Introduction

Most dealers running a reinsurance program have heard the term "fronting company" without ever getting a straight answer about what it costs, what it requires, or why it matters. That gap creates real problems — especially when fee structures and collateral obligations catch dealers off guard.

A fronting program is the legal mechanism that allows your reinsurance company to operate across state lines without holding individual insurance licenses in every state. Without it, your program cannot legally issue F&I contracts to consumers. That's a licensing requirement with direct consequences for how your program is structured and what it costs to run.

This article covers how the money flows, what fees and collateral to expect, and where dealers most often misread the cost picture. Whether you're running a CFC, a DOWC, or an admin obligor program, the fronting mechanics directly affect your bottom line.

TL;DR

- A fronting company is a licensed insurer that issues F&I product policies on your behalf, satisfying state licensing and lender requirements

- Without a fronting arrangement, your reinsurance company cannot legally underwrite F&I products in most states

- Fronting fees typically run 6–10% of gross written premiums, covering policy issuance, premium tax compliance, and claims infrastructure

- Collateral requirements are commonly set at 125–150% of projected losses, which affects your liquidity and investment flexibility

- Net premium after all deductions — not the fronting fee alone — is what determines real program profitability

What Is a Fronting Program in Dealer Reinsurance?

A fronting program involves a licensed, admitted insurer — the "fronting company" or "front" — issuing insurance policies for F&I products on behalf of your reinsurance company. Your reinsurance entity (a CFC, DOWC, or admin obligor company) typically holds no insurance licenses outside its domicile. The fronting company provides the licensed paper. Risk transfers back to your reinsurance company through a reinsurance contract.

According to Captive.com, fronting is "the use of a licensed, admitted insurer to issue an insurance policy on behalf of a self-insured organization or captive insurer" — and critically, the fronting insurer "does not intend to bear any of the risk."

What This Arrangement Accomplishes

Your reinsurance company gains the legal standing to operate across multiple states and satisfy contractual requirements — without you obtaining individual state insurance licenses. This is not self-insurance. You're not simply buying coverage from a third-party administrator either.

Your reinsurance company is the actual risk-bearer. It just operates through a licensed intermediary that holds the regulatory standing. Because your entity bears the risk, it also captures the financial upside — which is where the economics of a fronting program come into focus:

- The fronting company earns a fee for providing licensed paper and compliance access

- Your reinsurance company retains the underwriting profit on favorable claims experience

- Investment income on held reserves accumulates inside your entity over time

Why Dealer Reinsurance Programs Require a Fronting Company

The Licensing Problem

Dealer-owned reinsurance companies — CFCs, DOWCs, NCFCs — are generally not licensed as admitted insurers in every state where their F&I products are sold. Under U.S. insurance law, unlicensed insurers cannot issue policies directly to consumers. A fronting arrangement is the legal solution.

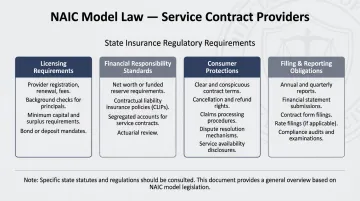

The NAIC Service Contracts Model Act (Model 685) makes the requirement explicit: service contract providers must "insure all service contracts under a reimbursement insurance policy issued by an insurer authorized to transact insurance in this state." The alternatives — maintaining funded reserves at 40% of gross premiums plus deposits, or holding $100 million in net worth — are not realistic options for most dealerships. Fronting is the practical path.

Lender and Contractual Requirements

Finance companies, lenders, and vehicle lessors commonly require F&I products to be backed by an insurer carrying a minimum AM Best rating — typically A (Excellent) or A-. The fronting company's AM Best rating is what appears on the product. Your reinsurance company's rating is irrelevant to those counterparties.

What lenders and lessors are actually checking:

- Whether the backing insurer holds a qualifying AM Best rating

- Whether the issuing carrier is licensed in the relevant state

- Whether the policy structure satisfies their contractual requirements

Your dealer-owned reinsurance company satisfies none of those checks on its own. The fronting carrier does.

What Happens Without Proper Fronting

The Microsoft subsidiary Cypress Insurance Company learned this the hard way. Washington state issued a cease-and-desist order to Cypress after finding it had written policies in the state without a licensed fronting arrangement — resulting in a bill for over $2 million in back taxes and fees. The company resolved the matter only after securing a Washington-licensed fronting carrier.

Secondary Services Fronting Provides

Policy issuance is just the start. Your fronting company also handles:

- Premium tax compliance and state filings

- Certificate of insurance issuance

- Claims handling infrastructure

- Guarantee fund participation (protecting your customers if the fronting carrier becomes insolvent)

These are services you'd otherwise need to source and manage independently.

How a Fronting Program Works in Practice

The Core Flow

The fronting company and your reinsurance company execute two agreements: a fronting agreement and a reinsurance contract. When an F&I product sells, the fronting company issues the policy under its licensed paper. The premium — minus the fronting fee — is ceded into your reinsurance trust, where it sits as an Unearned Premium Reserve (UPR) until claims are paid or the contract term expires.

Step 1: Policy Issuance and Premium Split

The fronting company issues the contract. The premium is immediately divided:

- The fronting fee stays with the fronting company

- The net premium flows into your reinsurance trust

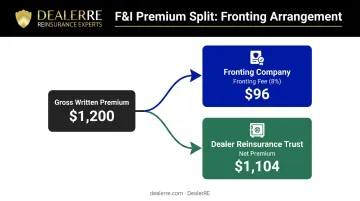

Example: On a $1,200 premium with an 8% fronting fee, $96 stays with the front and $1,104 flows into your dealer trust. That $1,104 becomes your working reserve — the pool from which claims are paid and profit eventually emerges.

Step 2: Risk Transfer and Reserve Management

Through the reinsurance contract, the fronting company transfers the risk of loss to your reinsurance company. The ceded premium enters the UPR, which is subject to conservative investment restrictions during this phase.

All trust funds are held in the United States and invested in assets acceptable to insurance regulatory authorities. Permitted instruments during the UPR phase include:

- Government bonds and short-term fixed instruments

- Assets meeting state insurance regulatory standards

Equities, alternative investments, and most foreign-issued instruments are prohibited or sharply restricted at this stage, consistent with Reg 114 trust standards.

Step 3: Profit Recognition and Surplus

Once the UPR phase matures, the mechanics shift. When contract terms expire and claims are settled, unused UPR funds become earned surplus in your reinsurance account. Investment restrictions loosen at that point — funds exceeding 125% of unearned premiums can be invested more aggressively or accessed by company ownership.

That combination of underwriting profit and investment income, accumulated inside a company you own, is the core financial case for dealer reinsurance. Through its admin obligor structure, DealerRE manages the legal forms, filings, compliance, and administration on the dealer's behalf — so the program runs without adding operational burden to the dealership.

Fronting Fees and Collateral: What Dealers Should Expect

Fronting Fee Range

The fronting fee is charged as a percentage of gross written premiums. Multiple industry sources cite the following ranges:

| Source | Fee Range Cited |

|---|---|

| Captive.com | 6–10% (fronting fee component) |

| Insurance Training Center | 5–15% |

| Captive International (2024) | 3–10% or more |

| Bender Insurance Solutions | 6–30% (all-in, including premium taxes and guarantee fund) |

The wide variation reflects what's included. The fronting fee alone typically falls in the 6–10% range. Total program costs — once premium taxes, guarantee fund participation, and other pass-throughs are added — run higher. When comparing quotes, confirm which number you're actually looking at.

What Drives Fee Variation

- Scope of services: Does the fronting company handle claims, or just issue paper?

- Premium volume: Higher volume often creates negotiating power

- Dealer's collateral strength: Stronger collateral positions can lower the fee

- Interest rate environment: Higher rates increase the value of withheld funds to the fronting carrier

Collateral Requirements

Fee variation is only part of the cost equation. Because the fronting company carries primary legal liability on every policy it issues, it also requires security from your reinsurance company. According to The Self-Insurer, fronting companies "can require collateral upwards of 125 to 150 percent of projected losses."

The three common collateral mechanisms:

- Funds withheld — the fronting company holds back a portion of ceded premiums

- Reg 114 trust — your reinsurance company funds a trust with U.S. government securities and investment-grade instruments; the fronting carrier can draw on it unilaterally if you fail to perform

- Letter of credit — a bank-issued guarantee, typically secured by your investment securities

Each option affects how accessible your capital is and how early you can generate investment returns. Evaluate them based on your liquidity position and program size.

The Total Cost Picture

Dealers who focus only on the fronting fee percentage miss the full picture. Before selecting a structure, model your net premium available for reserve-building after accounting for:

- Fronting fee

- Administrator fees

- Premium taxes

- Investment management fees

- Claims adjudication costs

Ask for complete fee disclosure at the outset and insist on seeing every line item before signing — regardless of which administrator you work with.

Common Misconceptions About Fronting in Dealer Reinsurance

"The Fronting Company Shares the Risk"

It doesn't. The fronting company's exposure is credit risk — the risk that your reinsurance company fails to reimburse claims as agreed. That's why collateral exists. The fronting carrier earns a fee for compliance access and services, not for taking on underwriting exposure.

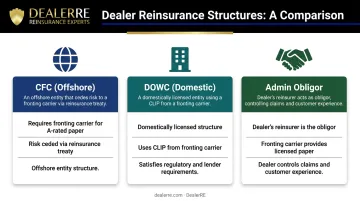

"All Dealer Reinsurance Structures Use Fronting the Same Way"

They don't. Here's how fronting applies differently across common structures:

- CFC (offshore): Requires a fronting carrier to issue A-rated paper; the fronting carrier cedes risk to the offshore entity via reinsurance treaty

- DOWC (domestic): A domestically licensed insurance entity that purchases a Contractual Liability Insurance Policy (CLIP) from a fronting carrier to satisfy regulatory and lender requirements

- Admin obligor: The dealer's reinsurance company is the obligor on F&I contracts; the fronting carrier provides licensed paper and regulatory backing while the dealer controls the customer and claims experience

The structural nuances matter when you're evaluating which program fits your dealership's size, state of domicile, and profitability goals.

"Collateral and UPR Restrictions Are Minor Details"

Dealers often fixate on the fronting percentage and overlook two factors that directly affect early-stage returns:

- Collateral requirements tie up capital — often 125–150% of projected losses — limiting how aggressively you can invest or access funds early on

- UPR investment restrictions keep reserves in conservative instruments until the threshold is met, slowing returns in the program's first years

There's also a less-discussed exposure worth understanding: fronting carrier insolvency. If your fronting carrier fails, your customers are protected by state guaranty funds (because the fronting carrier is the admitted insurer of record), and your trust assets remain protected within the Reg 114 trust structure. Even so, verify AM Best ratings before committing to any program. DealerRE structures its admin obligor programs exclusively with A-rated insurers for exactly this reason.

Frequently Asked Questions

What is a fronting company in reinsurance?

A fronting company is a licensed, admitted insurer that issues policies on behalf of an unlicensed reinsurance entity — such as a dealer's reinsurance company — satisfying regulatory and contractual requirements. The fronting company transfers the actual risk back to the reinsurance entity through a reinsurance contract and is compensated by fee rather than risk participation.

What is the fronting fee in reinsurance?

The fronting fee is a charge — typically 6–10% of gross written premiums — that the fronting company receives for lending its license, issuing policies, handling compliance, and carrying credit risk. It covers policy issuance, premium tax payments, guarantee fund participation, and sometimes claims handling infrastructure.

Do all dealer reinsurance programs require a fronting company?

Most do. CFCs, NCFCs, and admin obligor programs all require a fronting arrangement to legally issue F&I products across states. DOWCs use a CLIP from a fronting carrier rather than a traditional fronting agreement, but still rely on a licensed carrier for insurance backing.

What collateral does a fronting company require?

Fronting companies typically require collateral equal to 125–150% of projected losses, posted as withheld funds, a Reg 114 trust funded by investment securities, or a letter of credit. The mechanism you choose affects your liquidity and how quickly you can access surplus funds as contracts earn out.

How does a fronting arrangement affect the dealer's access to reinsurance profits?

The fronting fee and collateral requirements reduce net premium flowing into your reinsurance trust, but they don't prevent profit accumulation. Underwriting profit and investment income still build inside your reinsurance company as premiums earn out — the fronting structure determines when and how you access them, not whether you capture them.

What is the difference between a fronting arrangement and an admin obligor structure?

In an admin obligor structure, the dealer's reinsurance company is the obligor on F&I contracts (the entity responsible for paying claims), while the fronting carrier provides licensed paper and regulatory backing. This gives the dealer direct control over the claims process and customer experience — a more integrated arrangement than a standard CFC structure.