Introduction

When a customer walks into Location A to report a warranty issue on a vehicle they purchased at Location B, the coordination required exposes every weakness in a dealer group's service and claims infrastructure. This scenario plays out hundreds of times per day across multi-location dealer groups nationwide, and the financial consequences are real.

According to WarrCloud, the cost of processing auto warranty claims has increased by 28% since 2020, while processing time has jumped 47%. At scale, each breakdown in documentation, pre-authorization, or reimbursement tracking translates directly into profit leakage, audit risk, and customer dissatisfaction.

This guide covers both OEM/factory warranty claims and dealer-sold vehicle service contract (VSC) claims — two reimbursement streams with separate processes, administrators, and documentation standards. It's written for multi-location franchise, independent, and BHPH dealer group operators.

Here's what this guide covers:

- How the claims process works across multi-location dealer groups

- The specific operational challenges that arise at scale

- How top-performing groups standardize their workflows

- Why controlling warranty products through admin obligor reinsurance creates a structural advantage over outsourcing to third-party administrators

TL;DR

- Multi-location warranty management runs on two separate tracks: OEM reimbursements and dealer-sold VSC claims, each with distinct documentation requirements and administrators

- Consistent claim routing across OEM warranty departments, third-party providers, and dealer-owned reinsurance companies is the make-or-break operational challenge

- Without centralized oversight, dealer groups bleed money through denied claims, documentation errors, and profits lost to third-party administrators

- Top-performing groups use standardized workflows, shared DMS platforms, trained service advisors, and defined escalation protocols

- Dealer groups that control their own warranty products through admin obligor reinsurance set the rules, adjudicate claims on their timeline, retain underwriting profits, and eliminate third-party dependency

What Are Service & Warranty Claims at Multi-Location Dealerships?

A warranty claim is a formal request for reimbursement or coverage fulfillment when a vehicle component fails under a covered warranty agreement. The claim requires documentation of the repair performed, parts used, labor time, and authorization before payment is issued. Without proper documentation and approval, claims are denied—and in multi-location environments, denied claims quickly become a pattern that triggers costly audits.

Two distinct claim types operate simultaneously at most multi-location groups:

OEM/factory warranty claims - The manufacturer reimburses the franchise dealer for covered repairs performed under the factory warranty. These claims follow OEM-specific submission formats, labor time guides, and approval processes.

Dealer-sold VSC claims - A third-party administrator or the dealer's own reinsurance company pays for covered repairs under extended service contracts sold at the point of sale. These claims require pre-authorization from the administrator and follow contract-specific coverage terms.

These two streams use separate approval channels, reimbursement schedules, and documentation requirements. At single-location dealerships, managing this complexity is difficult. At multi-location groups, every claim creates coordination questions that rarely have obvious answers across locations:

- Which location owns the customer relationship?

- Who holds authority to approve the repair?

- Which system serves as the record of truth?

- Who ensures the claim is submitted correctly and paid on time?

Why Managing Claims Across Multiple Locations Is Uniquely Complex

The Jurisdiction Problem

When a vehicle sold at Location A arrives for service at Location B, the selling location may hold the service contract but lack visibility into the repair. Without a clear protocol, the service-performing location may not know the vehicle has coverage, who to contact for pre-authorization, or which administrator handles the claim. This breakdown leads to unauthorized repairs, denied claims, and frustrated customers who expect seamless service across all locations.

The Documentation Consistency Challenge

Warranty claims—especially OEM claims—can be denied or charged back for incomplete documentation. When different locations have different service advisors, different DMS configurations, and different training levels, claim quality becomes inconsistent across the group.

One location may submit claims with proper technician certification codes, labor time justifications, and "3 C's" documentation (complaint, cause, correction), while another submits bare-bones work orders that trigger immediate denials.

When Pre-Authorization Falls Through the Cracks

Many VSC claims require pre-authorization before a repair begins. Major administrators explicitly mandate this:

- Zurich requires repair facilities to verify coverage and obtain a repair authorization number before any repair is made

- Assurant mandates customers obtain authorization prior to beginning covered repairs, and the administrator must authorize all repairs in advance

- Allstate explicitly states that repairs completed prior to authorization may not be covered

Service advisors at the performing location may call the wrong administrator, use the wrong claim form, or stall on authorization because they're unfamiliar with coverage terms on a vehicle they didn't originally sell. Missed or incomplete pre-authorization is one of the most common reasons claims are denied.

The Financial Tracking Problem

Warranty work accounts for 25% of a dealer's service volume, and approved OEM parts and labor warranty claims contribute 15% or more to a dealership's gross profits. Yet nearly 60% of U.S. dealerships report an increase in warranty claims, while the cost of processing each claim has increased by 28% and processing time has risen by 47% since 2020.

That's a growing share of revenue tied to claims processing — and groups without centralized reimbursement tracking often have no one accountable for following up. Claims sit unpaid for weeks or months, and revenue that should reach the service department gets written off as uncollectible instead.

The Audit Exposure That Compounds Across Stores

OEMs conduct periodic warranty audits triggered by volume anomalies, repeat failures, or missing documentation. Multi-location groups face elevated risk when standards vary by store — a chargeback issued at one location can reveal systemic documentation problems group-wide.

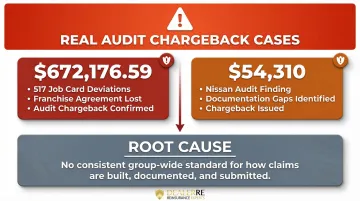

Two recent cases illustrate what's at stake:

- A GM dealer received a $672,176.59 chargeback for 517 job card deviations, ultimately losing the franchise agreement due to false claim submissions

- An Ohio dealership fought a $54,310 chargeback following a Nissan warranty audit over documentation gaps

Both outcomes trace back to the same root cause: no consistent standard across the group for how claims are built, documented, and submitted.

How Multi-Location Dealerships Handle Service & Warranty Claims

The most effective multi-location dealer groups treat warranty claims management as a fixed operational system, not a location-level discretionary process. They define exactly who is responsible at each step, across every store, with clear escalation paths and centralized oversight.

Step 1: Customer Check-In and Coverage Verification

The process begins when a customer arrives at any location. The service advisor must identify whether the vehicle has factory warranty, a dealer-sold VSC, or no coverage. In a multi-location group, this requires the DMS to surface coverage information regardless of which location sold the vehicle.

Best-in-class dealer groups run unified DMS platforms across all locations, allowing instant access to service history, active warranties, and contract administrators. When DMS systems are fragmented, 39.8% of dealership professionals lose 5-10 hours per week to inefficiencies, and 30.4% report that disconnected CRM and DMS systems slow transaction speed.

During check-in, the advisor confirms:

- Factory warranty status and remaining coverage period

- Active VSC contract and administrator contact information

- Authorization requirements before diagnostic work begins

- Which repair facility is authorized to perform the work

Step 2: Diagnosis, Documentation, and Pre-Authorization

Once a covered repair is identified, the advisor must document the complaint, cause, and correction (the "3 C's") in the required format. From there, they contact the appropriate warranty administrator — either the OEM warranty department or the VSC administrator — to obtain pre-authorization before performing the repair.

This is where claims break down most frequently. VSC contracts explicitly list "repairs performed without the Administrator's prior authorization" under non-covered conditions. The California Department of Insurance warns consumers that if they proceed without prior authorization, the obligor or claim administrator may try to deny the claim.

Top-performing dealer groups establish clear pre-authorization protocols:

- Service advisors know which administrators handle which contracts

- Each location has access to administrator contact information and claim submission portals

- Advisors document authorization numbers in the DMS before work begins

- Diagnostic tear-down is authorized separately from repair work

For OEM claims, documentation must meet manufacturer-specific standards, including labor time justifications, technician certification codes, and narrative descriptions of the failure. Missing or incomplete documentation triggers automatic denials.

Step 3: Repair, Claim Submission, and Reimbursement Tracking

After the repair is completed, the service team submits the warranty claim with all required documentation: labor times, parts invoices, authorization numbers, and technician certification codes.

In a multi-location group, there should be a group-level claims reviewer or warranty administrator who audits submissions before they leave the store and tracks reimbursement status across all locations.

This is where dealer-owned service contract programs create a structural advantage. Instead of submitting to a third-party administrator and waiting for approval, dealer groups that control their own admin obligor reinsurance company set their own claim guidelines, approve repairs faster, and retain profit that would otherwise go to an outside company.

Through DealerRE's admin obligor reinsurance structure, dealer groups function as the administrator—adjudicating claims internally, controlling timelines, and capturing underwriting profits. Repairs can be directed back to the dealer's own service facilities, keeping service contract revenue within the business ecosystem rather than losing it to third-party administrators. For multi-location groups, this eliminates the fundamental tension between standardizing claims handling and capturing profit—both goals are achieved through the same structure.

Key Factors That Affect Claims Management Across Locations

Five operational variables separate dealer groups that run tight claims operations from those losing revenue to administrative failures:

DMS integration across locations: Whether all stores run on the same DMS platform affects how quickly coverage can be verified and how accurately claims are tracked group-wide. Large dealer groups like Group 1 Automotive have consolidated from three DMS providers to a single platform, projecting annual IT cost reductions of at least $3 million while standardizing backroom processes.

Staff training consistency: One undertrained advisor can generate a pattern of denied claims that triggers an OEM audit for the entire group. High-performing dealer groups standardize training across all locations so every advisor understands documentation requirements, pre-authorization protocols, and claim submission standards.

Manufacturer or administrator relationships: Franchise dealers with strong OEM relationships tend to get faster approvals and more favorable labor time rulings, while independent dealers using third-party VSC administrators have less leverage. Dealer-owned admin obligor reinsurance programs eliminate this dependency entirely: the dealer sets the claim standards and approves repairs without external negotiation.

Volume and throughput: Higher-volume service departments face greater claims complexity, and multi-location groups must scale accordingly — often requiring dedicated warranty clerks or centralized claims reviewers. What works at a 10-car-per-day shop breaks down fast at 40 cars per day across multiple bays.

Regulatory and compliance constraints: Forty-nine states now have legislation requiring manufacturers to reimburse dealers at retail rates for warranty service. Illinois mandates a 1.5x multiplier on the OEM time guide, New Jersey's 2026 law introduces a multiplier based on average retail labor-time allowances, and states like New York allow dealers to use third-party labor time guides. Dealer groups operating across multiple states must ensure compliance in each jurisdiction and actively elect statutory submission methods to force OEMs to pay true retail rates.

Common Issues and Misconceptions in Multi-Location Claims Handling

Misconception: Warranty Claims Management Has No Profit Upside

Most dealers don't realize that OEM labor rate reimbursements are negotiable in many states, that denied claims can be successfully appealed with proper documentation, and that the VSC claims process is a direct profit opportunity. Armatus Dealer Uplift reports an average per-hour warranty labor increase of $21.16 for its clients — translating to an average annual warranty labor gross profit increase of $77,892.

For dealer-sold VSC claims, the profit opportunity is even larger. When dealers own their own admin obligor reinsurance company, they capture 100% of underwriting profits that third-party administrators were previously keeping. They also earn investment income on premium reserves held in trust.

The "Location Island" Problem

Dealer groups that let each location manage claims independently without group-level standards end up with wildly different denial rates, reimbursement timelines, and customer satisfaction scores—and no way to identify or fix the root cause. Without centralized tracking and oversight, high-performing locations subsidize underperforming ones, and systemic issues remain invisible until an audit reveals the damage.

Under-Investing in Warranty Administration Headcount

Many multi-location groups assume service advisors can handle claims as a side task. In reality, warranty claim errors are a primary driver of revenue leakage and audit vulnerability. Top-performing groups employ dedicated warranty clerks or group-level warranty administrators who audit submissions, track reimbursements, and ensure documentation standards are met before claims leave the store.

Misconception: Dealer-Sold VSC Claims Are Always Faster

When VSCs are sold through third-party administrators, dealers are at the mercy of that administrator's claim approval timelines, coverage interpretations, and dispute processes. The automotive third-party administrator industry averages 3 to 6 days for claim cycle times, while top performers achieve 1 to 2 days. However, Better Business Bureau data shows thousands of complaints against major TPAs for severe delays and claim denials—Endurance Warranty Services has 3,629 total complaints in the last three years, while CarShield has 2,642.

When customers file VSC claims, they often blame the selling dealership when administrators deny coverage or delay approvals. This damages the dealer's reputation for circumstances outside their control.

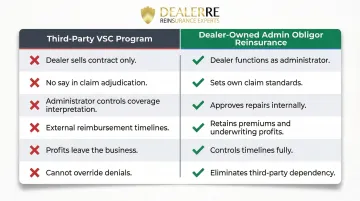

The Difference Between Third-Party VSC Programs and Dealer-Owned Admin Obligor Reinsurance

The two structures deliver very different outcomes for multi-location groups:

- Third-party VSC program: The dealer sells the contract but has no say in claim adjudication, coverage interpretation, or reimbursement timelines. The third-party administrator makes all decisions — dealers cannot override denials or expedite approvals.

- Dealer-owned admin obligor reinsurance: The dealer group functions as the administrator, setting claim standards, approving repairs, and retaining the premiums and profits that would otherwise leave the business.

For dealer groups trying to standardize claims handling while recapturing profit, the dealer-owned structure removes the core conflict. DealerRE helps dealer groups build and manage this structure, covering administration, claims adjudication, compliance management, and performance reporting across all locations.

Frequently Asked Questions

Can I take my car to a different dealership for warranty service?

For factory/OEM warranties, most manufacturers allow customers to take their vehicle to any authorized franchise dealer for covered repairs—the repair location bills the manufacturer directly. For dealer-sold VSCs, coverage typically follows the contract terms, which may allow any licensed repair facility or may require administrator authorization. Customers should check their contract or call the administrator before scheduling service.

What is the KPI for warranty claims?

The four primary KPIs are:

- Claim approval rate — percentage of submitted claims approved on first submission (industry average: 75%–85%; top performers: 88%–93%)

- Claim cycle time — days from repair completion to reimbursement

- Labor rate recovery — actual reimbursement vs. effective retail rate

- Chargeback rate — percentage of approved claims later reversed during audits

Best-in-class dealer groups track all four metrics by location to identify underperforming stores.

What are 5 common acts that void your vehicle's warranty?

Warranty coverage is typically voided by:

- Unauthorized modifications to the vehicle

- Neglected maintenance (missed oil changes documented by service records)

- Use of improper fluids or parts

- Racing or off-road use beyond vehicle specifications

- Odometer tampering

For dealer-sold VSCs, exclusions vary by contract — customers should review their specific terms with the administrator.

How do multi-location dealer groups coordinate warranty claims across stores?

The most effective groups use a shared DMS, standardized documentation procedures, a central warranty administrator or group-level warranty manager, and defined escalation protocols. This ensures customers can receive warranty service at any location — regardless of where they purchased their vehicle — without the claims process breaking down.

What is the difference between a factory warranty and a dealer-sold service contract?

A factory warranty is issued by the vehicle manufacturer and covers defects in materials or workmanship for a defined period, with claims reimbursed directly to the repair dealer by the OEM. A dealer-sold VSC is a separate product sold at the time of purchase, administered by a third party or—in dealer-owned programs—by the dealer's own reinsurance company, covering mechanical breakdowns beyond the factory warranty period. The two operate through entirely different claim submission, approval, and reimbursement processes.