 | $2,800,000 | — |

| 2025 | $2,850,000 | +$50K |

| 2026 | $2,900,000 | +$50K |

The threshold applies to the greater of net written premiums or direct written premiums — it is not calculated on a net-only basis after cessions. A captive writing $5 million gross that cedes $3 million to a reinsurer still does not qualify.

Aggregation Rules

IRC 831(b)(2)(C) treats all members of the same controlled group as one enterprise for premium threshold purposes. The controlled group threshold uses a modified >50% ownership standard. This means dealer groups with multiple entities cannot split premiums across related captives to stay under the cap.

Eligibility is also evaluated annually — a captive that qualifies one year may lose eligibility the next if premium volume grows past the threshold.

What Happens to Underwriting Profits

Accumulated underwriting profits have two paths:

- Stay in the captive as surplus, strengthening its balance sheet and reserve position

- Distributed to owners as shareholder dividends, typically taxed at qualified dividend rates

On the other side of the transaction, the operating business paying premiums into the captive deducts those premiums as ordinary and necessary business expenses under IRC 162(a) — provided the arrangement constitutes genuine insurance.

That pairing is the core financial case: a dealership or dealer group deducts premium payments at the operating level while the captive accumulates underwriting profits in a tax-advantaged structure. The dealer retains wealth that would otherwise flow to a third-party provider.

Key Tax Benefits of 831(b) Captives

Underwriting Income Accumulation

In years with low or no claims, underwriting profits accumulate inside the captive without triggering federal income tax. That surplus belongs to the business owner — not an outside insurer's shareholders. Over time, a well-run captive with favorable loss history can build a substantial reserve fund.

Premium Deductions at the Operating Level

Premiums paid by the operating business are deductible as ordinary business expenses. This reduces taxable income at the business level while simultaneously building assets inside the captive.

Important: The arrangement must meet IRS standards for genuine insurance to preserve deductibility. If it fails that test, payments may be recharacterized as loans or capital contributions rather than deductible expenses.

Flexible Deployment of Accumulated Reserves

Once reserves build inside the captive, the business owner has real options:

- Reinvest into the dealership or other business operations

- Dividend back to the owner (taxed at qualified dividend rates)

- Purchase real estate or other investment assets

- Fund education expenses for family members

- Build a long-term reserve pool for future claims

Commercial insurers hold and deploy reserves on their own terms. Dealers operating a captive under an 831(b) structure retain that control — directing accumulated income toward priorities that serve the business and the owner's broader financial goals.

Estate Planning Considerations

Captive ownership can be structured through trusts — asset protection trusts, dynasty trusts, or state income tax protection trusts — to help minimize estate taxes and facilitate wealth transfer. This is a secondary benefit — pursue it with qualified legal counsel alongside the primary insurance and tax objectives.

Qualification Requirements and IRS Compliance

The Three Core Criteria

To qualify under 831(b), a captive must meet three requirements:

- Qualify as an insurance company — genuine risk shifting and distribution, adequate capital, and operations consistent with a real insurer

- Be a U.S. taxpayer (or have elected to be treated as one)

- Gross written premium must not exceed $2.85 million for the 2025 tax year

What "Genuine Insurance" Actually Means

Courts and the IRS have consistently identified four elements required for an arrangement to constitute insurance for federal tax purposes:

- Risk shifting — economic risk transfers from the insured to the insurer

- Risk distribution — risk is spread across a sufficiently large pool

- Insurance risk — the risk insured must be an insurance-type risk

- Commonly accepted sense — the arrangement must operate as insurance would in its common meaning

Arrangements that insure implausible or fictitious risks, charge premiums that aren't set through a formal underwriting process, or never actually pay claims are not treated as legitimate insurance. Premium deductibility disappears and penalties may apply.

PATH Act Diversification Tests

To satisfy IRC 831(b)(2)(B), a captive must pass one of two alternative tests:

- Test 1 — Risk Distribution: No single policyholder may contribute more than 20% of the captive's net written premiums. The IRS counts related policyholders in the same controlled group together.

- Test 2 — Ownership: The ownership percentage held by "specified holders" (spouses or lineal descendants of persons with interests in insured assets) must not exceed their ownership of the insured assets by more than 2 percentage points.

Passing either test is necessary — but passing them doesn't fully end the compliance analysis. How the captive is structured and operated matters just as much to the IRS.

IRS Enforcement and the Dirty Dozen List

The IRS has placed micro-captive arrangements on its annual "Dirty Dozen" list of potential tax abuse schemes every year since 2015. The IRS has stated it supports legitimate captive arrangements. The scrutiny targets promoters who market captives primarily as tax shelters rather than genuine risk management tools — a distinction that matters directly to dealers evaluating whether their program is structured to withstand scrutiny.

The 2025 final regulations (T.D. 10029, effective January 14, 2025) established a two-tier classification system:

| Classification | Loss Ratio Trigger | Consequence |

|---|---|---|

| Listed Transaction | Below 30% over 10 years | Mandatory IRS disclosure (Form 8886) |

| Transaction of Interest | Below 60% over 10 years | Reporting requirements apply |

A legitimately structured captive — one that insures real risks, sets premiums actuarially, and pays claims consistently — is unlikely to fall into either classification. Dealers whose programs are built around actual risk management, not tax minimization, are operating on the right side of this line.

How 831(b) Tax Benefits Apply to Dealer-Owned Reinsurance Programs

The Connection Between Reinsurance and 831(b)

Auto dealers who establish their own admin obligor reinsurance companies to replace third-party F&I product providers may qualify under 831(b). When structured correctly, reinsurance premiums flowing into the dealer's company accumulate with tax efficiency, rather than underwriting profits going to an outside provider.

The F&I profit opportunity is substantial. According to Haig Partners' Q1 2025 data, the average publicly owned dealership earned $2,505 in F&I gross profit per vehicle retailed in Q1 2025 — approaching historic highs. Across the industry, F&I products represent an estimated $77 billion business. That's a significant portion of income flowing out to third parties instead of staying in the dealer's own company.

How the Admin Obligor Structure Works

DealerRE helps dealers establish administrator obligor reinsurance companies — a specific structure where the dealer's reinsurance company reinsures policies originally underwritten by A-rated fronting carriers. Here's the flow:

- Customers purchase F&I products (VSCs, GAP, CPI, ancillary coverage)

- Premiums are ceded to the dealer's reinsurance company and held in a U.S. custodial trust account

- Claims are paid from those reserves; the fronting carrier backstops any shortfall

- Underwriting profits accumulate in the dealer's company rather than with the third-party administrator

Products DealerRE helps dealers reinsure include vehicle service contracts, GAP, collateral protection insurance, debt cancellation coverage, and ancillary products like tire and wheel, door ding, windshield repair, and theft protection.

The Compounding Advantage

The admin obligor structure solves the profit-retention problem. Adding 831(b) qualification solves the tax problem. When both work together, the advantages compound:

- Underwriting income accumulates without triggering federal income tax

- Premiums paid by the dealership remain deductible

- Retained profits stay in the dealer's own company, not a third-party provider's

Since 1994, DealerRE's full-service model has covered compliance management, IRS filings, tax return preparation (Form 1120PC), license renewals, claims adjudication, and program governance — coordinated alongside experienced CPAs and legal counsel.

Dealers exploring whether their program can be structured for 831(b) advantages should work with specialists who understand both the F&I environment and the regulatory requirements of captive insurance.

Frequently Asked Questions

What is an 831(b) captive?

An 831(b) captive is a small, owner-operated insurance company that has elected to be taxed under Section 831(b) of the Internal Revenue Code. It pays federal income tax only on its investment income — not its underwriting income — as long as gross written premiums stay at or below the annual threshold ($2.85 million for 2025).

What are the benefits of a captive insurer?

The insured business deducts premium payments, underwriting profits accumulate in a tax-efficient structure the owner controls, and reserves can be invested and deployed strategically. Instead of those profits flowing to a commercial insurer's shareholders, they stay within the dealer's own company structure.

What is the current premium threshold to qualify for 831(b)?

For 2025, the gross written premium threshold is $2.85 million, indexed for inflation and adjusted annually. The threshold applies to the greater of net or direct written premiums. All captives owned or controlled by the same taxpayer count together toward that limit.

How does the IRS determine whether a captive is legitimate?

The IRS looks for genuine risk transfer and distribution, actuarially supported premiums, real insurable business risks, proper claims handling, and overall operation consistent with a legitimate insurer. Arrangements that insure implausible risks, charge inflated premiums, or rarely pay claims are flagged as abusive.

Can auto dealers use 831(b) captive structures for their reinsurance programs?

Yes — dealer-owned reinsurance companies may qualify under 831(b) if properly structured to meet IRS requirements. Dealers should work with administrators who understand both captive insurance compliance and automotive F&I — firms like DealerRE, which has structured dealer-owned reinsurance programs since 1994, can help ensure the program is built correctly and serves a genuine business purpose.