Introduction

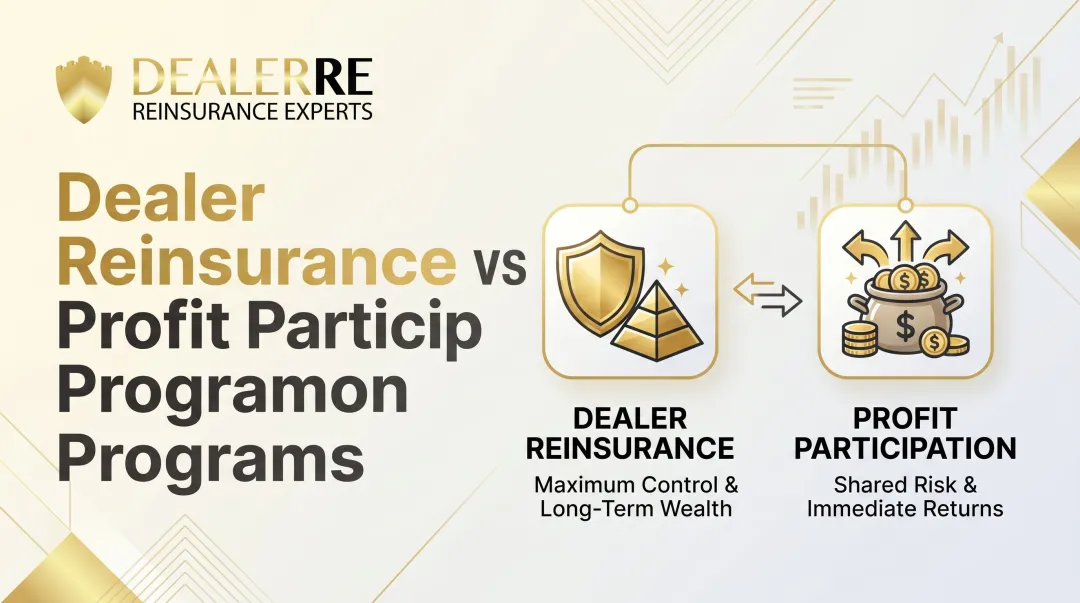

Most auto dealers generate strong F&I revenue but unknowingly surrender the most profitable layer — underwriting profit — to third-party product providers. Publicly traded auto retail groups generated an average of $2,534 in F&I gross profit per vehicle in Q3 2025, a 5.2% increase year-over-year. Yet in the standard dealer-agent model, the administrator retains 100% of the underwriting profit and investment income while the dealer earns only a flat commission. Profit participation programs give dealers a path to recapture that income, but which structure they choose determines how much they actually keep.

The choice between profit participation structures has real long-term consequences for net profit, tax strategy, and business equity. A retro bonus delivers a year-end check. An admin obligor reinsurance company builds a separately valued asset that grows with every contract written. This guide breaks down each structure — retro bonuses, CORPs, and admin obligor reinsurance — so dealers can make an informed decision about where their F&I income actually ends up.

Key Takeaways

- Profit participation programs let dealers capture underwriting profits from F&I products rather than leaving that income with third-party providers

- Retro programs, DORCs, and admin obligor programs each differ significantly in how much profit and control dealers actually retain

- The right program depends on F&I volume, capital position, risk tolerance, and tax planning goals

- Admin obligor programs provide maximum profit ownership, A-rated carrier backing, and wealth-building potential

- Working with an experienced reinsurance administrator helps dealers select, set up, and manage the structure that fits their dealership

What Are Profit Participation Programs for Auto Dealers?

Profit participation programs allow auto dealers to share in the underwriting profit generated by F&I products — the income that remains after claims are paid — rather than earning only a dealer markup or reserve commission on product sales. These arrangements became common in the 1970s, and today the vast majority of dealers participate in some form.

In a standard dealer-agent arrangement, the third-party provider retains underwriting profit when claims come in below premium levels. The dealer earns a fixed reserve but never sees the remaining spread. That residual income, compounded by investment returns on premium reserves, flows entirely to the administrator.

Types of Profit Participation Programs

Retro Programs (Retrospective Commission Arrangements):

The third party administers and controls the program; the dealer receives a bonus refund at period-end if the portfolio's loss ratio is favorable. Retro programs require $0 upfront costs and $0 ongoing expenses, with annual commission checks beginning after two full calendar years of writing contracts. If the overall portfolio goes negative, the dealer is not responsible for losses.

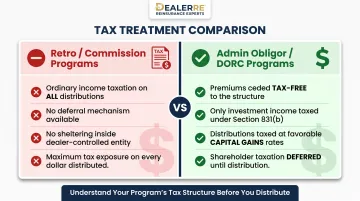

The tradeoffs are real, though. Profit is capped, timing is at the provider's discretion, distributions are taxed as ordinary income, and the dealer has no ownership of accumulated reserves.

Dealer-Owned Reinsurance Companies (DORC):

The dealer establishes a separate reinsurance entity — often domiciled in the Cayman Islands, Bermuda, or domestically in captive-friendly states — that assumes a share of underwriting risk from the third-party administrator.

These structures commonly use the Section 831(b) election, capping annual premiums at $2.8–$2.85 million and taxing only investment income. The dealer captures residual underwriting profit and builds a reserve asset in the owned entity, with distributions typically receiving capital gains treatment.

Admin Obligor Programs:

The dealer's own company is named as the obligor on F&I product contracts, backed by an A-rated carrier. This structure captures the maximum share of underwriting profit, provides the highest level of dealer ownership and control, and creates a distinct business asset with investment potential. DealerRE's admin obligor programs are insured by A-rated carriers, combining dealer ownership economics with institutional-grade risk backing.

Why the Structure Choice Matters

The financial difference between a retro arrangement and an admin obligor structure compounds significantly over time. Consider two scenarios:

- Mid-size dealer (150 units/month, 65% penetration, $800 avg. premium): accumulates well over $3 million in reinsurance reserves over five years, including investment returns — money that stays with the carrier without reinsurance ownership

- Smaller dealer (25 VSCs/month, ~$1,200 avg. premium): builds close to $400,000 in equity over three years at approximately 5% average return on reserves

Benefits extend beyond immediate profit:

- Investment control — accumulated premium reserves can be deployed into bonds, index funds, or other securities

- Claims authority — direct oversight of claims adjudication improves customer experience and reduces loss ratios

- Asset creation — a separately valued business entity usable for tax planning, wealth transfer, or succession funding

Key Factors to Consider When Choosing a Profit Participation Program

No single structure is right for every dealership. The decision must reflect a dealer's specific financial profile, operational scale, and long-term business goals — not just which program sounds most profitable on paper.

F&I Volume and Product Mix

Monthly unit volume and the range of F&I products offered are the foundational filter. Higher-ownership programs require sufficient premium flow to fund loss reserves and make administrative overhead worthwhile. Industry sources converge around 20-30 VSC contracts per month as the entry point — many dealers unnecessarily wait until reaching 50 or 100+ contracts, which represents a costly delay.

General industry guidance on volume thresholds:

- Retro programs: No minimum; viable at any scale

- DORC/CFC programs: 20-25 VSCs per month minimum

- Admin obligor programs: 25-30 contracts monthly or 300-350 annually

GAP and ancillary products require case-by-case evaluation. Ancillary products like tire and wheel, key replacement, and appearance protection carry extremely low loss ratios compared to standard VSCs, making them attractive candidates for reinsurance even at lower volumes.

Capital and Reserve Requirements

Admin obligor and reinsurance programs require the dealer to capitalize an owned entity and maintain adequate loss reserves, whereas retro programs require no upfront capital commitment. DORC startup costs run approximately $3,500-$5,000 with annual operating expenses of $2,500-$5,000. Admin obligor structures require significantly higher initial capitalization, though exact amounts vary by administrator and program design.

The capital requirement is real, but the funds deployed in a dealer-owned program earn investment income and accumulate as a business asset. Commissions and retro bonuses are consumed as ordinary income; capital in a dealer-owned structure keeps working.

DORC/CFC structures under Section 831(b) cap annual premiums at $2.8-$2.85 million. Dealers exceeding this threshold can establish multiple reinsurance entities or transition to a Super CFC or admin obligor structure, neither of which impose annual premium caps.

Risk Tolerance

Owning the underwriting risk in a DORC or admin obligor structure means the dealer is exposed if claims exceed projections. In admin obligor models backed by A-rated carriers, though, the carrier provides a financial backstop that limits catastrophic exposure. The dealer retains underwriting upside while the carrier absorbs losses beyond program thresholds.

Industry benchmarks often target a loss ratio of approximately 70%, though this varies by franchise brand, region, and product mix. A 98% loss ratio triggers remediation and deep operational review. Risk tolerance should be evaluated honestly alongside reserve capacity and the claims management quality the program partner provides — poor claims adjudication inflates losses and erodes the profit advantage of ownership.

Tax Planning Goals

Dealer-owned structures — particularly admin obligor reinsurance companies — offer meaningful tax planning advantages by accumulating underwriting profits inside a separately owned entity. Under Section 831(b), only investment income is subject to federal corporate tax; ceded premiums are not taxed, and shareholder taxation can be deferred until distribution. Dividends typically receive capital gains treatment rather than ordinary income rates.

Retro programs generate periodic taxable income with no structural ability to defer, invest, or shelter earnings inside a dealer-controlled entity — a meaningful gap for dealers with tax planning objectives beyond annual cash flow.

Dealers should consult a qualified tax advisor for their specific situation. Tax treatment varies by structure, domicile, and individual circumstances.

Administrative Support and Compliance Needs

Owning an F&I product entity — whether DORC or admin obligor — creates compliance, reporting, claims adjudication, and financial filing responsibilities beyond most dealership finance offices to manage independently. The quality and completeness of the program administrator's support is one of the most critical factors in whether the program succeeds.

Essential administrative services include:

- Legal filings and state approvals for contracts and policies

- Tax return preparation by insurance tax specialists

- Claims adjudication and loss ratio monitoring

- Monthly financial statements and annual reports

- Compliance management under IRS Code 831(b) and state regulations

- F&I training, menu development, and product optimization

A low-cost administrator with poor service will cost far more than the fee savings over time — service depth matters as much as the fee structure.

Long-Term Wealth Building Objectives

For dealers with a long-term view, admin obligor reinsurance programs function as a wealth-building engine. Accumulated premiums in the owned entity can be deployed into real estate purchases, children's education, reinvestment into the dealership, or other assets — turning F&I sales into a compounding personal and business asset.

Diverse income streams like reinsurance lower the risk profile of the enterprise, which tends to increase overall business valuation — a critical factor in buy-sell transactions. Reinsurance entities also serve as flexible vehicles for transferring wealth in multi-generational dealership families.

Retro programs and standard reserves provide reliable cash flow, but they don't build capital, generate investable assets, or create equity in a separately owned structure — the tradeoff that defines long-term program selection.

How DealerRE Can Help You Choose and Build the Right Program

DealerRE specializes in admin obligor reinsurance: the structure that gives auto dealers full ownership of their F&I profit, maximum underwriting income retention, and the ability to build long-term investable assets. With 28+ years of experience and more than 400 dealers served nationwide, DealerRE helps dealers identify which program structure fits their volume, capital position, and goals, then builds and manages that program from the ground up.

What's Included:

- Expert dealership analysis for maximum profitability

- Fast and easy company setup with no hidden fees

- F&I training, menu development, and product optimization

- Claims adjudication and compliance management

- Legal filings, tax returns, and performance reporting

- A-rated carrier backing for institutional-grade financial security

DealerRE operates on a straightforward premise: the company succeeds only when the dealer does. That means ongoing guidance as volume grows and the program matures — with the same team managing compliance, claims, and performance reporting from day one through year ten.

Conclusion

Selecting a profit participation program is not a one-time administrative choice — it is a strategic financial decision that shapes how much a dealership retains from every F&I sale for years ahead. The structure chosen today determines whether F&I income builds a dealer-owned asset or simply generates taxable commissions.

Before committing to any program structure, dealers should take three concrete steps:

- Audit the current arrangement — confirm whether the program captures underwriting profit or only generates commission income

- Assess long-term asset value — compare what a dealer-owned reinsurance structure builds over five years versus what periodic bonuses actually net after ordinary income tax

- Consult a reinsurance specialist — a structured review with an experienced administrator clarifies which program type fits the dealership's volume, risk profile, and financial goals

The gap between maximum and minimum participation compounds over time. Done right, F&I reinsurance builds real equity. Done wrong, it leaves the most profitable portion of every deal on someone else's balance sheet.

Frequently Asked Questions

What are profit participations?

In the auto dealer context, profit participations are arrangements allowing dealers to share in the underwriting profit generated by F&I products — the income remaining after claims are paid — rather than earning only a standard dealer reserve or markup.

What are the three types of profit sharing plans?

The three main structures are retro programs (third-party-controlled bonus arrangements), dealer-owned reinsurance companies (DORC), and admin obligor programs (dealer-owned obligor entities backed by A-rated carriers). Each represents a different level of dealer ownership and profit retention.

What is a typical percentage for profit sharing?

In standard arrangements, the administrator keeps 100% of underwriting profit. Dealer-owned structures change that equation: DORC programs capture underwriting profit minus administrative fees, while admin obligor programs retain 100% of both underwriting and investment income for the dealer.

What is the difference between a retro program and a dealer-owned reinsurance company?

In a retro program, the third party controls the reserve and decides when and how much to refund. In a DORC, the dealer owns a separate reinsurance entity that directly captures underwriting profit — giving the dealer control over timing, investment of reserves, and long-term accumulation.

How much F&I volume does a dealer need to start a reinsurance or admin obligor program?

Most DORC programs require 20-25 VSCs per month at minimum; admin obligor structures typically call for 25-30 contracts monthly (300-350 annually). GAP and ancillary products are evaluated individually based on premium volume and loss history.

What is an admin obligor reinsurance program?

An admin obligor program names the dealer's own company as the obligor on F&I contracts, backed by an A-rated insurance carrier. The dealer captures full underwriting profit while the carrier provides the financial backstop.