Introduction

Service revenue is no longer just a supplement to vehicle sales — it's become critical to dealership profitability. Pre-paid maintenance programs are among the strongest tools dealers have to lock in repeat service visits, boost F&I income, and improve customer retention all at once.

Most published content on prepaid maintenance plans focuses on the consumer side — very little exists to help dealers actually build and launch one. That gap is costing dealers real business.

According to Cox Automotive's 2025 Service Industry Study, only 54% of owners with vehicles two years old or newer return to the selling dealership for service, down from 72% in 2023. That's an 18-percentage-point swing in less than two years.

This guide covers how to structure, price, and launch a pre-paid maintenance program — from deciding what services to include to training your team to present it in the F&I office.

Key Takeaways

- A pre-paid maintenance program is a bundled service product sold at point of purchase, prepaying for scheduled maintenance over a defined period or mileage

- Dealers benefit through increased service traffic, higher F&I per-deal income, and improved customer loyalty

- Setup requires choosing service bundles, pricing tiers, risk structures, and training your F&I team

- State regulations vary by market; legal review before launch is required

- Structured well, pre-paid maintenance generates recurring service revenue on every enrolled vehicle

What Is a Pre-Paid Maintenance Program at a Dealership?

A pre-paid maintenance program is a fixed-cost service contract sold during the vehicle purchase that covers a set list of scheduled maintenance services — such as oil changes, tire rotations, and multi-point inspections — for a specified term or mileage limit.

Maintenance vs. Warranty: Know the Difference

Prepaid maintenance plans cover routine, scheduled services. Extended warranties cover mechanical failures. Some dealers confuse or blend these categories when building their F&I menu, but they are legally and functionally distinct.

Both the CFPB and the NAIC draw a clear line here. The CFPB describes prepaid maintenance plans as add-on products covering regular maintenance needs, while extended warranties cover defects or failures outside the manufacturer's warranty. The NAIC Service Contracts Model Act defines a "maintenance agreement" as "a contract of limited duration that provides for scheduled maintenance only" — a distinct legal category from service contracts covering repair, replacement, or breakdown.

Two Common Dealer Structures

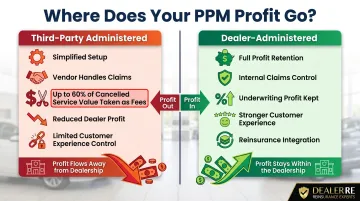

Dealers typically choose between two administrative models:

- Third-party administered: A vendor holds and manages the risk, simplifying setup — but a significant share of profit goes with it.

- Dealer-administered: The dealer controls pricing, claims, and profit, often through a dealer-owned reinsurance structure, retaining substantially more long-term value.

Which model you choose shapes how much of the program's economics you actually keep. Dealers who structure it internally — or through a reinsurance vehicle — consistently retain more than those who outsource.

Why Dealers Should Offer a Pre-Paid Maintenance Program

Pre-paid maintenance programs directly address one of the most persistent problems in retail automotive: customers servicing elsewhere after the sale.

The Service Retention Crisis

According to the 2025 Cox Automotive Service Industry Study, only 54% of people with cars two years old or newer returned to the selling dealership for service, down from 72% in 2023. Dealer share of total service visits fell from 33% to 29% since 2018.

An F&I and Showroom report found that at most dealerships, only 18% to 20% of customers return for service. A prepaid maintenance plan can triple that number to 54%-60%.

The Revenue Case

Each plan sold adds incremental F&I income at point of sale. According to the Haig Report Q2 2025, publicly traded auto retail groups reported an average F&I gross profit per vehicle retailed of $2,515.

Each redeemed service visit creates upsell opportunities — additional repairs, accessories, future purchases — that would otherwise go to a third-party shop. A MediaTrac study found that 95% of plan holders purchase additional services beyond what the prepaid plan covers, generating an average of $102 in additional revenue per repair order.

The Retention Multiplier

Customers who maintain a service relationship with the dealership are more likely to return for their next vehicle purchase. The Cox Automotive Fixed Ops and Ownership Study found that 74% of buyers who returned for service said they were likely to repurchase from that dealer, compared to just 44% who did not return.

A 2014 J.D. Power Customer Service Index Study established an early benchmark: 72% of vehicle owners with a prepaid or complimentary maintenance package repurchased the same vehicle make, versus 62% without — a loyalty gap that has only widened as service competition has intensified.

Low-Risk, High-Value Positioning

Pre-paid maintenance programs differentiate your F&I menu in a way that feels low-risk and high-value to the buyer. It's also one of the easier products to present in the F&I office. Unlike an extended warranty, customers immediately grasp what they're getting:

- Prepaid oil changes and filter services

- Tire rotations on a set schedule

- Multi-point inspections at each visit

- Predictable maintenance costs over the ownership period

That clarity speeds up the presentation and sets the stage for the upsell opportunities that follow — which is exactly what the rest of this guide covers.

What to Know Before You Set Up the Program

Operational Complexity Is Real

Many dealers underestimate the operational work required. Before the first plan is sold, three things need to be in place:

- Pricing that accounts for actual service costs and cancellation reserves

- A service department prepared to honor redemptions without friction

- An F&I team trained on how to present and explain the product

Skipping or rushing any of these steps is the most common reason programs underperform.

Compliance Is Not Optional

Depending on how the program is structured and in which state you operate, pre-paid maintenance contracts may be subject to state insurance or service contract regulations.

The NAIC Service Contracts Model Act explicitly excludes "maintenance agreements" from the definition of "service contract," classifying them as a distinct category. However, state adoption varies significantly.

According to a Troutman Pepper Locke podcast transcript, approximately 20-25 states have adopted a "primary purpose test" via case law, and about 9 states require separate licensure for third-party administrators.

Have qualified legal counsel review your program structure and state-specific requirements before you sell a single contract.

The Profit Gap Between Structures

Dealers who outsource administration to a vendor typically share a large portion of the program's profit. Those who structure it internally — or through a dealer-owned reinsurance vehicle — retain substantially more.

According to F&I and Showroom, third-party administrators may take up to 60% of the value of cancelled services as part of their fee structure. That's revenue leaving your dealership on every cancellation — revenue a dealer-owned structure would keep.

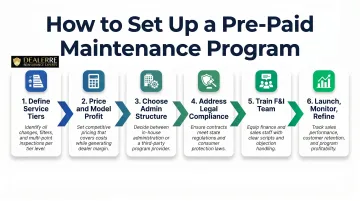

How to Set Up a Pre-Paid Maintenance Program at Your Dealership

This section walks through the full setup process in sequential stages — from defining the product to training staff and tracking performance. Skipping or rushing any stage is the most common reason programs underperform.

Step 1: Define Your Service Offerings and Coverage Tiers

Choose included services carefully. Common examples include:

- Oil and filter changes

- Tire rotations

- Multi-point inspections

- Cabin air filter replacements

- Fluid top-offs

Avoid overloading the plan with services your service department cannot consistently deliver.

Build at least two tiers. For example:

- Basic tier: Oil changes and tire rotations

- Premium tier: Adds multi-point inspections, fluid services, and filter replacements

This gives F&I managers a tiered menu to work with, so they can match the right plan to each customer's budget and vehicle.

Anchor coverage to realistic usage patterns. A BHPH dealer's typical customer may need a shorter-term, lower-mileage plan compared to a new car franchise buyer. Match the plan structure to your customer base's actual driving habits and ownership duration.

Step 2: Price the Program and Model the Profit

Calculate actual delivery cost. Determine the cost to deliver each service included in the plan (parts + labor). This is your cost floor.

For reference, KBB reports that conventional oil changes cost $35-$75, while full synthetic oil changes run $65-$125. A franchised dealer like Toyota of Irving lists conventional oil changes at $59.95 and synthetic at $79.95.

Use retail value to set competitive pricing. Find the retail value of those same services if purchased individually, then use the gap between cost and retail to set a competitive but profitable plan price.

A MediaTrac study found average retail prices for prepaid plans:

- One-year plan: $118

- Two-year plan: $254

- Three-year plan: $369

Factor in redemption rates. Not all customers will redeem every service in the plan. According to Auto Dealer Today, 10% of plan holders never use their plans, and an additional 25% only "sometimes" use their benefits.

Understanding average redemption rates helps you price more accurately and protect margin. F&I and Showroom reported a 55% redemption rate over a two-year term in one case study.

Build in profit margin. Account for both the F&I income at point of sale and any administrative or claims costs over the plan's life. F&I and Showroom notes that running an in-house PPM program with unlimited services results in at least 50% of total sales revenue being gross profit.

Step 3: Choose Your Administrative and Risk Structure

This is the single decision with the greatest long-term financial impact.

Option 1: Third-Party White-Labeled Program

Purchase a white-labeled program from a third-party F&I product provider. This is simpler to set up but surrenders a significant share of profit.

Third-party administrators may take up to 60% of the value of cancelled services. They handle claims, compliance, and administration, but the dealer loses control over the customer experience and underwriting profit.

Option 2: Dealer-Administered Program

Structure the program internally — potentially through a dealer-owned reinsurance or administrator-obligor structure. This requires more setup but allows the dealer to retain underwriting profits.

F&I and Showroom notes that in-house programs give the dealer full control over plan terms, benefit decisions, and customer experience. Third-party programs may deny claims, creating customer dissatisfaction.

Dealers who have already established a dealer-owned reinsurance company can often fold a pre-paid maintenance product into that structure, capturing the same underwriting profits that would otherwise go to a third-party vendor.

DealerRE, for example, helps dealers integrate pre-paid maintenance products into existing administrator-obligor reinsurance companies, providing full-service administration including training, claims adjudication, compliance, and financial reporting.

The choice between these two structures can represent thousands of dollars per month in profit either retained or surrendered — making it worth getting right before launch.

Step 4: Address Legal and Compliance Requirements

Identify your state's classification. Determine whether your state classifies dealer-administered maintenance programs as service contracts, insurance products, or a distinct category. This determines what filings, reserves, or licenses may be required.

The NAIC Service Contracts Model Act excludes maintenance agreements from service contract regulation, but state adoption varies. Check your state's specific requirements.

Ensure contract compliance. Confirm that your program's contract language, cancellation and refund terms, and consumer disclosures comply with applicable state consumer protection laws. Work with a dealer attorney familiar with F&I product compliance.

FTC CARS Rule compliance. The FTC Combatting Auto Retail Scams (CARS) Rule, effective July 30, 2024, requires dealers to:

- Disclose that add-ons are not required to purchase or lease the vehicle

- Provide pricing disclosures including the specific charge and total cost over the repayment period

- Obtain express, informed consent through an interactive process

Civil penalties can reach up to $50,120 per violation.

Clarify third-party responsibilities. If using a third-party administrator, confirm what compliance responsibilities transfer to them and what the dealer remains responsible for.

DealerRE manages all legal forms, filings, tax returns, and renewals for dealers using its reinsurance structure, ensuring compliance with IRS Code 831(b) and state regulations.

Step 5: Train Your F&I Team to Present and Sell the Program

Build a consistent presentation script. Focus on convenience, locked-in pricing, and savings versus paying per visit. Avoid leading with product features.

Example value propositions:

- "Lock in today's service prices against future inflation"

- "Roll maintenance costs into your monthly payment"

- "Plans are transferable, increasing your vehicle's resale value"

Role-play common objections:

- "I can get cheaper oil changes elsewhere"

- "I'll just pay as I go"

- "I'm not sure I'll keep the car that long"

Each has a straightforward response. For example: "While quick-lube shops may advertise lower prices, they often don't include manufacturer-recommended filters or fluids, and they can't maintain your warranty records like we can."

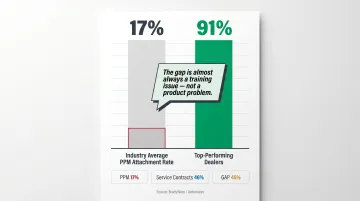

Set a target attachment rate. The industry average PPM attachment rate is only 17%, according to BradyWare/Autosweet, compared to 46% for service contracts and 45% for GAP. Some dealers achieve 90%-92% through optimized pricing and presentation.

That gap between 17% and 90% is almost always a training issue, not a product problem. Track your attachment rate weekly from day one — if the first 60 days underperform, revisit presentation before changing pricing or coverage.

DealerRE provides both online and in-person F&I training programs covering product analysis, claims adjudication, compliance, and performance reporting. These programs are designed to help F&I teams sell ancillary products like pre-paid maintenance with confidence.

Step 6: Launch, Monitor, and Refine

Start with a soft launch. Introduce the program to a subset of customers, gather redemption data and customer feedback, and use that information to refine pricing, coverage, or presentation before scaling.

Track three core metrics from day one:

- Attachment rate: Plans sold per vehicle sold

- Redemption rate: Services used per plan

- Downstream revenue per redeemed visit: Upsells, additional repairs

Together, these numbers show whether the program is generating F&I income at sale, driving service lane visits, and converting those visits into additional repair revenue.

Build a review cadence. Quarterly at minimum, assess whether plan pricing still covers your actual service costs, especially as parts and labor rates change over time.

DealerRE provides performance reports and financial analysis to dealers on their reinsurance programs, enabling ongoing monitoring and optimization.

Conclusion

A well-structured pre-paid maintenance program creates value at every stage: it increases F&I income at point of sale, brings customers back to your service drive, generates upsell revenue, and strengthens long-term loyalty. That return depends on getting the fundamentals right before the first plan is ever sold — choosing the right structure, pricing it accurately, and training your team. Dealers who nail those decisions find the program grows more profitable with each renewal cycle.

For those who structure the program through a dealer-owned reinsurance company, the financial advantage is even greater. Instead of paying third-party providers to administer and underwrite the product, the dealer keeps those profits and retains direct control over the customer experience — a compounding advantage that becomes more significant as plan volume grows.

Frequently Asked Questions

How does a prepaid maintenance plan work?

A customer pays a fixed upfront cost (often rolled into the vehicle purchase) to cover a defined set of scheduled maintenance services — such as oil changes and tire rotations — over a set term or mileage. They then redeem those services at the dealership's service department as needed.

Are prepaid car maintenance plans worth it for dealers to offer?

Yes. When properly structured and priced, pre-paid maintenance programs add F&I income per deal, drive repeat service traffic, and increase customer retention. That combination makes them one of the stronger ancillary products in any F&I menu.

What services should a dealer include in a prepaid maintenance program?

Most programs start with oil and filter changes, tire rotations, and multi-point inspections. More comprehensive tiers may add cabin filters, fluid services, or wiper blades. The key is only including services the service department can consistently and profitably deliver.

How do dealers make money on pre-paid maintenance programs?

Dealers profit two ways: the markup between the plan's cost to deliver and its retail sale price (captured at point of sale), and the downstream revenue from upsells during each service visit. Dealers who administer the program internally or through a reinsurance structure also capture underwriting profit.

What is the 30-60-90 rule for car maintenance?

The 30-60-90 rule refers to common manufacturer-recommended service intervals at 30,000, 60,000, and 90,000 miles, where specific inspections, fluid replacements, and component checks are due. For pre-paid maintenance programs, dealers often design coverage tiers around these intervals.

Can a pre-paid maintenance program be structured through dealer-owned reinsurance?

Yes. Some dealers integrate their pre-paid maintenance product into a dealer-owned administrator-obligor reinsurance structure, which allows them to retain the underwriting profit that would otherwise go to a third-party provider. That structure significantly increases the program's long-term financial return.