Introduction

Many auto dealers hand over a significant portion of their F&I product profits to third-party warranty providers without realizing an alternative exists: owning and operating their own reinsurance company to capture those underwriting profits in-house. Publicly traded dealership groups averaged $2,577 in F&I gross profit per vehicle retailed in Q4 2025, making F&I one of the most valuable profit centers in retail automotive. Yet under traditional third-party arrangements, 100% of collected premium flows to the administrator or carrier, with dealers receiving only a modest commission.

This guide is written for franchise, independent, and BHPH dealers considering a move away from third-party providers.

The migration process is often misunderstood at a practical level. Many dealers assume it's prohibitively complex, too expensive, or reserved for large groups only. The process is structured, repeatable, and accessible to dealers of varying sizes when executed with the right partner.

Key Takeaways

- A dealer-owned reinsurance company captures underwriting profits and investment income third-party providers currently keep

- Setup requires auditing contracts, forming the legal entity, establishing trust accounts, and transitioning premium ceding

- Volume, claims discipline, the right administrator, and a solid investment strategy determine whether the program succeeds

- Exiting third-party contracts without planning for claims run-off is the most common — and costly — migration mistake

What Does Migrating to In-House Reinsurance Actually Mean?

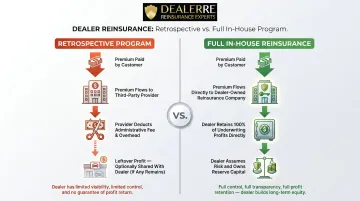

Migration in this context refers to the process of moving from a structure where a third-party provider holds and retains underwriting profits from your F&I products—vehicle service contracts, GAP, ancillary coverage—to a dealer-owned admin obligor reinsurance structure where those profits flow into your own reinsurance company.

This is fundamentally different from simpler profit-sharing arrangements like retrospective programs ("retros"). In a retro program, the dealer receives a share of leftover profits after the provider takes their cut. In full migration, the dealer assumes underwriting risk and ownership of reserves. Instead of waiting on a third party to decide whether to share profits, you capture them directly as they're earned.

Admin Obligor Structure

A Dealer-Owned Warranty Company (DOWC) is a specialized corporate structure where the dealer establishes a U.S. domestic C-corporation or offshore entity to act as the service contract provider (obligor) for their F&I products.

Under this structure, the dealer's reinsurance company is the named obligor — it bears initial performance risk and shifts uninsured performance risks to an affiliated captive through risk transfer agreements.

Eligible F&I Products for Ceding

Most standard F&I product categories can be ceded into a dealer-owned reinsurance program:

- Vehicle service contracts (VSCs)

- Guaranteed Asset Protection (GAP)

- Tire and wheel protection

- Dent and appearance coverage

- Theft protection

- Windshield repair

- Collateral Protection Insurance (CPI)

- Debt Cancellation Coverage (DCC)

Specific eligibility depends on program structure and your fronting insurer's guidelines — but these eight categories cover the large majority of what dealers migrate.

Why Dealers Switch from Third-Party to In-House Reinsurance

The Core Profit Gap

Under a standard walkaway program, 100% of the collected premium flows to the administrator or insurance carrier. The administrator takes a fee, the underwriter holds reserves, and if claims are low, the carrier keeps the profit. Dealers receive only a commission—typically a fraction of the total underwriting profit generated.

Research shows that dealers leveraging a DOWC structure see an average 20% lift in F&I profits. This lift comes not from selling more products, but from retaining underwriting profits that previously left the dealership entirely.

Financial Upside of In-House Reinsurance

When you own your reinsurance company, you capture three distinct financial advantages:

- Underwriting profit retention: Blended loss ratios for well-structured programs typically run 35-40%, meaning 60-65% of premiums become potential retained profit. On $500,000 in annual premiums at a 40% loss ratio, $300,000 stays in your reinsurance company instead of going to a third-party carrier.

- Investment income on reserves: Premiums arrive upfront while claims pay out over time. That gap creates a reserve pool earning investment income. Unearned Premium Reserves (UPR) require conservative investment initially, but once surplus accumulates, dealers can deploy it into equities, real estate, or other assets.

- Tax-deferred asset accumulation: Unlike commission income that's taxed immediately, reinsurance profits accumulate inside a captive structure. Reserves grow tax-deferred under Internal Revenue Code Section 831(b) for programs writing less than $2,200,000 in annual net premiums, allowing wealth to compound over time.

Operational Control

When you own your reinsurance company, you control how claims are adjudicated, can tailor F&I products to your customer base, and protect customer relationships by ensuring claims outcomes reflect well on your store. Directing claims back to your own service facility not only improves customer satisfaction but also keeps service revenue in-house.

Once surplus builds in your "B" account, those funds can be invested across a broader range of assets—real estate, equities, or other ventures—making in-house reinsurance a reliable long-term wealth-building strategy compared to taking taxable dealership distributions.

How the Migration Process Works, Step by Step

Migration is not a single action but a structured transition involving contract review, entity formation, trust setup, product onboarding, and staff alignment—typically executed over a defined period with the help of an experienced reinsurance administrator like DealerRE.

Step 1: Audit Your Existing Third-Party Agreements

The first step is a full review of current third-party warranty and F&I product contracts. This audit examines:

- Cancellation provisions and notice periods

- Penalties for early exit

- What happens to in-force policies and future claims (run-off liability)

- Obligations to customers on contracts sold under the old program

Dealers cannot simply walk away from existing obligations mid-term. All previously sold in-force customer contracts remain obligations of the original provider/obligor. New contracts written after the transition date flow into the new reinsurance entity.

Step 2: Select Your Reinsurance Structure and Domicile

Dealers must choose their reinsurance structure—most commonly admin obligor—and select a domicile for their reinsurance company.

Common domicile options:

Turks and Caicos Islands (TCI): TCI is a primary offshore domicile choice due to lighter-touch regulation and lower capitalization requirements. Formation costs are approximately $5,000 initial/$3,500 annual, with a 6-8 week timeline. All assets can remain in the United States even when the company is domiciled offshore.

Delaware Tribe (Tribal Domicile): Established in 2012-2013 as the first viable, economically-feasible domestic alternative to traditional offshore domiciles. Formation costs are $2,750 initial/$3,500 annual, with a 3-5 business day timeline. Eliminates the need for an IRS Section 953(d) election required for offshore entities.

The right choice depends on regulatory requirements, tax treatment, and the dealer's specific goals. Worth noting for dealers currently in offshore CFC/NCFC structures: the Tax Cuts and Jobs Act of 2018 pushed many to shift toward domestic DOWCs due to new disclosure and reporting requirements.

Step 3: Form the Legal Entity and Establish Trust Accounts

This step involves attorneys, CPAs, and a reinsurance administrator working together to:

- Form the legal entity (corporation or offshore captive)

- Establish reserve trust accounts with a U.S. Trust Company

- Set up the "A" account (Unearned Premium Reserves) subject to conservative investment restrictions

- Set up the "B" account (surplus/earned funds) with broader investment flexibility

- Ensure compliance with state licensing requirements and IRS Code 831(b)

DealerRE coordinates licensing, tax preparation, and all legal filings to ensure compliance. The structure requires a three-party trust agreement between the bank, the reinsurance company, and the fronting insurer. 100% of ceded funds are held in a U.S. Trust Company — no funds move offshore, even when the reinsurance company is domiciled there.

Step 4: Onboard Your Team and Align F&I Operations

Migration requires active staff preparation. F&I managers need to understand:

- Which products will now be ceded to the dealer's own company

- How remittance works and when premiums are submitted

- How claims will be processed differently

- The importance of product presentation quality on program profitability

DealerRE provides structured onboarding, F&I training programs (online and in-person), and F&I menus to support this transition. The quality of F&I training and product selection at this stage directly affects the profitability of the new program.

Step 5: Begin Premium Ceding and Monitor Program Performance

The operational start of the program involves:

- Remitting premiums from eligible products sold into the reinsurance trust

- Paying claims from UPR reserves

- Receiving regular performance reports from the administrator

The program requires active management, not a passive set-and-forget approach. That means monitoring loss ratios, investment returns, and claims trends on an ongoing basis. DealerRE provides monthly financial statements covering claims losses, underwriting profits, and overall program performance — giving dealers the visibility to make informed decisions as the program matures.

Key Factors That Determine a Successful Migration

F&I Sales Volume

There is a practical minimum volume threshold below which the economics of establishing and maintaining a dealer-owned reinsurance company may not justify the administrative cost and complexity.

Industry benchmarks:

- Elite FI Partners recommends 20-25+ F&I contracts per month

- Automotive Assurance Group suggests 25 VSCs or 50 GAP contracts per month

- Dealer Developments recommends 30 VSC sales per month

That said, DealerRE emphasizes that the belief that reinsurance requires very high volume is one of the biggest misconceptions in the industry. Smaller dealerships can benefit when the program is structured correctly and administered efficiently.

Choice of Reinsurance Administrator

The administrator manages claims adjudication, compliance filings, tax returns, legal forms, renewals, and performance reporting. This is the most critical partnership decision in the migration. A poorly chosen or misaligned administrator erodes the profitability the dealer is trying to capture.

see stronger long-term program performance.

Monthly loss monitoring and contract earn-out projections give dealers the visibility they need to stay ahead of claims trends rather than reacting after the fact.

Investment Strategy for Reserves

UPR funds must be invested within regulatory and insurer guidelines — typically conservative government bonds earning short-term rates. This keeps reserve capital protected while the underlying contracts earn out.

Once balance sheet cash exceeds 125% of UPR, surplus B-account funds can be invested more broadly in equities and other securities. Ask your administrator specifically how they approach surplus investment strategy — the difference between actively managed surplus funds and cash sitting idle can be substantial over a 5-10 year program horizon.

Common Mistakes and Misconceptions During Migration

Exiting Third-Party Contracts Without Managing Run-Off

One of the most common errors is terminating third-party agreements without a clear plan for handling claims on in-force policies. Dealers may still owe obligations to customers on contracts sold under the old program. Ignoring this creates financial and reputational exposure.

The transition is often scheduled at a contract-year boundary so existing contracts can run off under the old structure while new contracts are written under the new structure. Traditional VSC contract terms range from 60 to 120 months (5 to 10 years), meaning a book of business can take years to fully run off.

Assuming Migration is a One-Time Setup, Not an Ongoing Commitment

Many dealers underestimate the operational involvement required post-launch. Active management includes:

- Reviewing claims trends monthly

- Managing investment accounts strategically

- Ensuring timely remittance timing (weekly rather than monthly maximizes reserve growth)

- Conducting periodic program performance reviews

DealerRE provides ongoing support — from claims review to performance analysis — so dealers stay engaged and keep their programs running at full potential.

Misconception That Reinsurance is Only for Large Dealership Groups

The assumption that smaller or single-point stores cannot benefit from in-house reinsurance prevents many qualifying dealers from exploring it. While volume does matter, the economics have become more accessible as administrator support has improved. DealerRE has helped single-point stores and smaller independents establish profitable programs — dealers selling as few as 30 units per month can qualify. Size matters less than structure and consistency.

Conclusion

Migrating from a third-party warranty program to in-house reinsurance is a strategic decision that requires deliberate planning: auditing existing agreements, forming the right entity, onboarding staff, and selecting the right administrator. Dealers who complete that process gain direct control over underwriting profits they were previously paying to third-party providers.

Execution and the quality of the partnership behind it determine whether a program succeeds long-term. DealerRE has helped over 400 auto dealers establish and manage their own reinsurance companies — handling dealership analysis, compliance management, staff training, and full-service administration. Dealers considering the switch should work with an experienced reinsurance partner to assess readiness and build a program designed around their specific operation.

Frequently Asked Questions

What is warranty reinsurance?

Warranty reinsurance (in the dealer context) is a financial structure where a dealer forms their own captive reinsurance company to assume the underwriting risk of F&I products like vehicle service contracts and GAP insurance, allowing them to capture the profits from premiums exceeding claims rather than having those profits retained by a third-party provider.

Can you cancel a 3rd party warranty?

Third-party warranty agreements can often be exited, but the terms and timing vary by contract. Dealers should review cancellation provisions carefully, as in-force customer obligations and run-off claims may still need to be honored even after the provider relationship ends.

How do you convert from a third-party insurance arrangement to full in-house reinsurance?

The conversion path involves auditing existing contracts, forming the dealer-owned reinsurance entity, establishing trust accounts, transitioning eligible product ceding to the new company, and aligning F&I staff. Most dealers complete this process in partnership with an experienced reinsurance administrator like DealerRE.

How long does the migration from third-party to in-house reinsurance typically take?

The timeline varies, but entity formation, trust setup, and compliance work typically take several weeks to a few months. Dealers realize the full financial benefit over time as premiums accumulate and the loss ratio matures — most programs hit their stride in the second or third year.

What F&I products can be ceded to a dealer-owned reinsurance company?

Eligible products commonly ceded include vehicle service contracts (VSCs/extended warranties), GAP insurance, tire and wheel protection, dent and appearance coverage, and certain ancillary F&I products. Eligibility depends on the program structure and the fronting insurer's guidelines.