Switching warranty providers isn't just changing vendors. It involves active customer contracts, staff retraining, contractual exit terms, and potential revenue disruption if not managed correctly. One misstep during the transition can cost you penetration points, create compliance gaps, or leave customers in coverage limbo.

This guide walks through the specific signs it's time to switch, what to prepare before making any commitments, the step-by-step transition process, and what experienced dealers should consider beyond simply switching providers.

Key Takeaways

- Review your current contract's exit terms and run-off obligations before committing to any change

- Assess new providers on coverage depth, claims speed, profit structure, and training support — price is rarely the deciding factor

- Manage active customer contracts carefully to avoid coverage gaps during transition

- F&I staff retraining is non-negotiable and frequently underestimated

- For some dealers, switching providers doesn't solve the root issue; dealer-owned reinsurance may be worth exploring

Signs It's Time to Switch Warranty Providers at Your Dealership

Staying with the wrong provider costs you in two ways: direct profit loss and hidden damage from poor claims handling that erodes customer relationships. If you're seeing consistent underperformance, the financial impact compounds quickly.

Common triggers that signal it's time to evaluate alternatives:

- Low or inconsistent F&I income per deal — Public dealer groups averaged $2,612 F&I gross profit per vehicle retailed in Q4 2025, an all-time high. If your PVR is lagging this benchmark, your provider's product mix or pricing structure may be a contributing factor.

- High claim denial rates — When customers face repeated denials or slow adjudication, those complaints come back to your dealership, not the warranty company.

- Rigid coverage tiers with no customization options limit your ability to match products to customer needs or inventory profiles.

- Premiums or admin fees climbing while claims turnaround and support quality stay flat means you're paying more for the same — or worse — experience.

Contract structure can be just as telling as claims performance. Watch for:

- Rigid pricing with no volume incentives as your deal count grows

- Being treated as a low-priority account with slow or generic support

- Auto-renewal clauses that extend obligations without any performance review

Vehicle service contracts remain the highest-penetration F&I product at approximately 44% of deals, with products per deal averaging 1.56. A provider transition that disrupts VSC attachment even briefly has measurable PVR impact. That means your evaluation should be grounded in documented performance gaps — claim denial rates, PVR trends, support responsiveness — not just a competing quote.

What to Have in Place Before You Make the Switch

Dealers who skip the pre-switch audit often inherit the problems they were trying to leave behind. Rushed exits create compliance gaps, unresolved run-off claims, and staff who aren't ready to sell the new product.

Current Contract and Obligations Review

Pull your existing provider contract and review the following with your attorney or finance team:

- Termination notice requirements — Typically 30–90 days, though some contracts require longer notice periods

- Auto-renewal clauses — Many agreements automatically renew unless you provide notice by a specific deadline

- Exclusivity provisions — Some contracts restrict adding new products or working with competing providers during the term

Violating exit terms can result in financial penalties or unintended extended obligations. Document the exact termination date and required notice format before taking any further steps.

Run-off obligations define who remains responsible for honoring active customer service contracts after you switch providers. This is the most overlooked piece of the exit process.

Under the NAIC Service Contracts Model Act, the previous administrator's backing insurer remains obligated to honor all contracts issued prior to termination. Confirm in writing:

- Who handles run-off claims (the dealer, outgoing administrator, or backing insurer)

- How long the run-off period extends

- Whether any administrative fees apply to post-termination claims

Get this documented before you exit. If the outgoing administrator denies a run-off claim and you haven't secured a liability agreement, the repair cost may fall back on your dealership.

Data, Documentation, and Staff Readiness

Gather the following documentation before approaching new providers:

- Complete list of active customer contracts under the current provider

- Claims history for the past 12–24 months

- Product penetration rates by F&I manager

- Customer complaints tied to warranty coverage or claims experience

Brief your F&I managers on the pending change before selecting a new provider, not after. Their input on product gaps, customer objections, and claims friction shapes your evaluation criteria and builds alignment before the transition begins.

How to Switch Warranty Providers at Your Dealership

Step 1: Formally Audit Your Current Provider Relationship

Pull claims data, charge-back history, and customer complaint records for at least the prior 12 months to establish a performance baseline. This gives you objective comparison points when evaluating new providers.

Identify the contract termination clause and confirm the notice period required to exit without penalty. Document this date before taking any further steps.

Step 2: Define Your Requirements for the New Provider

Build a clear criteria list before approaching vendors:

- Minimum coverage tiers required for your inventory mix

- Expected claims turnaround time (top administrators typically offer same-day or next-business-day adjudication for straightforward mechanical claims)

- Profit structure — retail reserve, retrospective commission, or reinsurance participation

- Training support during onboarding and ongoing

- Multi-state compliance handling (confirm whether the provider manages state-by-state registration or if that falls to you)

Identify which F&I products your current provider is missing or weak on. This becomes your priority list for evaluating new candidates.

Step 3: Evaluate and Select a New Warranty Provider

Vet at least two to three providers side by side. Focus your evaluation on three factors:

Financial backing: Verify the administrator is backed by an A-rated insurer (A or A- rating by AM Best, which represents "excellent ability to meet ongoing insurance obligations"). This is standard for VSC administrators and protects both you and your customers.

Claims process: Ask how claims are adjudicated, typical turnaround times, and whether pre-authorization is required. Request claims data from reference dealers to validate performance claims.

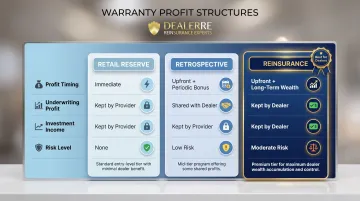

Profit participation: Compare structures carefully:

| Structure | Profit Timing | Underwriting Profit | Investment Income | Risk Level |

|---|---|---|---|---|

| Retail Reserve | Immediate at sale | Kept by provider | Kept by provider | None |

| Retrospective | Upfront + periodic bonus | Shared with dealer | Kept by provider | Low |

| Reinsurance | Upfront + long-term wealth | Kept by dealer | Kept by dealer | Moderate |

Request sample contracts and verify state-by-state compliance handling is included, not the dealer's sole responsibility.

Step 4: Negotiate the Transition Terms

Work with the new provider to set a go-live date that allows adequate training time, typically two to four weeks after contract signing. Before that date, nail down three things in writing:

- Go-live date with a confirmed staff training window

- Run-off claims responsibility: who adjudicates claims from the outgoing provider after the switch date

- Coverage overlap terms: no gaps or double-payment scenarios between the two contracts

Step 5: Retrain Staff and Update F&I Processes

Conduct formal F&I product training with the new provider before the first deal is written. Training should cover:

- Product features and coverage tiers

- Customer objection handling

- Compliance disclosures specific to the new contracts

- Claims submission process under the new system

Update F&I menus, deal jacket checklists, and customer-facing marketing materials to reflect the new provider. Confirm no old provider collateral remains in the finance office.

Plan for a 30-60-90 day onboarding ramp for F&I managers:

- Days 1–30: Product knowledge immersion and compliance training

- Days 31–60: Independent deal execution with manager coaching

- Days 61–90: Complex deal handling and self-assessment review

Most managers reach approximately 80% of store PVR targets by day 90.

Key Factors That Determine How Smooth the Transition Is

Two dealerships following the same steps can have very different transition experiences. The difference usually comes down to four variables — all within your control.

Exit terms documented before you initiate: The single biggest source of transition friction is ambiguity about termination terms. Dealers who clearly document exit rights and run-off responsibilities before initiating the switch avoid the most common delays and disputes.

What your new provider commits to in writing: A provider's willingness to invest in training, compliance setup, and early claims support during the first 60–90 days is a strong predictor of long-term performance. Ask upfront:

- What does your onboarding timeline look like?

- How many training sessions are included in the first 90 days?

- Who is our point of contact for claims issues during the transition?

- Do you provide performance reporting to track penetration rates post-launch?

When you bring your F&I team into the decision: Dealers who involve their F&I manager during the evaluation — not after the decision is made — see faster adoption and fewer early mistakes. Announcing a provider change without any input from the finance office creates resistance that slows everything down.

A script ready before the first customer calls: Existing customers with active service contracts need to understand their coverage continues uninterrupted. Prepare a short script before the transition window opens. Confirming coverage continuity and providing the new claims contact takes 30 seconds — and prevents the kind of confusion that damages customer trust.

Common Mistakes Dealers Make When Switching Warranty Providers

Three mistakes consistently derail otherwise well-planned transitions — and each one is avoidable.

Skipping a formal contract exit review: Many dealers begin evaluating new providers before confirming exit terms, then discover they're locked in for another year or owe early termination penalties. This step must come first, not midway through the process.

Failing to account for run-off claims: Switching providers without a documented plan for who handles outstanding customer claims under the old program is a costly oversight. If the outgoing administrator denies a run-off claim and you haven't secured a liability agreement, the repair cost may fall on your dealership.

Underinvesting in staff transition: Announcing a new warranty provider without structured training leaves F&I managers presenting products they don't fully understand. This directly hurts penetration rates and deal profitability in the first weeks post-switch. Plan for follow-up sessions and performance check-ins at 30, 60, and 90 days — not just an announcement meeting on day one.

Should You Just Switch Providers — or Build Your Own Reinsurance Program?

If switching providers still leaves you sending profits to a third-party administrator, have you actually solved the problem — or just changed who holds your money?

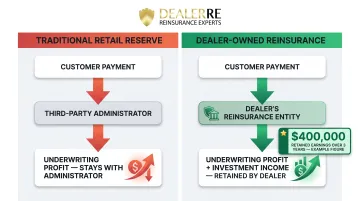

The fundamental limitation of working with any third-party warranty provider is this: the underwriting profits, investment income, and unearned premium reserve on all contracts written stay with the administrator, not the dealer. Switching providers may improve service or pricing, but it doesn't change that structure.

Dealer-owned reinsurance works differently. The dealer sets up their own reinsurance company (as an admin obligor), participating directly in the underwriting profits their own F&I volume generates. Claims are still managed through a licensed administrator and backed by A-rated insurers, but the profit flow changes entirely.

Here's how the two models compare:

- Traditional retail reserve: The dealer earns a flat commission; the administrator retains underwriting profit and investment income

- Dealer-owned reinsurance: The dealer creates a separate insurance entity that assumes the risk and retains both profit streams

In practice, when a customer purchases a vehicle service contract, premiums go to the dealer's reinsurance company instead of a third-party provider. The dealer captures the underwriting profits once claims are paid and contracts expire.

Reinsurance becomes practical at approximately 20–25 vehicle service contracts per month. A mid-size dealer selling 25 VSCs monthly at $1,200 premium ($360,000 annual premium) could accumulate approximately $400,000 in retained earnings over three years.

This isn't a fit for every dealership. Volume, F&I product mix, and long-term business goals all factor into whether a dealer-owned reinsurance program makes sense. DealerRE has helped more than 400 dealers across the country evaluate and establish these programs, and offers a business analysis to determine if the structure is the right fit before making any commitment.

Frequently Asked Questions

Do vehicle service contracts I sell restrict customers to my service department?

Most vehicle service contracts allow customers to use any licensed repair facility, not just the selling dealership. Coverage network terms vary by administrator, so confirm repair facility access when evaluating which products to offer.

How much does it cost to transfer an extended warranty?

Transfer fees for customer-facing extended warranties typically range from $50 to $100 and are governed by the administrator's contract terms. This is separate from the dealer's cost to switch providers at the business level.

Can my dealership exit a warranty provider agreement early?

Your ability to exit depends entirely on the contract's termination clause. Most agreements include notice periods, auto-renewal provisions, and early exit penalties — review these terms carefully before signing with any administrator.

What happens to in-force contracts when I switch warranty providers?

In-force contracts remain the obligation of the original administrator until they expire — your new provider does not inherit them. During the transition, you'll typically run two administrators in parallel until existing contracts close out naturally.

How do vehicle service contracts work?

A vehicle service contract (VSC) is a separate agreement — not a manufacturer's warranty — in which an administrator agrees to cover specified mechanical repairs for a set term or mileage. Claims require pre-authorization from the administrator before repairs begin — confirm this process with any provider before signing.