The problem isn't the program structure. It's the data.

According to IML, a Bermuda-based captive insurance consultancy, many captives still rely on static spreadsheets or fragmented claims records, which limits their ability to analyze trends, forecast losses, or satisfy governance requirements. That's not just an inconvenience — it's a structural risk.

This article covers what centralized data access actually means for dealer reinsurance programs, which data streams matter most, and how consolidating that information leads to better claims control, stronger profitability, and more confident decision-making.

TL;DR

- Dealer reinsurance data is typically scattered across F&I systems, TPA portals, spreadsheets, and delayed financial statements — making it nearly impossible to manage proactively

- A healthy dealer reinsurance loss ratio falls between 50% and 65%; you can't manage that benchmark without product-level data

- Four data streams matter most: premium/contract data, claims/loss data, reserve/financial data, and F&I performance benchmarks

- Centralized data requires a disciplined administration model: consistent reporting structures and regular review cycles, not a one-time technology fix

- A full-service administrator like DealerRE is the most practical path to data centralization — no extra headcount required

What Is Centralized Data Access in Dealer-Owned Reinsurance?

Centralized data access in dealer reinsurance means having a single, consolidated view of everything flowing through your program — premium intake, claims activity, investment performance, and F&I product-level results. Instead of pulling numbers from disconnected sources, it all comes through one consistent reporting structure.

Traditional insurance carriers focus on policy systems and claims portals — that model doesn't translate to dealer-owned programs. For a dealer-owned reinsurance company, the challenge is aggregating information that spans three distinct environments: the dealership's F&I office, the administrator's claims process, and the reinsurance company's financials.

What Centralized Reporting Looks Like in Practice

For most dealer programs, a centralized reporting environment surfaces:

- Loss ratios broken down by product type

- Premium performance by month and by vehicle category

- Claims frequency and average cost trends

- Reserve balances and adequacy status

- Investment income generated on premium funds

The key is that all of this comes from one accountable reporting structure, on a consistent schedule, in a consistent format.

Centralization doesn't require complex software or a full IT buildout. For most dealers, it's achieved through a well-managed administration model where one party owns data accuracy, reporting regularity, and making sure the dealer always has the complete picture.

That only works when the dealer, F&I team, and reinsurance administrator are operating from shared data definitions, consistent reporting schedules, and agreed-upon performance benchmarks — not their own versions of the numbers.

Why Most Dealer Reinsurance Programs Operate Without Clear Data Visibility

Many dealer-owned reinsurance companies were set up with a primary focus on capturing premium income, not on building a framework for ongoing data review. Years later, dealers often can't tell whether their program is performing at its potential or falling behind.

How Fragmentation Happens

The pattern is predictable. F&I managers track product sales in the DMS. Claims get adjudicated by a third party that sends reports in inconsistent formats. Reserve calculations happen in a spreadsheet. Financial statements arrive months after the reporting period closes. By the time the dealer reviews results, the data is stale — and the opportunity to course-correct has passed.

A Deloitte survey of insurers found that only about one in three characterized their data as "very effective" at supporting decision-making, while one in five rated their data governance as outright ineffective. Dealer-owned reinsurers, operating with far fewer resources than large carriers, face these challenges at greater intensity.

The Specific Risk for Dealer-Owners

That fragmentation hits dealer-owners harder than most. The dealer is simultaneously the seller of the F&I product and the risk-bearer through the reinsurance company. Without clear data visibility, there's no way to know whether what the finance office is selling is actually profitable for the entity the dealer owns.

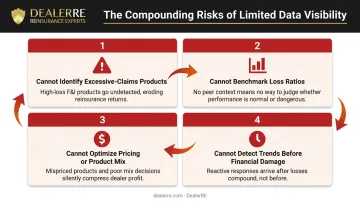

That blind spot creates four compounding problems:

- Can't identify which products are generating excessive claims

- Can't benchmark loss ratios against program expectations

- Can't make informed decisions about pricing, coverage terms, or product mix

- Can't detect developing trends until financial statements confirm a problem that's been building for 12 months or more

F&I revenue flowing through dealer reinsurance programs is near historic highs — averaging $2,505 in F&I gross profit per vehicle retailed in Q1 2025, according to Haig Partners. A larger premium pool means more profit potential — but also more exposure when the data to manage it simply isn't there.

The Key Data Streams That Should Feed Your Dealer Reinsurance Program

Four data streams form the core of any well-managed dealer reinsurance program. Each answers a different question — about exposure, risk performance, financial health, or selling behavior.

1. Premium and Contract Data

This is your exposure baseline. It tells you how much premium has been written by product type, contract term, vehicle age, and selling F&I manager. Without it, you're projecting future program performance without knowing what risk you've actually taken on.

2. Claims and Loss Data

This is the most direct measure of whether your reinsurance program is absorbing risk as expected, or experiencing adverse selection. Key metrics include:

- Claim frequency by product and vehicle segment

- Average claim cost

- Time-to-close

- Product-level loss ratios compared against benchmarks

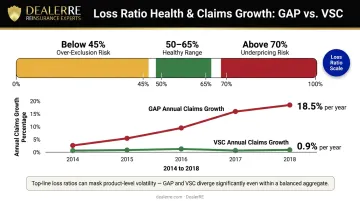

A healthy long-term loss ratio for a mature dealer reinsurance program typically falls in the 50% to 65% range. Sustained ratios above 70% signal underpricing or weak underwriting controls. Below 45% may indicate excessive exclusions. The important detail: a single aggregate loss ratio can mask dangerous trends in individual product lines.

GAP products, for instance, show sharply different volatility than vehicle service contracts. VSC claims on used vehicles rose roughly 0.9% annually from 2014 to 2018, while used-vehicle GAP payouts jumped an average of 18.5% per year over the same period. If you're only watching the top-line number, a deteriorating GAP portfolio can hide behind stable VSC performance.

3. Reserve and Financial Data

This connects operational results to wealth-building. Reserve and financial data covers three core areas:

- Reserve adequacy by cohort

- Investment income on premium funds held in the reinsurance company

- Overall program net income

Regulatory obligations also live here. Underfunded reserves can trigger intervention, and filing deadlines don't adjust for disorganized data.

4. F&I Performance Benchmarks

Front-end selling behavior drives downstream reinsurance results. Penetration rates by product, average retail selling price, and finance office gross per deal are the leading indicators to watch. If claims on a specific product are rising, the answer may live in how that product is being sold, to whom, and on which vehicles.

DealerRE consolidates all four of these streams into structured performance reports delivered to dealer clients monthly, along with periodic strategic reviews to walk through operational and financial direction together. Rather than reconciling data from a separate TPA, a separate accountant, and their own DMS, everything flows through one accountable structure.

How Centralized Data Directly Improves Claims Experience Management

One of the primary reasons dealers own reinsurance companies is control: specifically, control over the claims experience. That control only holds when claims data is timely and accurate.

Without centralized visibility, a dealer may not realize for 6 to 12 months that a specific product or vehicle segment is driving claim costs above acceptable levels. By then, the losses have already accumulated.

What Proactive Management Looks Like

With consolidated claims data reviewed consistently, dealers can:

- Identify which vehicle makes or model years are generating disproportionate mechanical breakdown claims

- Adjust coverage parameters for high-loss categories before losses compound

- Work with the F&I team to shift product recommendations away from high-risk inventory segments

- Detect IBNR (incurred but not reported) exposure before it creates reserve deficiencies

There's also a regulatory dimension. Fragmented, delayed claims data makes it harder to provide prompt reinsurance notification — and failure to notify can result in complete denial of coverage under standard captive claims handling requirements. Centralized data protects both reserve adequacy and reinsurance recovery rights at once.

Arizona is one of the most common domicile choices for dealer-owned captives, and its compliance requirements are representative of what dealers face regardless of where their entity is structured. Arizona-domiciled captives must file annual financial statements within 90 days of fiscal year-end and audited reports within six months. That timeline requires organized, accessible data year-round — not a last-minute scramble when deadlines hit.

From Data to Decisions: Practical Strategies for Centralizing Your Dealer Reinsurance Data

Centralization is less about technology and more about discipline. Here's where to start.

Establish a Standardized Reporting Cadence

At minimum, all key program metrics should be reviewed quarterly in a consistent format. Annual-only reviews are inadequate — claims cost inflation can develop within a single quarter, and adverse trends won't wait for year-end statements.

Monthly financial statements from your administrator, combined with a structured quarterly review, create the rhythm needed to catch and correct problems before they compound.

Align the F&I Team with Program Performance

Since the dealership's selling behavior directly drives premium volume and risk selection, F&I managers should understand how their product presentations connect to reinsurance outcomes. A simple F&I-to-reinsurance performance bridge — showing the link between product mix, vehicle selection, and downstream loss ratios — transforms the finance office from an isolated revenue center into an active participant in program management.

That shift happens when F&I-level data and reinsurance financials are reviewed together, not in separate conversations.

Work with a Full-Service Administrator

The most practical path to data centralization for most dealers is partnering with a full-service administrator who handles core program functions under one umbrella — eliminating the coordination gaps that create data silos in fragmented setups. That typically includes:

- Claims adjudication and processing

- Compliance management and filings

- Performance reporting and analysis

- Financial statements and bookkeeping

That single point of accountability means your data doesn't have to travel through three vendors before it reaches you.

DealerRE has operated as a full-service reinsurance administrator since 1994, working with more than 400 auto dealers nationwide. For dealers concerned about visibility gaps, stale reporting, or disconnected product-level data, a program review can quickly identify where consolidation would make the biggest difference.

Frequently Asked Questions

What data should a dealer regularly review in their own reinsurance company?

Dealers should review premium volume by product, claims frequency and cost trends, reserve adequacy, and net program income — at minimum quarterly. Monthly financial statements from the administrator provide the foundation; periodic strategic reviews help interpret trends and adjust course.

How does centralized data help a dealer control their claims experience?

When claims data is consolidated and reviewed consistently, dealers can identify high-loss product types or vehicle segments early, allowing them to adjust coverage, pricing, or selling strategy before losses erode profitability. Without that visibility, problems build silently for months.

What is the difference between a data silo and a centralized data approach in dealer reinsurance?

A data silo occurs when premium, claims, and financial information lives in separate, unconnected places: spreadsheets, third-party portals, delayed statements. A centralized approach consolidates that information into one consistent reporting structure, delivered on a regular schedule by a single accountable administrator.

Can a small or mid-size dealership realistically centralize their reinsurance data?

Yes. Data centralization in dealer reinsurance doesn't require sophisticated technology. It requires a disciplined administrator who produces structured, consistent reports and a dealer who commits to reviewing them regularly. The process, not the platform, is what matters.

How does F&I performance data connect to reinsurance program results?

The dealer sells F&I products through the finance office and reinsures them through their own company. What F&I managers sell, how they price it, and to which customers directly shapes the risk profile and profitability of the reinsurance program. Front-end and back-end data need to be reviewed together.

What happens when a dealer-owned reinsurance program lacks regular data reporting?

Without regular data review, loss ratios deteriorate undetected and reserves become inadequate. By the time financial statements reveal the problem, it may have been building for 12 months or more — and corrective action at that point is far more costly.