Introduction

Federal law classifies BHPH dealers who extend in-house credit as creditors — subject to the same Truth in Lending Act obligations as banks and finance companies. That distinction carries real consequences: FTC enforcement can mean civil penalties up to $53,088 per violation, not the outdated $11,000 figure often cited.

Beyond federal fines, dealers face private civil liability, state-level consumer protection claims, and consent orders that force fundamental business changes.

This guide covers what BHPH dealers need to know to stay compliant and avoid enforcement:

- TILA and Regulation Z fundamentals for in-house creditors

- Required deal-level disclosures and how to calculate them correctly

- Advertising trigger term rules that catch many dealers off guard

- Common violations that attract FTC and CFPB scrutiny

- How to build a defensible compliance program

TLDR: Key Takeaways for BHPH Dealers

- Two or more in-house financed sales in any 12-month period makes you a creditor under TILA, triggering full Regulation Z requirements

- Every retail installment contract needs a TILA disclosure box (APR, finance charge, amount financed, total of payments) grouped and presented before signing

- Using any trigger term in ads (down payment, payment count, monthly payment) legally requires full APR and repayment term disclosure in the same ad

- Violations attract FTC enforcement at $53,088 per violation, plus private statutory damages and state consumer protection claims

- Regulators deploy mystery shoppers at BHPH lots; dealers without written credit policies face compounded TILA and Fair Lending exposure

What Is TILA and Why Does It Apply to BHPH Dealers?

The Truth in Lending Act (15 U.S.C. 1601) is federal law requiring clear, standardized disclosure of loan terms and costs in consumer credit transactions. Regulation Z (12 CFR Part 1026) is the implementing regulation BHPH dealers must follow.

Regulation M (12 CFR Part 1013) governs consumer leases separately. If you operate a lease-here-pay-here model, different disclosure rules apply.

Regulation Z: The Four-Part Test for BHPH Dealers

You must comply with Regulation Z if all four criteria are met:

- Credit is offered to consumers (not businesses)

- Credit is offered regularly (more than one transaction in any 12-month period)

- Credit is subject to a finance charge OR repayable in 4+ installments

- Credit is for personal, family, or household use

Nearly every BHPH dealer meets all four criteria. A dealer making just two in-house financed sales in a year qualifies as a creditor under 12 CFR 1026.2(a)(17).

What Transactions Are Exempt from TILA

TILA exemptions include:

- Business or commercial purpose credit (vehicle purchased for business use)

- Credit exceeding $73,400 (2026 threshold, adjusted annually)—most BHPH transactions fall well below this

- Agricultural loans

- Securities or commodities transactions

BHPH consumer auto loans do not qualify for any of these exemptions. One threshold worth monitoring: the credit amount limit adjusts annually based on CPI-W. Verify the current figure at the CFPB Regulation Z threshold page.

Required TILA Disclosures: What Every BHPH Deal Must Include

The TILA Disclosure Box

Every retail installment contract must include a TILA box—a disclosure block containing all required terms. Critical rules:

- All required disclosures must be grouped together

- Segregated from other contract information (not buried in general contract language)

- Clear and conspicuous (not fine print)

- Must not include unrelated content

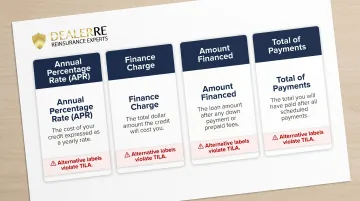

The Big Four: Core Disclosures

Each of these must be disclosed using the exact term required by Regulation Z:

| Required Disclosure | Exact Label | What It Means |

|---|---|---|

| Annual Percentage Rate | "annual percentage rate" or "APR" | Cost of credit as a yearly rate |

| Finance Charge | "finance charge" | Total dollar cost of the credit |

| Amount Financed | "amount financed" | Loan principal after down payment and trade-in |

| Total of Payments | "total of payments" | Total amount buyer will pay after all scheduled payments |

Using alternative terms like "interest rate" or "finance rate" instead of "annual percentage rate" violates TILA—even if the number is accurate. The label itself is a legal requirement, not a suggestion.

Payment Schedule and Balloon Payment Disclosures

Under 12 CFR 1026.18(g), you must disclose:

- Number of payments

- Payment amounts

- When payments are due

Balloon payments (any payment more than twice the size of a regular periodic payment) must be disclosed separately, outside the main payment table. BHPH dealers using balloon structures who skip this step face a clear TILA violation—regardless of whether the payment amount itself was accurate.

Timing and Format Requirements

Getting the content right matters—but so does how and when you deliver it. Three rules govern disclosure delivery:

- Before consummation: Disclosures must be provided before the customer signs. Handing them over after closing is a violation.

- Retain a copy: The consumer must leave with a copy of the disclosures. Showing a document and taking it back does not satisfy TILA.

- Clear and conspicuous: Disclosures must be reasonably understandable. Burying required terms in 6-point font or dense legal language does not meet this standard.

TILA Advertising Rules: Trigger Terms and Compliance

What Counts as an Advertisement

Regulators define "advertisement" broadly—any commercial message in any medium promoting a credit transaction:

- TV, radio, print ads

- Digital ads, email, social media posts

- Price tags on lot vehicles showing credit terms

- Phone solicitations

Communications during a specific deal negotiation are not advertisements. Anything promoting financing terms to the public is.

The Four Triggering Terms

When any one of these appears in an advertisement, you must also disclose the complete credit picture:

- Amount or percentage of down payment ("$0 down," "$500 down")

- Number of payments or repayment period ("48 months to pay," "24 payments")

- Amount of any payment ("$199/month," "payments as low as $150")

- Amount of any finance charge ("0% interest," "$500 finance charge")

Required Additional Disclosures

When you use a trigger term, the ad must also state:

- Down payment amount or percentage

- Full repayment terms (including balloon payments if applicable)

- Annual percentage rate (using that exact term or "APR")

Safe Harbor Language (No Additional Disclosures Required)

These phrases do NOT trigger additional disclosure requirements:

- "Financing available"

- "Easy monthly payments"

- "Low down payment accepted"

- "Terms to fit your budget"

Examples of Triggering vs. Non-Triggering Ads

Triggers additional disclosures:

- "Drive home for $199" (payment amount)

- "$0 down available" (down payment)

- "0% interest financing" (finance charge)

- "Up to 48 months to pay" (number of payments)

Does not trigger:

- "Flexible financing options"

- "We finance anyone"

- "Bad credit? No problem"

Digital Advertising Rules

Online ads can use hyperlinks to display required disclosures if:

- The hyperlink label is obvious (such as "See full terms")

- The linked page shows complete disclosures prominently, without distractions

- The hyperlink is tested and functional

Digital ads give BHPH dealers more flexibility than print — but Regulation Z still requires disclosures to be clear, conspicuous, and easy to find. A buried hyperlink or a cluttered landing page won't satisfy the standard.

Getting the mechanics right is one thing. The penalties for getting it wrong are another.

Penalties for Advertising Violations

TILA does not allow individual consumers to sue over advertising violations (15 U.S.C. 1640(a) excludes Part C advertising requirements). However:

- The FTC can impose fines up to $53,088 per violation

- State attorneys general can bring enforcement actions

- Some states classify TILA advertising violations as unfair or deceptive trade practices, opening dealers to state-level liability

Federal enforcement actions show how seriously regulators treat these violations. The FTC's 2015 Operation Ruse Control targeted auto dealers for advertising violations where ads promoted attractive terms while burying limitations in fine print. In 2017, Cowboy Toyota settled FTC charges for deceptive Spanish-language advertising. The FTC sent warning letters to 97 dealership groups in March 2024 regarding deceptive pricing practices.

Common TILA Violations for BHPH Dealers (and How to Avoid Them)

Most BHPH dealers don't set out to violate TILA — the violations happen because of inconsistent forms, ad copy written without legal review, or credit policies that were never written down. Here are the four most common failure points and how to close them.

Incomplete or Missing TILA Disclosure Boxes

Using non-standardized contract forms, omitting required fields, or burying TILA disclosures inside other contract language are among the most common documentation errors in BHPH.

Use standardized Retail Installment Sales Contracts (RISCs) from approved vendors or finance sources. The TILA box must be:

- Clearly separated from surrounding contract language

- Complete with all four required disclosures

- Written using exact regulatory terminology

Triggering Term Trap in Advertising

Ads listing payment amounts, down payments, or loan terms without the required APR and full repayment terms violate TILA's triggering terms rule. This is especially common in social media posts and price tags on lot vehicles.

Before publishing, audit all advertising across every channel. If you mention a specific payment, down payment, or loan term, include the full disclosure in the same ad — or cut the specific term and use safe harbor language instead.

APR Disclosure Errors

Listing a rate as "interest rate," "finance rate," or just "6%" without the required label violates TILA — even when the number itself is accurate. The label matters as much as the figure.

Always use the exact term "annual percentage rate" or "APR" in both the TILA box and any advertising that includes rate information. No variations or shorthand.

Inconsistent Credit Terms Across Customers

Different buyers receiving different down payment requirements or payment terms without documented rationale can trigger both TILA compliance issues and ECOA violations at the same time — meaning one policy gap can generate two separate enforcement actions at once.

The fix requires more than good intentions:

- Develop written credit and underwriting policies that define how terms are set

- Apply those policies uniformly across every customer

- Train all staff on what consistent application looks like in practice

TILA and Fair Lending: Why BHPH Dealers Face Double Compliance Risk

Regulators don't evaluate TILA in isolation. When BHPH dealers apply financing terms inconsistently—different down payments, APRs, or payment amounts for similar transactions—they risk violations of both TILA and the Equal Credit Opportunity Act (ECOA) at the same time.

Documented BHPH Enforcement: United States v. Guaranteed Auto Sales

In United States v. Guaranteed Auto Sales (D. Md., July 2020), the Department of Justice used mystery shoppers from the Fair Housing Testing Program to investigate a BHPH dealership in Glen Burnie, Maryland. Key findings:

- African American testers were required to pay larger down payments ($2,000 vs. $1,500 for white testers)

- African American testers were denied installment payment of down payments

- African American testers were quoted higher monthly payments ($150 vs. $125 for the same vehicles)

The consent order required the dealership to:

- Develop written financing policies to govern all credit decisions

- Post nondiscrimination notices

- Provide mandatory ECOA training to all staff

- Submit ongoing compliance reports to the DOJ

This case confirms BHPH dealers must assume testers may visit their lots. The absence of written credit policies was a contributing factor in the discrimination finding.

FTC Enforcement: Bronx Honda

The FTC's 2020 Bronx Honda case resulted in a $1.5 million settlement for violations of the FTC Act, TILA, and ECOA. The FTC found:

- African American consumers were charged approximately $163 more in interest

- Hispanic consumers were charged approximately $211 more than similarly situated non-Hispanic white consumers

Both cases follow the same pattern: inconsistent lending terms across customer groups triggered liability under multiple federal statutes at once. The practical takeaway is that TILA compliance and fair lending compliance are inseparable for BHPH dealers.

Frontline Defense: Written Credit Policies and Staff Training

Written, consistently applied credit policies are the primary defense against both TILA and fair lending scrutiny. Key components include:

- Set underwriting criteria for down payments, interest rates, and payment terms in writing

- Apply those criteria uniformly across every customer, every deal

- Train all staff involved in credit decisions, deal structuring, or advertising

- Document training attendance and verify comprehension

Without written policies, individual staff make inconsistent judgment calls — and inconsistency is exactly what regulators look for.

Building a TILA-Compliant F&I Program for Your BHPH Dealership

Foundational Compliance Steps

Use standardized contracts: Adopt compliant retail installment sales contracts from approved sources. Ensure the TILA box is clearly separated and includes all required disclosures.

Audit advertising regularly: Review all advertising materials across all channels—digital, print, social media, and lot signage. Verify that any triggering terms are accompanied by full disclosures.

Establish written credit policies: Document how down payments, interest rates, and payment terms are determined. Apply these policies consistently for all customers and train all staff on their use.

Ongoing Monitoring and Training

TILA compliance is not a one-time task. It requires:

- Periodic staff retraining on TILA requirements and Fair Lending principles

- Regular advertising audits to catch new violations before they attract enforcement

- Tracking regulatory updates — including annual TILA threshold adjustments — so your policies stay current

BHPH dealers with well-structured F&I programs — clear product menus, compliant disclosure practices, and documented deal processes — are in a stronger position during any regulatory examination.

Industry Resources and Support

The National Independent Automobile Dealers Association (NIADA) offers several resources specifically relevant to BHPH compliance:

- Certified Master Dealer (CMD) program — includes dedicated compliance and F&I training modules

- NIADA Dashboard — publishes ongoing BHPH regulatory compliance content

- BHPH Dealer Forum — connects dealers with compliance experts and experienced operators

Working with an F&I program administrator can also provide ongoing support on compliance structure, staff training, and documentation oversight. DealerRE partners with BHPH dealers to build structured F&I programs that support both profitability and compliance, covering reinsurance program administration, claims adjudication, and compliance management — so dealers can focus on running their business.

Frequently Asked Questions

What is the Truth in Lending Act in simple terms?

TILA is a federal law requiring lenders—including BHPH dealers—to clearly disclose the costs and terms of any credit they extend to consumers. Buyers must see those disclosures before signing so they can compare loan offers and understand exactly what they're agreeing to pay.

Does TILA and Regulation Z apply to car dealerships?

Yes. TILA and Regulation Z apply to any car dealership that regularly extends credit directly to consumers. BHPH dealers who finance their own sales act as both seller and lender, triggering full Regulation Z disclosure requirements on every deal.

What information is required to be disclosed under TILA?

TILA requires disclosure of the annual percentage rate (APR), finance charge (in dollars), amount financed, total of payments, and the payment schedule—all presented together in a TILA disclosure box before the deal is finalized.

What transactions are exempt from TILA?

TILA exempts credit for business or commercial purposes, loans above $73,400 (2026 threshold), agricultural loans, and certain securities transactions. BHPH consumer auto loans do not qualify for any of these exemptions.

Do you need a license for buy here pay here?

Licensing requirements for BHPH dealers vary by state and may include dealer licenses, sales finance licenses, or consumer lender licenses. Check with your state's motor vehicle and financial regulatory agencies to confirm which licenses apply before you begin financing customers directly.