That distinction matters. When you understand how assumption reinsurance actually works — who owns the obligation, who carries the liability, and where the money flows — you start seeing your F&I program differently. Specifically, you start asking why a third party is the one assuming your customers' risk and keeping the underwriting profit that comes with it.

This article breaks down assumption reinsurance from the ground up: what it is, how it works mechanically, how it differs from traditional indemnity reinsurance, and what the concept means for dealers looking to build their own reinsurance programs.

TLDR

- Assumption reinsurance transfers an insurer's full obligations — including direct liability to policyholders — to a reinsurer, not just financial risk behind the scenes

- The original insurer is released entirely; the assuming company becomes the insurer of record

- Policyholder consent and regulatory approval are required in most U.S. states to complete the transfer

- Dealer-owned reinsurance programs use this structure to redirect underwriting profits back to the dealership instead of a third-party provider

What Is Assumption Reinsurance?

Assumption reinsurance is a specific type of reinsurance agreement in which the assuming (reinsuring) company takes over the ceding insurer's complete contractual obligations for a defined set of policies. The assuming company becomes directly liable to policyholders — not just financially exposed behind the scenes.

Three parties are involved:

- The ceding company — the original insurer transferring its risk and obligations

- The assuming company — the reinsurer that accepts full responsibility for the transferred policies

- The policyholder — who now has a direct legal relationship with the assuming company, not the original insurer

The NAIC Assumption Reinsurance Model Act (MO-803) defines an assumption reinsurance agreement as any contract that "both transfers insurance obligations and is intended to effect a novation of the transferred contract of insurance with the result that the assuming insurer becomes directly liable to the policyholders."

How It Differs From Indemnity Reinsurance

This distinction defines how each structure actually works. In standard indemnity reinsurance, the original insurer stays on the hook to policyholders — the reinsurer simply reimburses losses. Policyholders may never know a reinsurer is involved at all.

In assumption reinsurance, that relationship changes completely. The ceding insurer is released from those obligations. The assuming company is no longer a backstop — it becomes the new insurer of record.

The Concept of Novation

Assumption reinsurance is legally structured as a novation — the substitution of one party for another in a contract. Investopedia defines novation as "the replacement of one of the parties in a two-party agreement with a third party, with the agreement of all three parties," extinguishing the original obligation and creating a new one.

Because the policyholder's counterparty is changing, all three parties — original insurer, assuming insurer, and policyholder — must consent. Most states legally require policyholder notification and affirmative approval before the transfer takes effect.

The Regulatory Framework

The NAIC Model Act provides a framework many states have adopted to govern these transactions. As of 2022, 11 states have enacted it in substantially similar form, including Georgia, Kansas, Maine, Nebraska, and Oregon. Other states, like Illinois (215 ILCS 5/1705), maintain their own specific statutes.

Where states haven't adopted the Model Act directly, related insurance regulations still apply. Dealers operating across state lines should confirm which statutes govern each jurisdiction before structuring a transaction.

How Assumption Reinsurance Works: The Key Mechanics

Identifying the Need and Structuring the Transfer

A ceding insurer typically initiates assumption reinsurance when it wants a clean exit from a block of policies — not just risk-sharing. Common triggers include exiting a line of business, improving capital ratios, or restructuring after an acquisition.

The reinsurance agreement specifies:

- Which policies are included in the transfer

- The effective date of the transaction

- How premiums and reserves are handled

- That the assuming company takes over all rights, liabilities, claims handling, and policy administration

The ceding insurer removes the related assets and liabilities from its balance sheet on the effective date. The assuming insurer records those reserves on its own statutory financials.

Getting Approvals and Completing the Transfer

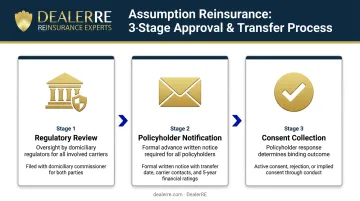

The transfer doesn't happen automatically. Under the NAIC Model Act structure, the process includes:

- Regulatory review — the assumption agreement must be filed with the domiciliary insurance commissioner for both parties

- Policyholder notification — each affected policyholder receives formal written notice via first-class mail, including the proposed transfer date, contact information for both carriers, and five years of financial ratings

- Consent collection — policyholders can actively consent, reject, or allow consent to be implied through conduct (such as remitting premiums to the new carrier)

Implied consent has a structured timeline under the Model Act: if no response is received after 24 months, a final notice is sent, and consent is deemed after one additional month of non-response.

That standard process does have one exception: when the ceding insurer is in hazardous financial condition, a state commissioner may authorize the transfer with implied consent to protect policyholders, bypassing the normal timeline entirely.

After the Transfer Is Complete

Once the novation takes effect:

- The assuming company becomes the insurer of record

- Policyholders interact directly with the new entity for claims and service

- The ceding insurer has no further obligations for the transferred policies

From a compliance standpoint, the transaction is considered final once all required notices are issued and the regulatory filings are acknowledged — meaning no party can unwind the transfer after that point without starting a new agreement.

Assumption Reinsurance vs. Traditional (Indemnity) Reinsurance

These two forms of reinsurance differ structurally — in legal mechanism, liability, and regulatory treatment. Here's a direct comparison:

| Dimension | Assumption Reinsurance | Indemnity Reinsurance |

|---|---|---|

| Policyholder liability | Reinsurer becomes directly liable | Original insurer remains liable |

| Ceding insurer obligation | Extinguished upon novation | Fully retained |

| Policyholder consent | Required (active or deemed) | Not required |

| Legal mechanism | Novation | Indemnification |

| Balance sheet impact | Liabilities removed from ceding insurer | Reinsurance credit recorded as asset |

| Regulatory filing | Required with commissioner | Standard reinsurance reporting |

The NAIC Model Act draws this line explicitly — it excludes from its scope any transaction where the ceding insurer "continues to remain directly liable" to policyholders. That covers the entire indemnity reinsurance category, which falls under separate regulatory frameworks.

The practical distinction matters for dealers evaluating program structures: traditional reinsurance manages ongoing risk and capital, while assumption reinsurance is a permanent exit mechanism — used when a party wants to fully transfer a set of obligations and remove them from its books entirely.

Key Benefits of Assumption Reinsurance

For the Ceding Insurer

The primary value is a clean break. By completing a novation:

- Future claims exposure is removed from the balance sheet entirely

- Capital ratios improve because reserves tied to transferred policies no longer apply

- Administrative burden for those policies shifts to the assuming company

This supports companies that want to exit legacy lines, simplify operations after a merger, or redirect capital toward growth areas.

For Policyholders

Coverage continues uninterrupted under the same policy terms. There's no gap in protection and no ambiguity about which company is responsible going forward: the consent process establishes that accountability before the transfer is finalized.

Real-World Scale

The transactions in this space can be substantial. Recent examples include:

- Wilton Re assumed $2.7 billion in long-term care statutory reserves from CNO Financial's Bankers Life subsidiary, allowing Bankers Life to exit its legacy LTC obligations entirely

- Global Atlantic completed an $8.0 billion annuity reinsurance transaction with Ameriprise Financial in 2021, transferring an entire block of annuity business between carriers

- RGA acquired John Hancock's US group life and disability business through the same mechanism

At this scale, the permanence of assumption reinsurance is the point — carriers and counterparties need certainty that the transfer is final, not a shared arrangement that could unravel.

Assumption Reinsurance and What It Means for Auto Dealer F&I Programs

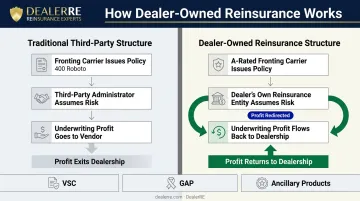

The Third-Party Problem

When a dealer sells a vehicle service contract, GAP product, or ancillary F&I coverage backed by a third-party provider, that provider is the one assuming the underwriting risk — and capturing the underwriting profit that comes with it. The dealer earns a flat commission. The administrator keeps the rest.

With F&I gross profit per vehicle retailed averaging $2,515 in Q2 2025 according to Haig Partners data, the dollars at stake are significant. The question is where those underwriting profits land — with the dealer or with a third party.

How Dealer-Owned Reinsurance Changes the Equation

In a dealer-owned reinsurance program, the structure flips:

- An A-rated fronting carrier issues the policy and maintains ultimate claim payment liability

- The dealer's own reinsurance company assumes the underwriting risk and earns the underwriting income

- When claims are lower than anticipated, profit accumulates in the dealer's entity, not a vendor's

- Programs cover VSCs, GAP, CPI, DCC, and ancillary products — tire and wheel, windshield repair, door ding, and more

DealerRE has been helping dealers establish and manage these programs since 1994, working with over 400 dealers nationwide. Thirty years in this space means the structural and compliance missteps that derail newer programs — mis-capitalized captives, failed state filings, reserve shortfalls — are problems DealerRE clients consistently avoid.

Frequently Asked Questions

What does "reinsurer assuming company" mean?

The assuming company is the reinsurer that accepts full transfer of risk and obligations from the ceding insurer. In assumption reinsurance, it becomes directly liable to policyholders for the policies covered by the agreement, replacing the original insurer as the party responsible for claims and coverage.

What is the difference between ceded and assumed?

"Ceded" refers to the original insurer's action of passing risk to a reinsurer; "assumed" refers to the reinsurer's acceptance of that risk. They describe two sides of the same transaction — the ceding company transfers, and the assuming company receives.

What is the difference between assumption reinsurance and indemnity reinsurance?

Assumption reinsurance results in a full transfer of obligations, with the reinsurer becoming directly liable to policyholders and the original insurer released. Indemnity reinsurance keeps the original insurer responsible to policyholders, with the reinsurer only reimbursing losses after the fact.

Does assumption reinsurance require policyholder consent?

In most U.S. states, yes. Because the transaction changes who is directly responsible for the policy, policyholders must be notified and given the opportunity to consent or reject. Consent can also be deemed through conduct, such as remitting premiums to the new insurer after receiving proper notice.

How is assumption reinsurance related to novation?

Assumption reinsurance is effectively a form of novation: a legal substitution of one contracting party for another. The original insurer is released and replaced by the assuming reinsurer as the new direct obligor — requiring agreement from all three parties: the original insurer, the assuming insurer, and the policyholder.

How does understanding assumption reinsurance help auto dealers?

Dealers who grasp this concept can see why dealer-owned reinsurance programs are profitable: instead of a third party assuming the underwriting risk on F&I products and keeping the profit, the dealer's own reinsurance company assumes that risk and captures those profits directly.