With F&I gross profit per vehicle retailed now averaging $2,505 in Q1 2025 — up 2.8% year-over-year — the spread between what dealers keep in a traditional arrangement versus a dealer-owned reinsurance structure has never been wider.

Genesis Reinsurance is one of the A-rated carriers backing dealer-owned admin obligor reinsurance programs. This article covers what that means, how the structure works, which products it supports, and how dealerships of every type can benefit — with DealerRE guiding the process from setup through long-term program management.

TL;DR

- Genesis Reinsurance is an A-rated carrier that backs dealer-owned admin obligor reinsurance companies, allowing dealers to replace third-party F&I providers and retain underwriting profits

- In an admin obligor structure, the dealer's reinsurance company becomes the obligor on VSCs and other products, backed by an A-rated carrier for financial security

- Products eligible for reinsurance include VSCs, GAP, ancillary F&I products, credit life, and BHPH-specific programs like collateral protection insurance

- Profits accumulate inside the dealer's reinsurance company, with potential tax advantages under IRC Section 831(b) — consult a tax advisor

- DealerRE has helped over 400 dealers build profitable reinsurance programs since 1994, covering setup, compliance, training, and administration

What Is Genesis Reinsurance?

Genesis Reinsurance is an A-rated carrier that provides the insurance backing for dealer-owned admin obligor reinsurance companies. In the F&I space, that distinction matters. Genesis Reinsurance is not a third-party product provider selling VSCs or GAP at a markup — it's the financial security layer sitting behind a dealer's own reinsurance company.

The "A-Rated" Designation and Why It Matters

AM Best's Financial Strength Rating (FSR) is an independent assessment of an insurer's ability to meet ongoing policy obligations. The rating scale runs from D (Poor) to A++ (Superior), with A and A- classified as "Excellent."

For dealers, an A-rated carrier backing their reinsurance program provides two things:

- Customer assurance — claims on the dealer's F&I products are supported by a financially sound carrier

- Program stability — the dealer's reinsurance structure rests on a carrier with verified capacity to honor obligations

Dealers evaluating any reinsurance program should verify current carrier ratings directly through AM Best's FSR database or the NAIC Consumer Information Source.

The Historical Foundation

Dealer-owned reinsurance is not a new concept. The model originated in the 1950s, when Texas dealers began forming state-domiciled insurance companies to reinsure credit life and disability products. The concept has been in practice for more than 30 years, and reinsurance companies have grown into major factors in the marketing of credit life and extended vehicle service contracts.

The admin obligor structure places an administrative company as the legal obligor on F&I contracts, not the selling dealership directly. Within this structure, the dealer's reinsurance company captures underwriting profits while the A-rated carrier — Genesis Reinsurance — provides the financial credibility that makes the program viable.

DealerRE helps dealers access and structure these programs, handling everything from company formation to ongoing compliance, so dealers can stay focused on running their business.

How Does Genesis Reinsurance Work for Auto Dealers?

The Premium Flow, Step by Step

Here's the basic mechanics of an admin obligor reinsurance program:

- Dealer sells an F&I product (VSC, GAP, ancillary coverage) to a customer

- Premium flows into the dealer's reinsurance company, held in a U.S.-based trust account

- Genesis Reinsurance backs the program as the A-rated carrier, providing financial security on the dealer's obligations

- The dealer's reinsurance company invests reserves conservatively — typically in government bonds — earning investment income that stays inside the dealer's structure

- Reserves pay claims as they occur; the remainder accumulates as underwriting profit for the dealer

- Excess funds become available once trust account balances exceed 125% of unearned premiums, at which point the dealer can direct more aggressive investment or begin withdrawals

Compare that to the traditional model: front commission paid to the dealer, all remaining underwriting profit retained by the third-party provider. The dealer has no reserve accumulation, no investment income, and no long-term wealth building from the products they sold. That structural gap extends beyond finances — it also affects how your customers are treated after the sale.

Claims Control and Customer Experience

One of the structural advantages dealers cite most often is claims control. In a standard third-party arrangement, the provider adjudicates claims — and the dealer has no influence over how that process is handled or how customers are treated.

In a DealerRE-administered admin obligor program, claims adjudication is part of the dealer's own program. That means:

- The dealer's customers are handled through the dealer's own reinsurance structure

- Repairs can be driven back to the dealer's service department, keeping revenue in the dealership's ecosystem

- The dealer controls the ownership experience rather than depending on a third party to represent their brand

Compliance and Legal Structure

A properly administered program manages the full compliance stack. DealerRE handles all legal forms, filings, tax returns, and renewals — including:

- Licensing coordination

- Annual Form 1120-PC filings with insurance tax specialists

- Coordination with CPAs and legal counsel to ensure the reinsurance entity meets applicable IRS codes and state regulations

Under IRC Section 831(b), qualifying small insurance companies with net written premiums not exceeding $2,200,000 may elect to be taxed only on investment income rather than total underwriting income. For dealers whose reinsurance company falls within this threshold, that election can represent meaningful tax savings — though all tax planning should be reviewed with a qualified tax advisor, as individual circumstances vary.

Products and Services Covered Under a Genesis Reinsurance Program

The product scope of a Genesis Reinsurance-backed admin obligor program extends well beyond VSCs. Here's how the major categories break down:

Vehicle Service Contracts (VSCs)

VSCs are the dominant product in dealer reinsurance. The U.S. VSC market was valued at approximately $22 billion in 2024 and is projected to exceed $31 billion by 2032. Under a Genesis Reinsurance-backed admin obligor structure, the dealer's reinsurance company replaces the manufacturer or third-party warranty provider as the party capturing underwriting profit. Reinsuring VSCs is effectively owning a warranty company built solely for your store and your customers.

GAP Insurance and Ancillary Products

GAP coverage can also be structured through the dealer's reinsurance company. GAP penetration has reached approximately 35.39%, with income up roughly 3% per deal, adding measurable lift to total reinsurable F&I income. Ancillary products that also flow through DealerRE programs include:

- Tire & wheel protection

- Door ding / paintless dent repair

- Theft deterrent / window etching

- Windshield repair

Credit Life and Disability Insurance

Dealer-owned reinsurance originated specifically to capture underwriting profit on credit life and disability products. Dealers offering these products today can structure them within the reinsurance framework the same way they handle VSCs and GAP — keeping more of every dollar earned.

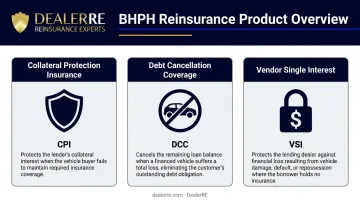

BHPH-Specific Programs

Buy Here Pay Here dealers operate with a distinct risk profile, and the program structure reflects that. Key BHPH-specific products include:

- Collateral Protection Insurance (CPI) — force-placed coverage protecting the dealer's collateral when customers fail to maintain required insurance; can be reinsured to capture underwriting profit

- Debt Cancellation Coverage (DCC) — covers the total debt owed if a vehicle is a total loss, allowing the dealer to get the customer into another vehicle

- Vendor Single Interest (VSI) — protects the lender against vehicle damage or repossession loss

For BHPH dealers, VSC premiums are financed over the loan term and billed monthly as payments come in. Dealers aren't required to fund the full cost upfront, which protects cash flow and the lending pool while still capturing all underwriting profit at term expiration.

Financial Benefits Dealers Gain Through Genesis Reinsurance

Profit Recapture

The core financial argument is straightforward: every dollar of underwriting profit that flows to a third-party provider is a dollar the dealer generated but didn't keep. DealerRE frames the question bluntly to prospective clients — if the third-party provider weren't making a profit off the dealer, why would they continue the relationship?

Dealers running 150 GAP contracts annually at $499 each are generating $74,850 in premium that, under a reinsurance structure, stays inside their own company. DealerRE clients have captured hundreds of thousands of dollars in underwriting profit through reinsured programs that previously generated only front-end commissions.

Investment Income and Reserve Accumulation

Premium reserves held in the dealer's trust account earn investment income throughout the policy term — and that income belongs to the dealer's reinsurance company, not the carrier. The trust structure starts with conservative investments (government bonds), then allows more aggressive positioning once reserves exceed 125% of unearned premiums. Under a standard third-party arrangement, the dealer collects a front commission and nothing more. Reinsurance generates returns on both underwriting performance and reserve investment.

Deploying Accumulated Profits

Dealers who build reserves inside their reinsurance company have flexibility in how they use those funds. DealerRE clients have directed accumulated profits toward:

- Real estate acquisitions

- Reinvestment in dealership operations or expansion

- College education funding

- Personal wealth accumulation

For many dealers, that flexibility is what moves reinsurance from an F&I tactic to a long-term wealth strategy — one they control entirely.

Which Types of Dealerships Are a Good Fit?

Franchise and Independent Retail Dealers

Both franchise and independent used-car dealers can access Genesis Reinsurance-backed admin obligor programs. DealerRE's threshold for program suitability generally starts at dealers selling more than 30 cars per month — below that volume, the economics of a full reinsurance structure don't justify the setup cost. Above that threshold, the program is designed to scale with volume.

With approximately 16,990 franchised dealerships and an estimated 52,000 active independent dealers in the U.S., the addressable market is large — and the majority of those dealers are leaving underwriting profit in the hands of third-party providers.

BHPH Dealerships

BHPH dealers have a distinct path through Genesis Reinsurance, with a structure built around their specific business model. Rather than replacing manufacturer VSC providers, BHPH programs protect the dealer's vehicle portfolio through:

- CPI (Collateral Protection Insurance) — covers insurance-funded losses on the dealer's portfolio

- DCC (Debt Cancellation Coverage) — handles cancellation events tied to the loan

- VSI (Vendor's Single Interest) — protects the dealer's financial interest in financed vehicles

- VSC Reinsurance — covers mechanical breakdown losses across the portfolio

The monthly billing structure accommodates the cash flow realities of the BHPH model without disrupting the dealer's lending pool.

How DealerRE Guides Dealers Through a Genesis Reinsurance Program

Full-Service Setup and Onboarding

DealerRE manages the entire process of establishing a dealer's reinsurance company — from company formation and domicile selection through legal filings, licensing coordination, and compliance setup. Key elements:

- All legal forms, filings, tax returns, and renewals managed by DealerRE

- Tax preparation coordinated with insurance tax specialists

- Compliance with IRS Code 831(b) requirements and state contract/policy approvals

- Staff onboarding through the DealerRE Training Academy (online and in-person)

DealerRE doesn't cut corners on compliance or tax structure. Dealers with existing programs that don't meet current IRS standards should assess their audit exposure — the structure matters as much as the economics.

Ongoing Program Management

Support doesn't stop at launch. DealerRE provides:

- Monthly financial statements covering all reinsurance operations activity

- Performance reporting and analysis tracking program profitability

- Claims adjudication through the program administrator

- F&I training — both online courses and in-person sessions

- F&I menu development to maximize product penetration and per-vehicle profitability

- Periodic ownership reviews to assess financial direction and reserve deployment

DealerRE's Track Record

Since Tim Byrd founded DealerRE in 1994 in Southeast Virginia, the company has helped over 400 auto dealers build more profitable F&I programs through reinsurance. The client roster includes dealers recognized as National Quality Dealer of the Year, NIADA Board Members, State Quality Dealer of the Year, and state association presidents.

Frequently Asked Questions

What is Genesis Reinsurance in the context of auto dealerships?

Genesis Reinsurance is an A-rated carrier that backs dealer-owned admin obligor reinsurance companies, enabling dealerships to replace third-party F&I product providers and retain underwriting profits within their own reinsurance company rather than forfeiting those profits to an outside provider.

How does an admin obligor reinsurance structure differ from a traditional third-party F&I arrangement?

In a traditional arrangement, the third-party provider retains all underwriting profits and controls the claims process. In an admin obligor structure, the dealer's own reinsurance company is the obligor on the product, retaining those profits, with an A-rated carrier like Genesis Reinsurance providing the financial backing.

What F&I products can be covered through a Genesis Reinsurance-backed program?

Common products include:

- Vehicle service contracts and GAP insurance

- Ancillary products: tire and wheel, door ding, theft protection, windshield repair

- Credit life insurance

- BHPH-specific programs: collateral protection insurance, debt cancellation coverage, and vendor single interest

Are there tax advantages to owning a dealer reinsurance company backed by Genesis Reinsurance?

Profits accumulating inside a dealer-owned reinsurance company may offer tax planning advantages, particularly under IRC Section 831(b), which allows qualifying companies with net written premiums under $2,200,000 to be taxed only on investment income. Consult a qualified tax advisor for guidance specific to your dealership.

Can independent and BHPH dealers qualify for a Genesis Reinsurance program?

Yes. Both independent and BHPH dealers can access these programs, with structures tailored to their specific business models. DealerRE generally works with dealers selling more than 30 vehicles per month, with program design adapted to whether the dealer is a retail, independent, or buy-here-pay-here operation.

How does DealerRE help dealers get started with a Genesis Reinsurance program?

DealerRE handles company formation, legal filings, licensing coordination, compliance management, and staff training, along with ongoing administration covering claims adjudication, financial reporting, and F&I menu development. Call (804) 824-9533 to begin a program analysis.