Introduction

Auto dealers face a fundamental profit problem that most never fully recognize: the third-party F&I product providers and warranty companies handling your vehicle service contracts, GAP coverage, and ancillary products are keeping profits that belong to your dealership. Average F&I gross profit per vehicle reached $2,505 in Q1 2025, yet dealers in traditional third-party models collect only a commission while underwriting profits and investment income flow elsewhere. The captive insurance manager you choose determines whether that changes.

This is one of the highest-stakes vendor decisions a dealer principal makes. A captive insurance manager handles regulatory compliance, claims adjudication, financial reporting, and staff training — and a wrong choice can jeopardize program compliance and invite IRS scrutiny. The Reserve Mechanical Corp. case saw premiums reclassified and taxed at 30% when a poorly managed captive failed basic insurance tests.

This guide breaks down what a captive insurance manager does in a dealership context, the criteria worth evaluating, and the questions to ask before committing to a long-term partner.

Key Takeaways

- A captive insurance manager oversees your dealer-owned reinsurance company's operations—underwriting, claims, compliance, and financials

- Auto dealer expertise matters: generic captive managers lack F&I product knowledge and miss optimization opportunities

- Evaluate on: dealer-specific experience, full-service capabilities, regulatory track record, and fee transparency

- Ask for client references from active dealerships before signing anything

- Confirm they handle all legal filings, tax returns, and renewals—not your CPA

- Red flags: hidden fees, vague pricing, vendor conflicts, and managers who handle captives as a secondary offering alongside unrelated industries

What Is a Captive Insurance Manager for Auto Dealers?

A captive insurance manager in the dealer context is a licensed professional or firm that establishes and manages a dealer-owned reinsurance company—often structured as an admin obligor—enabling dealers to replace third-party F&I products and capture underwriting profits that would otherwise flow to outside warranty and insurance providers.

Understanding Dealer-Owned Reinsurance

Dealer reinsurance flips the traditional F&I model. Instead of earning only a flat commission while the contract administrator retains underwriting profit and investment income, the dealer creates a legally separate reinsurance entity that assumes the risk and captures both profit streams.

The structure works through three stages:

- A fronting insurance company underwrites the F&I products and collects premiums

- Premiums flow into the dealer's reinsurance entity, which assumes claims responsibility

- Unearned premiums sit in conservative investments until contracts expire — at that point, they become dealer capital to reinvest as the owner sees fit

Core Responsibilities of a Captive Insurance Manager

A qualified manager handles four core functions:

- Underwriting and pricing — coordinates with actuarial partners to set coverage terms, exclusions, and pricing for VSCs, GAP, and ancillary products. These decisions directly drive claims ratios and program profitability.

- Claims adjudication — evaluates and pays claims, sets appropriate reserves, and tracks outcomes against projections. Consistency here reflects both program health and customer satisfaction.

- Compliance and financial reporting — prepares monthly financials, files regulatory documents, and manages tax returns under Section 831(b) or applicable code sections. The January 2025 IRS final regulations created a "seller's captive" exception: if 95% or more of the captive's business is third-party customer risk, no Form 8886 filing is required. Compliance lapses still carry significant risk regardless.

- F&I staff development — some managers provide F&I training, menu development, and dealership onboarding. Ask specifically whether this is included — it directly affects product penetration and the quality of claims that come in.

Key Factors for Choosing the Right Captive Insurance Manager

The auto retail environment has specific F&I dynamics, regulatory considerations, and deal-level economics that most general captive managers have never worked with. The six factors below tie directly to program profitability, compliance exposure, and long-term financial outcomes for the dealership.

Auto Dealer Industry Expertise

Generic captive management experience doesn't translate to dealerships. A manager who knows broad corporate risk structures but not F&I product margins or VSC loss ratios will miss the variables that drive profitability. BHPH customer risk profiles and dealer regulatory environments require direct experience — not on-the-job learning at the dealer's expense.

Ask specifically:

- How many auto dealership programs have you established and currently manage?

- Do you have experience with franchise, independent, and BHPH programs?

- Which type of dealership does your track record best match?

F&I penetration growth has driven profitability gains—more products per transaction, not higher pricing. A manager without direct dealer experience won't understand how menu simplification, product bundling, and staff training affect underwriting results.

Full-Service vs. Limited-Service Administration

| Full-Service | Limited-Service | |

|---|---|---|

| Underwriting & Claims | Included | Dealer coordinates separately |

| Compliance & Tax Filings | Included | Dealer coordinates separately |

| Staff Training | Included | Dealer coordinates separately |

| Administrative Burden | Low | High |

For most dealers, especially those new to captive programs, a full-service arrangement reduces administrative burden and ensures no compliance element falls through the cracks. The manager who handles everything is also more accountable for overall program performance.

Regulatory Compliance and Tax Management

Captive insurance programs operate within a defined legal and tax framework. The manager must stay current on:

- Domicile regulations (e.g., Tennessee requires $250,000 minimum capital, Nevada requires $200,000)

- IRS captive insurance guidelines under Section 831(b) or 501(c)(15)

- State-specific requirements applicable to the dealer's program

The Reserve Mechanical case shows the consequences of poor management: premiums four times higher than commercial coverage without actuarial justification, circular flow of funds lacking risk distribution, and a $340,000 claim paid without investigation.

Confirm the manager explicitly takes responsibility for all legal filings, renewals, and tax returns—not your CPA or attorney who may lack captive-specific knowledge.

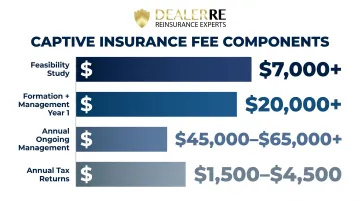

Financial Transparency and Fee Structure

A trustworthy manager presents their fee structure clearly upfront—no sliding scales, no vague language, and no fees that surface only after the program is underway.

Common fee components include:

- Feasibility study: $7,000+

- Formation + management (Year 1): $20,000+

- Annual management (ongoing): $45,000–$65,000+

- Tax returns: $1,500–$4,500 annually

Source: Captive Experts industry benchmarks

Ceding fees and proprietary fund fees can significantly erode returns. Ask whether the manager earns any compensation from third-party vendors, carriers, or banks tied to the program. Undisclosed compensation arrangements represent a conflict of interest that could bias program recommendations away from the dealer's best interest.

Track Record and References

The single most reliable predictor of future program performance is a manager's documented history:

- How long have they been in business?

- How many programs have they established?

- What do the claims and compliance records look like?

- Are current dealer clients willing to speak on their behalf?

Request references specifically from similar-sized or similar-type dealerships. A manager with strong results at large franchise groups often lacks the experience or service model suited to an independent or BHPH dealer.

Independence from Conflicts of Interest

A captive manager's primary obligation should be to the dealer, not to a carrier, product provider, or parent brokerage firm. If the manager requires the dealer to use specific banks, carriers, or service vendors as a condition of the program, this may signal a financial relationship that benefits the manager more than the dealer.

Independent captive managers—those whose core business is program management rather than product sales—give unbiased advice on program structure, coverage choices, and reinsurance partners. Watch for these conflict signals:

- Required use of specific banks or carriers as a program condition

- Undisclosed compensation from vendors tied to the program

- Parent company that sells the products the captive is designed to replace

Questions to Ask Before You Sign

Before signing with any captive manager, put these questions directly to them — and pay close attention to how they respond:

- How long have you been managing dealer-owned captive/reinsurance programs, and how many active dealer programs are you currently managing?

- What does your fee structure include, and are there any fees not covered in your base arrangement?

- Who handles regulatory filings and tax returns — is that included in your service, or is it the dealer's responsibility to coordinate?

- Can you provide references from dealerships of a similar size and type to ours?

- What happens to our program and our assets if we decide to transition away from your management?

The answers tell you more than what's on paper. A manager who hedges on fees, resists providing references, or can't clearly explain program transition procedures is giving you a preview of how they'll handle every issue that comes up after you sign.

Red Flags to Watch Out For When Evaluating Managers

Some managers market themselves effectively but lack the substance to deliver. The following warning signs should prompt dealers to slow down or walk away:

- Fee schedules that are vague, sliding, or not fully disclosed upfront

- Captive administration offered as a secondary service rather than a core specialty

- Mandatory use of specific third-party vendors with no explanation why

- Refusal or inability to provide references from current dealer clients

- Claims experience that consistently falls short of projections made at program inception

- Monthly financial reporting that lacks detail or transparency

If any of these patterns appear during your evaluation, take them seriously — switching managers after a program is established is complex and costly. Transition mechanisms include novation, loss portfolio transfer, and stock acquisition, and legacy acquirers typically prefer liabilities at least three years past policy expiration. A runoff transaction can take up to a year.

That's a year of operational disruption and legal overhead that most dealers can't afford — making the due diligence you do now worth every hour.

How DealerRE Can Help Auto Dealers Build and Manage Reinsurance Programs

If you've worked through the criteria above, DealerRE is worth a close look. The firm has spent more than 30 years focused exclusively on dealer-owned reinsurance — helping more than 400 franchise, independent, and BHPH dealers replace third-party F&I products and keep the underwriting profits they'd otherwise hand to outside providers.

Here's what working with DealerRE actually looks like.

Full-Service Model

DealerRE manages all legal forms, filings, tax returns, and renewals on behalf of the dealer. The firm provides:

- Claims adjudication

- F&I training, menus, and onboarding for dealership staff

- Ongoing performance reports and financials so dealers always have a clear picture of program health

- No hidden fees

- No outsourced obligations left to the dealer to manage independently

Key Differentiators

- Admin obligor structure backed by A-rated insurers — dealers get the profit benefits of self-insurance with fronting carrier security behind it

- Investment access on earned premiums — once unearned premiums exceed 125% of reserves, excess funds can be deployed into real estate, business reinvestment, or other assets

- F&I training and menu development built into the program, directly improving claims quality and per-deal profitability

- Staff with dealership experience — team members have worked as F&I managers and salespeople, so advice reflects how a real finance office runs

To explore whether a reinsurance program is the right fit for your dealership, contact DealerRE at (804) 824-9533.

Frequently Asked Questions

What is the role of a captive manager?

A captive manager oversees the day-to-day operations of a captive insurance or reinsurance company—handling underwriting, claims adjudication, regulatory compliance, and financial reporting—so the business owner can benefit from the program without managing its administrative and legal complexity directly.

What is the difference between a captive insurance manager and a reinsurance administrator for auto dealers?

A reinsurance administrator in the dealer context manages the dealer's admin obligor reinsurance company—including F&I product underwriting, VSC claims, and financial reporting. A traditional captive manager may focus more broadly on corporate risk structures. For dealers, the distinction matters: prioritize experience with dealer-owned reinsurance programs specifically.

How long does it take to set up a dealer-owned captive reinsurance company?

Setup timelines vary based on domicile, regulatory requirements, and how prepared the dealer's financial information is. Ask your prospective manager for a realistic project timeline during the evaluation process.

Can a small independent or BHPH dealer benefit from a captive reinsurance program?

Yes. Independent and BHPH dealers can participate—industry sources generally cite 20–25 vehicle service contracts per month as the minimum volume for meaningful results. The structure lets smaller dealers retain F&I profits and control claims, provided the manager has experience at that scale.

What happens to my reinsurance program if I decide to switch captive managers?

Switching managers requires transferring program records, notifying the domicile regulator, and ensuring uninterrupted claims handling—a multi-step process that can take months. Selecting the right manager upfront is far more straightforward than correcting a poor fit later.

How do I know if a captive insurance manager is truly independent and conflict-free?

Ask directly whether the manager receives compensation from any third-party carriers, banks, or product vendors connected to the program, and request a written disclosure of all fee sources. A manager whose only compensation comes from the dealer—not from affiliated vendors—is in the strongest position to give unbiased advice.